Consumer Goods Sector Update : Resilient topline albeit margin pressureby Emkay Global Financial Services Ltd

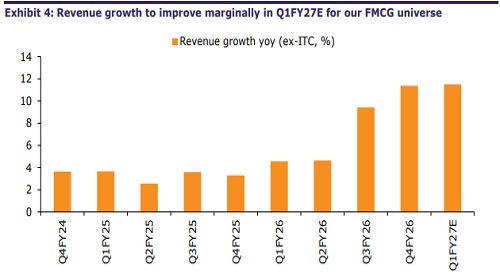

We expect the Emkay FMCG universe to report healthy revenue growth in 1QFY27, on stable demand conditions and price hikes (low-to-mid single digit). Volume growth for most players, expected to be impacted qoq partly due to price hikes, should still be healthy in our view. Margins are likely to be under pressure due to higher input costs (mainly of crude-linked derivatives and palm oil) and elevated A&P spends. GCPL, Marico, and Dabur have reported strong revenue growth in their quarterly business preview, but also highlighted margin pressure. We raise our TP for GCPL by 8% to Rs1,350 from Rs1,250 and for Marico by 5% to Rs1,000 from Rs950 due to their strong 1Q updates. Our top picks: GCPL, Marico, BRIT. We also like Honasa, Bikaji, and Gopal Snacks.

Demand

Per FMCG players’ pre-quarterly business updates, overall demand conditions were stable in 1QFY27, partly helped by easing of tensions in West Asia and the consequent decline in crude prices. Value growth should benefit from the price increases taken by the companies to offset input cost inflation. Rural continued to outpace Urban. However, going forward, the impact of El Niño on the monsoon is a key monitorable.

Margin

Raw material prices (especially crude-linked) were inflationary during the quarter, but eased subsequently with decline in crude prices. Palm oil prices were firm and are likely to impact most FMCG companies. However, some raw materials like copra, tea, coffee, etc, saw price decline and should benefit companies such as Marico, HUL, and Nestlé.

Godrej Consumer Products

Revenue growth is expected to be strong, in the high-teens, led by a high single-digit volume growth. India business is likely to grow in double-digits, while Indonesia growth would accelerate owing to the volume-driven mid-teens revenue growth. GAUM growth is likely to be strong too. Margin would see pressure due to higher input costs.

Marico

Revenue growth is likely to be strong (>20%) led by double-digit volume growth. Parachute saw a sharp jump in volume growth, to double-digits, due to price cuts. VAHO sustained its strong growth trajectory (>20%), while foods and premium personal care (incl digital first brands) continue to scale up well. Gross margin is likely to improve qoq due to sharp decline in copra prices, but EBITDA margin is likely to be impacted by higher A&P spends.

Dabur

Revenue growth is likely to be in double-digits (after 11 quarters of single-digit growth), led by near-double-digit growth in its India business and high-teens growth in International. Growth is likely to be led by double-digit growth in HPC, foods, and beverages. Gross margin is expected to be flattish yoy, as calibrated pricing actions were taken to offset the input cost inflation. However, we expect EBITDA margin to decline slightly yoy, due to higher A&P spends.

Other companies

We expect Britannia’s revenue growth at ~8% yoy, led equally by pricing and volume growth. Growth should also benefit from other players vacating the Rs4.5/9 price-points in LUPs. Margin pressure should be limited due to forward cover in palm oil. Honasa should see sequential uptick in revenue growth led by Mamaearth and sunscreens (seasonality). We expect EBITDA margin to inch up qoq due to operating leverage. HUL’s revenue growth should be ~10% yoy, aided by price increases. Growth is likely to be led by the home care segment. Margins would be under pressure due to input cost inflation, in our view. We expect ITC’s net sales to decline 1% yoy, while EBITDA is likely to decline >10% mainly due to the drag from the cigarettes segment. Nestlé and Colgate are likely to report strong revenue growth on a benign base (+16% and +9% yoy, respectively) but higher A&P spends will keep margin under pressure. We expect Emami to post double-digit revenue growth, helped by recent acquisitions and a low base. EBITDA is likely to contract by >200bps. Bikaji is expected to report a low double-digit revenue growth (ex-PLI), while EBITDA growth is likely to be lower due to higher costs. Gopal Snacks is likely to see a strong quarter, albeit on a low base.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

Financials Sector Update : ICRA Webinar on NBFC-MFIs sector outlook By Motilal Oswal Financi...