Neutral Zen Technologies Ltd for the Target Rs. 1,400 by Motilal Oswal Financial Services Ltd

Execution ramp-up to track improving order inflows

Zen Technologies’ (ZEN) 4QFY26 results were weaker than our estimates. However, the standalone order book increased 77% YoY to INR12.1b, aided by healthy order inflows, which have been ramping up since 3QFY26. We expect revenue execution to ramp up from 2HFY27 onward. The company has added various new products to its product portfolio and expects to scale up on both standalone and consolidated basis, supported by higher subsidiary contribution. The company has also received its arms manufacturing license for 12.7mm, 23mm, 30mm and 40mm cannons. While order inflows have increased in the last six months, we believe that it is important to see sustenance of inflows in order to achieve revenue growth on both standalone and consolidated basis. We trim our estimates by 9%/3% for FY27E/FY28E and maintain our Neutral rating on the stock with an unchanged TP of INR1,400, based on 30x two-year forward earnings.

Weak set of results

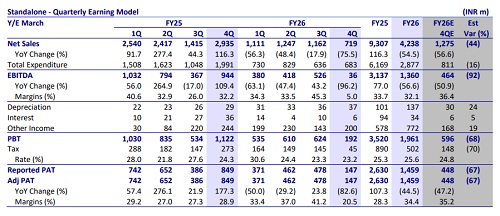

ZEN’s 4QFY26 numbers came in lower than our estimates. Revenue declined 76% YoY to INR719m, missing our estimate by 44%. Gross margins surged to 70.0% during the quarter vs. our estimate of 57.3%. However, due to weakness in overall execution, absolute EBITDA declined 96% YoY to INR36m. This led to PAT declining 83% YoY to INR147m vs. our estimate of a 57% YoY decline. The standalone order book as of FY26-end increased 77% YoY to ~INR12.1b. On a consolidated basis, the company received order inflows worth INR4.3b during 4QFY26, taking the consolidated order book to INR13.4b. For FY26, revenue/EBITDA/PAT declined 54%/57%/45% YoY, while EBITDA margin contracted 160bp YoY to 32.1%.

Subsidiaries’ execution to support consolidated revenue guidance

ZEN’s standalone execution for FY26 stood at INR4.2b, supported by an opening order book of INR6.9b. Order inflows witnessed a recovery during the year, leading to a standalone order book of INR12.1b as of FY26-end. Consolidated order book for ZEN stood at INR13.4b, including ~INR10b from equipment (52% simulators; 48% anti-drones) and the balance from AMC. For FY26, consolidated revenue/EBITDA/PAT stood at INR6.9b/INR2.4b/INR2.2b, indicating subsidiaries’ contributions to revenue/EBITDA/PAT at ~INR2.6b/INR1.1b/INR476m for FY26, with EBITDA margin/PAT margin of ~42%/18%. Revenue from subsidiaries mainly included contributions from ARIPL (INR1.3b) and UTS (INR1.2b). Pipeline for both remains healthy for coming years, with ARIPL expected to benefit from naval simulation related orders, while UTS pipeline can convert into ~INR2b worth of inflows per annum from FY28. Going ahead, the company has maintained its consolidated revenue guidance of INR40b for FY27-28 combined. Revenue contribution from its subsidiaries is guided to be ~INR3.7b in FY27, with ARIPL expected to scale up to ~INR3b by FY28 and UTS to ~INR1.5-2.0b. We expect standalone revenue to increase to ~INR10b/INR14b for FY27/FY28.

We expect margin to recover on execution scale up

ZEN’s 4Q margins were impacted by a mix of operating deleverage and several costrelated factors. Lower overall revenue led to weaker absorption of fixed costs. Employee expenses included additional costs of ~INR50m relating to year-end performance incentives. Warranty provisions were revised upward based on the actual utilization trends in anti-drone systems, leading to an incremental impact of ~INR31m. The company also incurred ~INR27m of post-supply costs related to export orders, including installation, logistics, and on-ground support. Additionally, R&D expenses were higher by ~INR33m sequentially, reflecting continued investments in future product development, which management highlighted as a structural and ongoing commitment. Going ahead, the company has guided for its consolidated EBITDA margin/PAT margin to be ~35%/25%. We factor in standalone EBITDA margin of 35.9%/36.4% for FY27/FY28 as the company’s recent order wins reach the execution stage, leading to operational leverage. We also expect PAT margin of its subsidiaries to be in line with its guidance of ~30% for ARIPL and around mid20s% for UTS.

Newly acquired arms manufacturing license to open gateways to growth over the long run

The recently received arms and ammunition licenses mark a strategic entry into a large adjacent market, particularly aligned with the company’s anti-drone focus. The initial emphasis is for manufacturing weapon systems such as 12.7mm, 20mm, and 30mm cannons, along with smart ammunition, especially 30mm programmable rounds designed for drone neutralization in hard-kill anti-drone systems. ZEN had already been working on related hardware over the past two years and sees strong demand both for standalone weapon systems and integrated solutions. While revenues from this segment are expected to be modest in the initial years, the company expects meaningful scale-up over the medium term, with manufacturing likely to commence from FY27 post testing and certification.

Upcoming products to expand its overall portfolio

ZEN is expanding its product portfolio with a strong pipeline of next-generation defense technologies aimed at capturing evolving warfare requirements. Key additions include 1) advanced anti-drone systems with wider frequency dominance from 70 MHz to 12 GHz, 2) AI-enabled anti-drone simulators for realistic training, 3) a cyber security suite designed for deployment across command centers, ships, and aircraft, 4) an unmanned ground vehicle named ‘VRISHABH’, capable of combat logistics and casualty evacuation with 150kg payload and autonomous capabilities, and 5) Hyperstrike interceptor drone, capable of speeds up to 400kmph with AIbased targeting, designed to neutralize low-cost enemy drones. These products, along with naval simulation solutions and integrated command systems, position the company to transition from a simulator-focused player to a comprehensive defense technology provider.

Financial outlook

We cut our estimates by 9%/3% for FY27/FY28 to factor in lower margins. We expect revenue of ~INR10b/INR14b for FY27/FY28, with EBITDA margin of ~36% resulting in PAT of ~INR3b/INR4.2b. This will be supported by 1) the finalization of orders across simulators and anti-drones; 2) EBITDA margin of ~36% for FY27-28; and 3) control over working capital due to improved collections. Subsidiaries’ contributions to consolidated numbers are also expected to scale up meaningfully over the next two years.

Valuation and view

The stock currently trades at 45.5x/32.4x P/E on FY27/28E earnings. While order inflows have increased in last six months, we believe that it is important to see sustenance of order inflows in order to achieve revenue growth on both standalone and consolidated basis. We cut our estimates to factor in slightly lower margins and maintain our Neutral rating on the stock with an unchanged TP of INR1,400, based on 30x two-year forward earnings.

Key risks and concerns

Any slowdown in procurement from the defense industry, especially for simulators, can expose the company to the risk of reduced order inflows and hinder its growth. ZEN is also exposed to foreign currency risks for its export revenue.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412