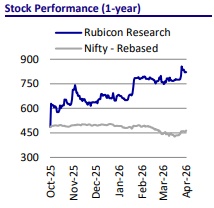

Buy Rubicon Research Ltd for the Target Rs.955 by Motilal Oswal Financial Services Ltd

Rubicon Research (Rubicon) aims to make inroads into the central nervous system (CNS) therapy in India’s branded market (DF) through Arinna Lifescience (Arinna).

* While Arinna’s products will be added to the portfolio, the key advantage of this acquisition would include gaining access to an established network of distributors, stockists, and retail pharmacies in India, along with a strong prescriber base. We find this acquisition to be a logical move, as it provides Rubicon’s innovative US pipeline of commercialized as well as under-development products with access to a key market in the form of India.

* This provides a strong foundation in the branded domestic CNS formulation market. Further, Rubicon has a proven track record of acquiring capabilities/capacities and scaling them to deliver exponential, profitable growth through integration with its existing business.

* In the PR release, management has flagged off that US revenues have grown 32x over the past decade. We note that a decade ago, the company lacked balance sheet cash as well as business scale, and was yet to fire up its R&D engine. In the past decade, the US market went through a challenging macro environment on compliance and pricing, despite which Rubicon achieved 32x revenue growth with best-in-class return ratios.

* In that light, given that Rubicon today is a well-scaled, cash-generating machine, with its R&D engine firing solidly (which provides the opportunity to bring innovative products to India), we believe that the optionality of a substantial scale-up in the coming decade in the acquired Indian business should not be ignored by investors.

* The strong execution track record and foray into the CNS DF market warrant a higher valuation multiple, rather than bucketing its valuation with conventional US generics companies.

* We raise our P/E multiple to 37x (from 35x earlier) to factor in the potential upside from this acquisition. Accordingly, we revise our TP to INR955. Reiterate BUY.

CNS entry via Arinna: Established foothold in Indian branded CNS therapy

* Arinna, incorporated in 2013, is a branded pharmaceutical marketing company focused on CNS and neuro-psychiatric therapies, with a portfolio of 60+ brands and 140+ SKUs across chronic segments.

* Its <b style='mso-bidi-font-we

Rubicon Research (Rubicon) aims to make inroads into the central nervous system (CNS) therapy in India’s branded market (DF) through Arinna Lifescience (Arinna).

* While Arinna’s products will be added to the portfolio, the key advantage of this acquisition would include gaining access to an established network of distributors, stockists, and retail pharmacies in India, along with a strong prescriber base. We find this acquisition to be a logical move, as it provides Rubicon’s innovative US pipeline of commercialized as well as under-development products with access to a key market in the form of India.

* This provides a strong foundation in the branded domestic CNS formulation market. Further, Rubicon has a proven track record of acquiring capabilities/capacities and scaling them to deliver exponential, profitable growth through integration with its existing business.

* In the PR release, management has flagged off that US revenues have grown 32x over the past decade. We note that a decade ago, the company lacked balance sheet cash as well as business scale, and was yet to fire up its R&D engine. In the past decade, the US market went through a challenging macro environment on compliance and pricing, despite which Rubicon achieved 32x revenue growth with best-in-class return ratios.

* In that light, given that Rubicon today is a well-scaled, cash-generating machine, with its R&D engine firing solidly (which provides the opportunity to bring innovative products to India), we believe that the optionality of a substantial scale-up in the coming decade in the acquired Indian business should not be ignored by investors.

* The strong execution track record and foray into the CNS DF market warrant a higher valuation multiple, rather than bucketing its valuation with conventional US generics companies.

* We raise our P/E multiple to 37x (from 35x earlier) to factor in the potential upside from this acquisition. Accordingly, we revise our TP to INR955. Reiterate BUY.

* CNS entry via Arinna: Established foothold in Indian branded CNS therapy

* Arinna, incorporated in 2013, is a branded pharmaceutical marketing company focused on CNS and neuro-psychiatric therapies, with a portfolio of 60+ brands and 140+ SKUs across chronic segments.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041