Insurance Sector Update : A slow and steady start to the year by Emkay Global Financial Services Ltd

The insurance sector is likely to report a modest performance during Q1FY27E on account of:

1) APE growth for life insurers is likely to remain modest owing to uncertainties arising from geopolitical tensions during the quarter and the overall macroeconomic situation. However, VNB margins across insurers are likely to be stable to improving, supported by continued growth in term life products.

2) The general insurance sector continues to face challenges given the absence of a Motor TP hike in FY27, heightened competition in the Motor OD segment, and increased pricing aggression in the commercial lines segment, impacting growth and claims ratios.

3) The health insurance sector continues to witness growth momentum, led by the GST rate exemption improving affordability. We expect a slight improvement in claims ratios for Star health in Q1FY27.

Against this backdrop, focus is likely to shift to key sector developments including:

1) Draft regulations on Commission and Expense of Management

2) Commencement of operations of Bima Sugam

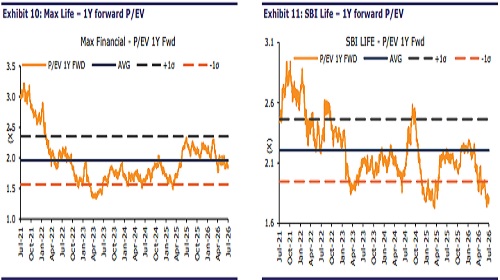

3) Transition to Ind AS accounting. The underperformance of life insurance stocks amid regulatory overhangs has made the risk-reward favorable, with life insurance stocks trading near their lowest valuation multiples since listing. Current valuations do not adequately reflect the strong franchise strengths, supported by brand, distribution, and scale. We find the sector attractively valued, especially considering the defensive nature of the insurance business.

Growth moderation in Q1FY27 while VNB margins largely stable

The uncertain geopolitical and economic environment in Q1FY27 is likely to result in APE growth moderation during the quarter. While the industry saw strong growth in Apr-26 on account of deferred purchases from Mar-26, APE growth during May-26 remained modest due to uncertainties arising from the Middle East conflict. Overall, we expect MAXF to continue its strong growth momentum delivering ~17% APE growth, while IPRU Life is expected to deliver ~13% APE growth owing to healthy growth in the group and retail segments. We expect SBI Life to clock strong 31% APE growth backed by strong growth in Group OYRGTA business. LIC is expected to report ~9% APE growth in Q1FY27. HDFC Life is expected to deliver ~10% yoy APE growth in Q1FY27E owing to slower growth in the HDFC Bank channel. VNB margins for life insurers are likely to be stable, led by continued growth momentum in the protection business. We expect MAXF and LIC to witness margin improvement, while HDFC Life, and ICICI Pru Life are likely to report largely flat margins. SBI Life is likely to witness a dip in margins given higher share of group business during the quarter. Given the ~7% increase in the NIFTY over the last quarter, we expect equity market movements to have a slight positive impact on economic variances, thus aiding EV growth.

General insurance faces challenges, while SAHIs maintain growth momentum

The general insurance sector continues to face challenges given

1) Increased competitive intensity in the Motor OD segment

2) No Motor TP rate hike expected in FY27

3) Increased pricing aggression in the Commercial Lines business, impacting the premium growth and claims ratios. Against this backdrop, we expect ICICIGI to deliver ~8% GWP growth, while GO Digit is likely to report flat GWP growth in Q1FY27E. While ICICIGI is expected to witness a slight improvement in claims ratios owing to its focus on profitability, Go Digit is likely to witness an increase in claims ratios due to likely elevation the claims ratios across the Motor and Commercial Lines segments. The health insurance segment continues its growth momentum, led by the GST rate exemption. We expect Star Health to deliver ~19% GWP growth in Q1FY27. We also expect a slight yoy improvement in claims ratios for Star Health, led by strong fresh premium growth and multiple measures undertaken by the company.

Regulatory developments to be watched, valuations remain undemanding

Investor focus is likely to shift toward evolving regulatory developments, including

1) The draft regulations on commission

2) The commencement of the Bima Sugam platform

3) The transition to Ind AS accounting. We do not expect these regulatory changesto hurt the fundamentals of life insurers. While life insurance stocks have corrected owing to regulatory overhang, we believe current valuations provide an attractive entry point. We prefer SBILIFE and MAXF. The underperformance of general insurance stocks also appears to have largely priced in the sector’s near-term challenges. Based on the risk-reward, we prefer STARHEAL and ICICIGI

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

Tag News

Life Insurance Sector Update : New business in Jul-26 - Slowdown in growth momentum by Emkay...