Neutral Tata Chemicals Ltd for the Target Rs.700 by Motilal Oswal Financial Services Ltd

Industry headwinds hurt performance; near-term outlook subdued

Operating performance significantly below our estimates

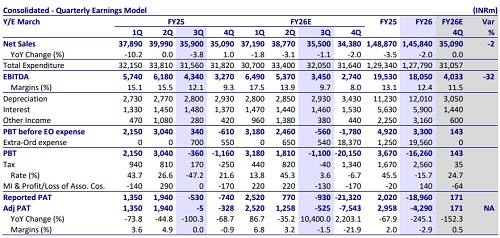

* Tata Chemicals (TTCH) posted a weak performance in 4QFY26, with consol. EBITDA declining 16% YoY. The slowdown was led by subdued performance across all the businesses, hit by lower realizations and higher fixed costs.

* Further, due to adverse current market conditions and unremunerative Southeast Asian markets (the highest export share of the US business), TTCH has recognized an INR18b impairment in goodwill in the US business.

* The global soda ash market remained muted with flat demand, excess inventory, and geopolitical pressures keeping costs elevated. However, no sharp demand destruction was visible. India stands out with strong demand and high utilization, supported by reduced imports and a shift toward domestic sourcing.

* Factoring in a weak 4Q performance and near-term macro environment, we cut our FY27/FY28 EBITDA estimates by 9%/5%. We reiterate our Neutral rating with an SoTP-based TP of INR700.

Earnings dip on weaker realizations across regions

* TTCH reported an overall revenue of INR34.4b (est. in line) in 4QFY26 (down 2% YoY) primarily due to lower realizations. EBITDA margin contracted 130bp YoY to 8% (est. ~11.5%), and EBITDA stood at INR2.7b (est. INR4.0b), down 16% YoY.

* It posted an adj. net loss of INR7.5b vs. adj. net loss of ~INR328m in 4QFY26 (est. ~INR171m). The company has reported an impairment in goodwill of the US business of INR18b.

* The Basic Chemistry Products business fell 3% YoY to INR29.3b. Operating loss was INR18b (vs. EBIT of INR840m YoY). EBIT margin stood at -61%.

* The Specialty Products business grew 7% YoY to INR5b. Loss before interest and taxes was INR460m (operating loss of INR630m in 4QFY25). EBIT margin stood at -9.1%.

* The Indian standalone revenue rose ~3% YoY to INR12.5b, while TCNA/TCEHL/TCAHL dipped 10%/19%/3% YoY to INR11.8b/INR3.4b/INR1.5b. Rallis increased 6% YoY to INR4.6b

* EBITDA for India standalone/TCNA/TCAHL declined 6%/55%/45% to INR2.2b/INR360m/INR290m. EBITDA loss for TCEHL/Rallis stood at INR70m/ INR10m (vs. a loss of INR280m/INR180m).

* EBITDA/MT of TCNA stood at USD7.5 (vs. USD15.7 YoY). EBITDA/MT of TCAHL declined 54% YoY to USD39. EBITDA margin for India standalone contracted 160bp YoY to 17.2%.

* For FY26, revenue/EBITDA declined 2%/8% to INR146b/INR18b. TTCH reported an adj net loss of INR4.3b vs. an adj net profit of INR2.9b in Mar’25.

* Gross debt stood at INR71.1b vs. INR63.0b as of Mar’25. Further, the CFO stood at INR1.3b vs. INR1.8b as of Mar’25.

Highlights from the management commentary

* Demand-supply scenario: Global soda ash markets remained adequately supplied, and the supply overhang continued to exert pressure on pricing in 4QFY26. The challenging external environment amid the ongoing geopolitical crisis in the Middle East led to a rise in power and logistics costs, uncertainty, and limited visibility of any immediate change in market conditions.

* India: Soda ash demand in India remains robust, with customers shifting to domestic sourcing amid geopolitical tensions. Power costs (imported coal) remain insulated, cost increases are largely passed through, and a potential safeguard duty is under evaluation.

* Supply chain risk: Ammonia supply remains under watch in India following regulatory restrictions on fertilizer units supplying to non-fertilizer players; while current availability is adequate, any prolonged constraint could pose an operational challenge. In Kenya, HFO remains a key concern with ~45 days of inventory, after which procurement at sharply higher spot rates (up ~50–60%) could further pressure costs despite ongoing pass-through efforts.

* Capex: TTCH has guided capex of INR13b in FY27 for growth (Silica and Singapore acquisition) and maintenance capex. Silica plant/Dense Soda ash plant/Iodized Salt at Cuddalore/Mithapur/Tamil Nadu are expected to be commissioned by 4QFY28/3QFY28/2QFY29. Further, TTCH’s board approved INR1b capex to debottleneck salt capacity at the Mithapur plant by 82.5kTPA over the next 12-14 months, on which ~20% returns are expected.

Valuation and view

* The near-term environment remains unfavorable, with the soda ash demand– supply balance yet to meaningfully improve despite expectations of future demand from solar glass and electric vehicles. Benefits from these end-use industries are likely to play out gradually while the current oversupply persists. Although the company has expansion plans in India, the payoff remains contingent on a broader cyclical recovery, limiting near-term upside.

* We expect TTCH to record a revenue/EBITDA CAGR of 9%/27% over FY26-28. Reiterate Neutral with an SoTP-based TP of INR700.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)