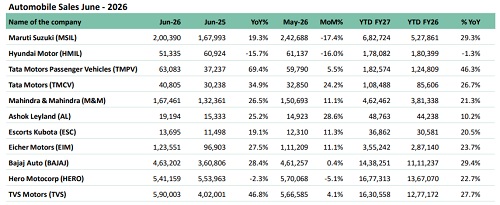

Monthly Auto Sales Update - June 2026 by ARETE Securities Ltd

Auto industry volumes eased 1% MoM in June, led by normalization in PV dispatches after a strong May, though volumes remained up 22% YoY with CV, 2W and tractors broadly resilient. CV volumes were strong across trucks, LCVs and buses, led by M&M and TMCV, reflecting broad-based demand strength. PV dispatches rose 24% YoY but eased 13% MoM, supported by SUV and EV traction; TMPV and M&M outperformed, while HMIL was impacted by a one-off supplier-led disruption. 2W volumes were flat sequentially but up 21% YoY, aided by premium motorcycles, rising EV penetration and record exports led by BAJAJ and TVS. Tractors improved on early kharif activity, though uneven monsoon progression and emerging El Niño risks temper near-term visibility. 3W volumes rose 23% YoY and 11% MoM, led by strong performance from TVS and M&M, while BAJAJ delivered steady gains in the segment. Industry exports rose 9% MoM and 38% YoY to ~26% of total volumes, with 2W and CV shipments scaling fresh highs, while PV and tractor exports remained relatively muted, keeping the sustainability of the current export mix dependent on agricultural conditions for tractors and global demand trends for 2W and CV exports.

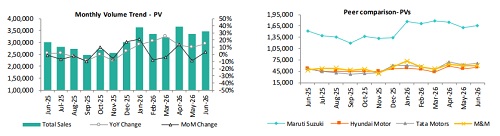

PV Segment

PV domestic dispatches rose 24% YoY but declined 13% MoM, benefiting from a favourable base, healthy retail demand and continued strength in SUVs and EVs. MSIL's domestic dispatches increased 21% YoY but normalized sequentially after an unusually strong May, while export volumes remained robust. TMPV outperformed peers with 67% YoY and 5% MoM growth, as EV volumes more than doubled alongside broad-based portfolio strength. M&M sustained momentum with 28% YoY and 4% MoM growth, led by continued strength in its SUV portfolio. In contrast, Hyundai's dispatches declined 10% YoY and 17% MoM amid June price hikes and supply disruptions. Exports remained broadly stable at the industry level, rising 1% YoY but declining 1% MoM, as a 13% YoY increase in MSIL's exports and a sharp recovery in TMPV shipments offset HMIL third consecutive month of declining export dispatches.

CV Segment

CV dispatches rose 16% MoM and 30% YoY, with growth driven by broad-based strength across all OEMs led by M&M and TMCV. Trucks, accounting for 61% of volumes, rose 17% m/m and 33% y/y, with M&M and TMCV remaining the key growth contributors. LCVs (18% mix) increased 13% MoM and 29% YoY, supported by AL and TMCV, while M&M remained largely stable sequentially. Domestic buses (14% mix) rose 18% MoM and 11% YoY, led by TMCV, although AL continued to decline on a high base despite sequential recovery.

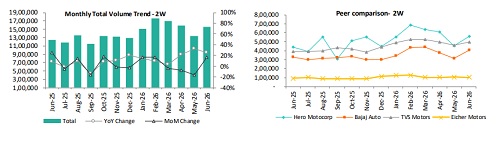

2W Segment

2W volumes remained flat sequentially while rising 21% YoY, supported by premium motorcycles and continued EV adoption. The e-2W segment recorded 1.93 lakh VAHAN registrations, with TVS, BAJAJ and HERO accounting for 24%/22%/11% share and 47.0k/43.2k/21.8k registrations, respectively. TVS and BAJAJ were the primary contributors in the segment in domestic dispatches where volumes rose 15% YoY to 11.84 lakh units but declined 3% MoM, with gains at TVS and EIM partially offsetting weakness at HERO and BAJAJ. Sequentially, gains at TVS and EIM offset lower dispatches at HERO and moderation at BAJAJ, keeping overall volumes broadly stable. Export momentum remained robust, with industry exports rising 44% YoY and 11% MoM, led by BAJAJ and TVS, with HERO contributing from a smaller base.

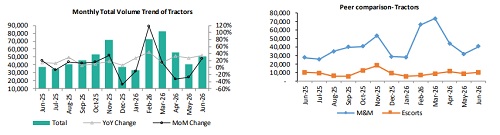

Tractor Segment

Tractor dispatches rose 19% MoM and 13% YoY, supported by early kharif activity and resilient rural demand despite uneven monsoon progression and emerging El Niño concerns. M&M domestic tractor volumes increased 12% YoY and 22% MoM to 58k units, while ESC domestic sales rose 20% YoY and 11% MoM to 13k units, with exports broadly steady as M&M exports grew 8% YoY to 1.8k units and total exports remained flat at 2.3k units. Overall tractor volumes stood at 73.6k units. Near-term demand remains contingent on monsoon evolution, with delayed rainfall posing risks to sowing and sentiment, partially offset by healthy reservoir levels and ongoing policy support

Please refer disclaimer at http://www.aretesecurities.com/

SEBI Regn. No.: INM000012

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...