Auto & Auto Ancillaries Sector Update : Demand rebound visible; potential margin expansion from H2 by Emkay Global Financial Services Ltd

Demand for Indian auto OEMs is returning after the brief Apr/May-26 disruption due to the West Asia crisis; the strong wholesale dispatch growth, robust Vahan retail registrations (across segments), healthy retail-to-dispatch ratio across OEMs (>95% in Q1FY26), and positive dealer commentary (also highlighted by FADA) all point to the recovery. Notably, despite the recent commodity-led price hikes, consumer prices are well below the pre-GST-cut levels which should continue to drive replacement demand, especially in 2Ws/MHCVs (2W/MHCV FY26 industry volumes only 4%/1% above their FY19 peaks). Further, electrification is at an inflection point, and the already-building up consumer pull (evident in the sustained 60-100% YoY EV industry retail growth during Q1FY27 and EV penetration at a fresh high across 2Ws/3Ws/PVs in Jun-26) is being reinforced by a regulatory push, (eg Delhi EV Policy 2.0)—this is likely to further boost the EV theme. Also, after a sustained rise from Q2FY26 to mid-Q1FY27, commodity prices have started correcting in Jun-26 and the historical precedent suggests that OEMs could witness margin expansion from H2FY27 (especially MHCVs/2Ws). Valuations across the pack now look favorable, with 2W/CV OEMs trading at their LTA and PV OEMs below LTA. Against this backdrop of strong demand/margin expansion (would drive a robust ~20% FY26-28E EPS CAGR for our OEM universe), we favor TMCV (BUY | TP Rs650), AL (BUY | TP Rs220), TVSL (BUY | TP Rs5,000), Ather Energy (BUY | TP Rs1,350), EIM RE (BUY | TP Rs8,700), M&M (BUY | TP Rs4,100), MSIL (BUY | TP Rs16,900)

Demand returning across segments despite commodity spike-led price hikes

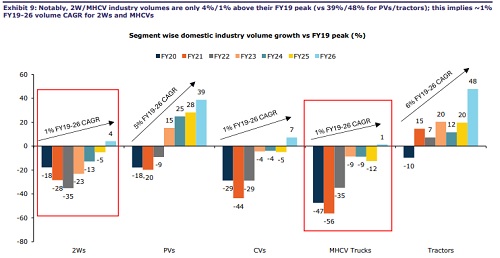

Following the momentary disruption in Apr/May-26 due to the West Asia crisis, the Indian auto OEMS are witnessing demand returning in Jun-26 which is being reflected in the strong growth in wholesale dispatches and Vahan retail registrations. This is supported by the retailto-domestic dispatches at >95% (across 2Ws, PVs, and MHCVs) in Q1FY26 as well as a positive dealer commentary (also evident in FADA’s May-26 survey: link). Notably, despite the recent commodity-led price hikes taken by OEMs (Exhibit 8), consumer prices remain well below pre-GST-cut levels (8-10% benefit due to GST cut). This favorable pricing gap is likely to continue driving a replacement cycle, with the effect more pronounced in 2Ws/MHCVs (FY26 industry volumes for 2Ws/MHCVs are 4/1% above their FY19 peaks vs 40/46% for PVs/Tractors implying a 1% FY19-26 volume CAGR for 2Ws/MHCVs vs 5-6% for PVs/Tractors)

Electrification at an inflection; consumer pull reinforced by regulatory push

Electrification is now at an inflection point, with strong demand being witnessed across segments (E-2W/E-3W/E-PV industry retail volumes have risen 60-100% YoY in Q1FY27). Notably, EV share is at a fresh high across 2Ws/3Ws/PVs (at 10.6%/47%/7.6%) in Jun-26, with acceleration in growth clearly visible across categories in recent months. The already evident consumer pull is also being reinforced by a regulatory push (refer to Delhi EV Policy 2.0 – A major step to accelerate electrification). We believe a cascading effect of this policy could offer further boost to electrification as a theme, with Ather as the key beneficiary (Yet another mega shift in motion; Ather – The frontrunner).

Margin recovery ahead, with commodity price correction underway

Following continued rise in prices since Q2FY26 (sharp spike, particularly in Q4FY2/early Q1FY27), commodity prices are now seen correcting (eg spot prices of brent crude/precious metals/aluminium 15-20% below Q1FY27 average). Previously, when the RM basket saw a continual price drop over Q4FY22-Q4FY24 (30-40% across MHCVs/2Ws/PVs), gross margin for OEMs saw strong improvement, with recovery particularly pronounced in MHCVs (600bps) and 2Ws (400bps) vs PVs (200-300bps). We believe with underlying demand momentum being robust, commodity prices easing and calibrated-price hikes in place, OEMs could witness margin expansion starting H2FY27.

Valuations favorable; prefer CV OEMs, TVSL, Ather Energy, EIM, M&M and MSIL

Auto stock prices have seen correction on concerns of slowing demand amid war-driven macro uncertainty and margin pressure from a spike in commodity prices. 1YF valuations for 2W/CV OEMs are now at their long-term average, while PV OEMs are trading below their long-term average. Against this backdrop, we favor TMCV (BUY | TP Rs650), AL (BUY | TP Rs220), TVSL (BUY | TP Rs5,000), Ather Energy (BUY | TP Rs1,350), EIM RE (BUY | TP Rs8,700), M&M (BUY | TP Rs4,100), and MSIL (BUY | TP Rs16,900). While valuations for Escorts are favorable (1SD below LTA), it lacks near-term trigger (the management has also highlighted a potential volume moderation in coming quarters

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

Tag News

Auto & Auto Ancillaries Sector Update : Growth momentum rebounding; electrification on the r...

More News

Consumer Durables Sector Update : Ear to ground: After a weak 2Q, green shoots visible by JM...