Building Materials Sector Update : Healthy Realization to Drive Margin Expansion by PL Capital

In Q1FY27, building material companies under coverage are expected to report healthy revenue growth of 15.7% YoY, driven by the pipes segment. EBITDA margin is likely to expand by ~210bps, supported by rising PVC resin prices, enabling larger players to pass on costs, price hikes across tiles & bathware segments, and cooling of chemicals price. Plastic pipes sector is anticipated to deliver soft volume growth of 5.4% YoY. Tiles sector is likely to experience single-digit growth. In the wood panel segment, CPBI is expected to see good revenue growth, led by the plywood segment (contributes 55% to the topline). We expect coverage companies to register sales/EBIDTA/PAT growth of 15.7%/35.9%/46.0% YoY, and tiles & bathware players to outperform in the building materials space

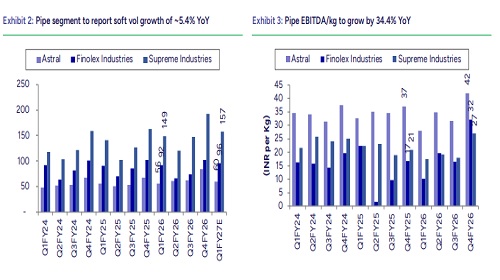

Plastic pipes - Healthy realization to offset soft volume growth:

Plastic pipe companies under our coverage are expected to report soft volume growth in Q1FY27, due to weak demand, channel destocking amid fluctuating PVC resin prices, and muted agricultural offtake owing to lower-than-expected rainfall. ASTRA/SI/FNXP are expected to report pipes & fittings volume growth of 7.0%/5.5%/4.4% YoY. Finolex Industries’ volume growth is likely to remain subdued due to soft offtake in agri pipes and cautious dealer inventory restocking, following fluctuation in PVC resin prices. Despite modest volume growth, higher PVC resin prices (+28% YoY/+9.0% QoQ in Q1FY27) are expected to support realization. We estimate Astral/Supreme Industries/Finolex Industries to report ~8%/15%/15% YoY realization growth, supported by higher YoY PVC resin prices during Q1FY27. On the profitability front, margins of the coverage pipes companies are expected to expand by ~240bps YoY to 14.3%, supported by improved realization and absence of inventory losses during the quarter.

Tiles & bathware:

Kajaria Ceramics (KJC) is expected to report revenue growth of 15.2% YoY, driven by price hikes implemented to offset higher gas costs. Tile volumes are expected to grow by 5.5% YoY, supported by continued market share gains amid disruptions in the Morbi cluster. CRS is expected to deliver revenue growth of 13.3% YoY, led by ~17.0% growth in the faucets segment and ~14.0% growth in sanitaryware. EBITDA margin is likely to expand by ~40bps YoY to 13.1%, supported by price hikes that helped offset higher input costs.

Wood panel – Plywood continues to outperform:

CPBI is expected to deliver healthy sales growth of 16.7% YoY, with EBITDA margin of 12.0%. We expect MDF volume growth of ~25.0% YoY for CPBI and ~10.5% YoY for GP. Greenpanel's MDF volume is likely to remain relatively soft, due to elevated freight rates resulting from geopolitical tensions, which continue to weigh on export volumes, along with sustained competitive intensity in the industry. Plywood volume growth is estimated at +12.0% YoY for CPBI and 14.6% YoY for GP. CPBI’s laminate segment is likely to record single-digit volume growth of 5.5% YoY, impacted by geopolitical tensions affecting exports. Overall, the wood panel coverage universe is expected to report revenue growth of +14.6% YoY, while EBITDA is likely to increase by ~48% with margin expanding by 260bps to 11.7%.

TP changes:

We have revised downward our FY28 earnings estimates for Supreme Industries and Greenpanel Industries (GP), raised estimates for Kajaria Ceramics, and maintained estimates for the remaining companies in our coverage universe. We have retained our ratings across all companies under our building materials coverage. We maintain positive view on CERA, Astral and Supreme Industries over the medium to long term.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...