Buy Home First Finance Ltd for the Target Rs. 1,350 by Motilal Oswal Financial Services Ltd.

Early delinquencies improve; easing BT-out to support growth

Prudent opex management and healthy AUM growth to anchor earnings stability

* Affordable HFCs have historically delivered robust growth, driven by strong penetration in low-tier cities, expertise in lending to informal income profiles, and relatively benign competitive intensity. However, in recent times, growth in the segment has moderated due to multiple factors such as a) increased participation from banks and other financial institutions, particularly in higher-yield secured lending segments; b) risks of MFI stress spilling over to affordable housing demand; c) weakness in the MSME segment; and d) government-related disruptions in the southern markets.

* Against this backdrop, HOMEFIRST continues to strengthen its positioning as a focused affordable housing financier. With a strong presence in the low- to middle-income segment, the company has built a granular loan book anchored by first-time homebuyers. While growth has moderated in the near term due to external disruptions and prudent underwriting, underlying business fundamentals remain intact, thereby positioning the company for a gradual recovery, supported by favorable demand dynamics and structural growth levers.

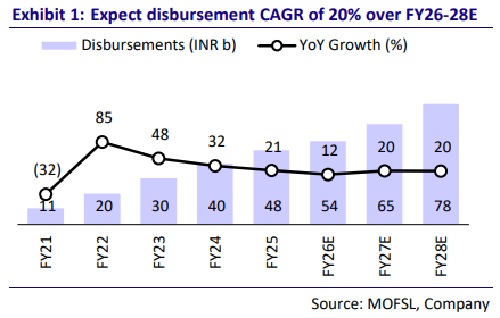

* HOMEFIRST reported AUM growth of ~25% YoY to ~INR149b in 3QFY26, despite relatively modest disbursement growth of ~11% YoY. However, management has highlighted early signs of recovery, with disbursement momentum expected to improve from 4QFY26 onward, indicating that the recent slowdown is largely cyclical. Simultaneously, easing competitive intensity, evident in lower BT-out rates (~6.6% in 3QFY26 vs. ~7.6% in 2QFY26), is expected to support a pickup in growth. Over the medium term, branch expansion, deeper penetration in affordable housing, and scale-up of co-lending initiatives should continue to drive growth, with the company guiding for ~25% AUM growth in FY27.

* Margins remain stable, supported by disciplined pricing, a predominantly floatingrate loan book, and the inherently high-yield nature of affordable housing loans. In addition, a diversified funding mix, along with an increasing share of PSU bank borrowings, continues to support cost efficiency. We expect HOMEFIRST to deliver NIMs of ~6.1%/~5.9% in FY27/28E.

* Asset quality is showing clear signs of stabilization, with 1+ DPD improving to ~5.3% (down by ~20bp in 3QFY26) as stress eases across geographies. While pockets of weakness persist, particularly in Tamil Nadu, normalization is expected from 4QFY26 onward. Strong underwriting and technology-led collections continue to support resilience. We expect credit costs to moderate to ~40bp over FY27/28E, reflecting gradual normalization.

* As growth rates gradually recover, HOMEFIRST is well positioned to be a key beneficiary of this uptrend, supported by its focused business model and execution capabilities. We estimate the company to deliver ~23% AUM CAGR over FY26-FY28E, along with stable NIM (as percentage of average AUM) of 6.1%/5.9% in FY27/FY28E. Accordingly, we recommend a BUY rating on the stock with a TP of INR1,350, premised on 2.5x FY28E BVPS.

Cyclical moderation eases; growth visibility strengthens

* HOMEFIRST has delivered steady growth, with AUM growing ~25% YoY to ~INR149b in 3QFY26, despite temporary headwinds.

* The recent slowdown appears cyclical, with early signs of recovery already visible in origination and disbursement momentum entering 4QFY26. Competitive intensity is also easing, reflected in declining BT-outs, while initiatives such as branch expansion and co-lending are enhancing growth visibility.

* With ~83% of AUM concentrated in the housing segment (ATS of ~INR1.2m), HOMEFIRST is well positioned to benefit from steady demand from first-time and new-to-credit borrowers, supporting management’s confidence in delivering ~25% AUM growth in FY27. We estimate an AUM CAGR of ~23% over FY26-28E.

Stable margins supported by prudent pricing and funding mix

* HOMEFIRST maintains stable margins through disciplined pricing and a predominantly floating-rate loan book, enabling effective repricing across interest rate cycles. Its focus on small-ticket, high-yield loans supports superior spreads relative to traditional mortgage players.

* On the liability side, a diversified funding mix, comprising banks (~57%), NHB refinance (~15%), and off-balance-sheet avenues such as co-lending (~5%) and DA (~16%), ensures both flexibility and cost efficiency.

* Improved access to bank funding, particularly from PSUs, has further optimized borrowing costs. As a result, spreads remain stable at ~5%, with NIMs expected at ~6.1%/~5.9% in FY27/ FY28E.

Calibrated expansion and technology to drive operating efficiency

* Operationally, the company is executing a calibrated expansion strategy, with a steady increase in branch presence across both core and emerging markets. This is complemented by a technology-driven operating model featuring centralized underwriting, data science capabilities, and API-based verification, enabling faster loan approvals (~90% loans approved within 48 hours) and consistent credit assessment.

* While operating expenses reflect continued investment in distribution and talent, they remain well controlled, with operating leverage expected to improve as scale and branch productivity increase.

* The cost-to-income ratio is projected to remain stable at ~33% over the medium term.

Asset quality stabilizes; credit costs set to normalize

* Asset quality is showing signs of stabilization, with early delinquency indicators improving sequentially. While some localized stress persists, particularly in select geographies, the overall portfolio remains resilient, supported by a secured and granular lending book.

* Strong underwriting practices and a technology-enabled collection framework have helped contain credit risk, with GNPA levels remaining stable. As macro conditions normalize, credit costs are expected to remain controlled, supporting a gradual improvement in asset quality metrics from FY27 onward.

* We expect credit costs to remain contained at ~39bp/36bp in FY27/FY28E, with a gradual normalization trajectory as asset quality stabilizes.

Valuation and view

* HOMEFIRST remains well placed to navigate near-term headwinds, supported by its resilient business model, granular loan book, and disciplined execution. With early signs of recovery in disbursements, easing competitive intensity, and stabilizing asset quality, growth is expected to gradually normalize. Backed by structural drivers such as branch expansion, deeper segment penetration, and co-lending, the company is well positioned to deliver steady performance over the medium term.

* We estimate the company to deliver ~23% AUM CAGR over FY26-FY28E, along with stable NIM (as a percentage of average AUM) of 6.1%/5.9% in FY27/FY28E. Accordingly, we recommend a BUY rating on the stock with a TP of INR1,350, premised on 2.5x FY28E P/BV.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041