Buy Motherson Wiring Ltd For Target Rs. 46 Motilal Oswal Financial services Ltd.

Spurt in copper prices hurts performance

Demand outlook remains healthy

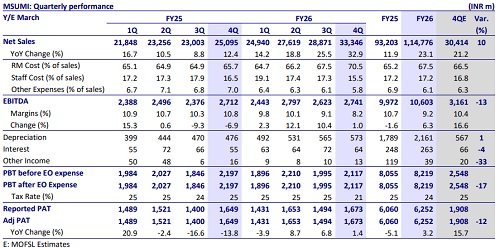

* Motherson Wiring’s (MSUMI) 4Q PAT came below our estimates at INR1.7b (+1.4% YoY), primarily due to an 18% QoQ jump in copper prices. While rising Cu prices are a pass-through with a lag of a quarter, the sustained rise in Cu prices over the last few quarters has been hurting margins.

* Considering a pickup in auto demand after GST rate cuts and the ramp-up of its new greenfield plants, we estimate MSUMI to post a CAGR of 11%/18%/18% in revenue/EBITDA/PAT over FY26-28E. The company’s premium valuations at 36x/30x FY27E/FY28E EPS seem justified, given its strong competitive positioning, top-decile capital efficiency, and benefits of EVs and other mega-trends in autos. We reiterate our BUY rating with a TP of INR46 (based on 35x FY28E EPS).

PAT below our estimate in 4Q, led by sustained margin pressure

* Revenue grew 33% YoY to INR33b, aided by the commencement of new greenfield plants, which contributed to INR4.4b. Excluding these plants, revenue grew ~21% YoY, much higher than the PV industry growth of 13% YoY for 4Q. The growth was due to input cost inflation. The EV revenue share was 8.6% in 4QFY26.

* Copper inflation was steep, rising ~18% QoQ, with prices averaging INR1259/kg in 4Q.

* Due to high copper inflation, EBITDA margin missed our estimates, coming in at 8.2% (estimated 10.4%). EBITDA grew 1% YoY to INR2.7b, lower than our estimate of INR3.2b.

* Greenfield plants posted a combined EBITDA loss of INR139m in 4Q. Excluding the Greenfield plants, the EBITDA margin was better at 10%.

* Other income was much lower than expected at INR13m (est. INR20m).

* As a result, PAT came in below our estimate at INR1.7b, growing 1.4% YoY (estimated INR1.9b). Even adjusting for the greenfield investments, PAT declined ~2% to INR1.85b.

* MSUMI remains net debt-free despite near-term margin pressures from the greenfield plants.

Highlights from the management commentary

* MSUMI reported a strong 33% YoY revenue growth in 4Q. Of this, ~5% was attributable to copper price pass-through, while the remaining was driven by volume growth.

* Copper prices, which are 24-28% of the RM basket, increased 18% QoQ in 4Q. As a result, the gross margin dipped 290bp QoQ. While rising Cu prices are a pass-through with a lag of a quarter, the sustained rise in Cu prices over the last few quarters has been hurting margins.

* Apart from copper, polymer prices have also started rising due to geopolitical issues. However, the impact of the same is unlikely to be material.

* Adverse currency movement also impacted margins during the quarter.

* The company’s existing plants are operating at around 80% utilization, while the greenfield plants are at different stages of ramp-up. Current utilization levels are approximately 80% at Kharkhoda, 50% at Pune, and 60% at Navgam. Kharkhoda and Navgam are progressing as per plan and are expected to ramp up fully in the next couple of quarters. Pune, however, is facing some ramp-up challenges.

* Capex for FY26 stood at INR1.9b. Management expects to invest a similar amount in capex in FY27 as well, which would be invested in greenfield plants, replacement capex, and automation/digitization at existing plants.

Valuation and view

* Considering a pickup in auto demand following GST rate cuts and the ramp-up of its new greenfield plants, we estimate MSUMI to post a CAGR of 11%/18%/18% in revenue/EBITDA/PAT over FY26-28.

* The stock trades at 36x/30x FY27E/FY28E EPS. We believe MSUMI deserves rich valuations, given its strong competitive positioning, top-decile capital efficiency, and benefits of EVs and other mega-trends in autos. We reiterate our BUY rating with a TP of INR46 (based on 35x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041