Buy Piramal Pharma Ltd for the Target Rs. 250 by Motilal Oswal Financial Services Ltd

Operationally, in-line 4Q; FY25 ends on a strong note

Targeted initiatives to strengthen segment-wise performance

* Piramal Pharma (PIRPHARM) delivered in-line sales/EBITDA in 4QFY25. However, its earnings were below our estimate due to impairment of certain intangible assets during the quarter.

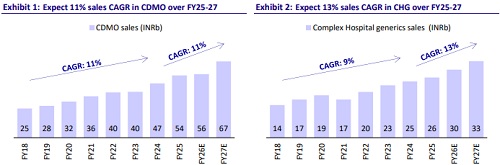

* After eight quarters of strong high-teens YoY growth in the CDMO business (65% of 4Q sales), PIRPHARM witnessed some moderation in growth for this segment. Having said this, there has been a surge in on-patent commercial manufacturing business within the CDMO segment (USD179m in FY25 vs. USD116m in FY24).

* The company exhibited moderate performance in the complex hospital generics (CHG) segment for 4QFY25/FY25. This was mainly due to a pricing pressure on Sevoflurane.

* PIRPHARM delivered robust growth in the India Consumer Health (ICH) segment (up 15% YoY) in 4QFY25, on the back of new launches and market share gains in existing products.

* We cut our earnings estimate by 47%/33% for FY26/FY27, factoring in 1) inventory normalization for one product in the CDMO segment, 2) inconsistent recovery in funding biotech projects, thus affecting the outlook of the CDMO business, and 3) lower operating leverage. We value PIRPHARM on an SoTP basis (17x EV/EBITDA for CDMO business, 12x EV/EBITDA for CHG business, and 13x EV/EBITDA for consumer health (ICH) business) to arrive at a TP of INR250.

* While FY26 would be the year of consolidation in revenue for PIRPHARM, it continues to invest in a) potential areas like ADCs/peptides/sterile injectables within the CDMO segment, b) capacity expansion in the CHG segment, and further improvement in profitability in the ICH segment. Accordingly, we build ~3x earnings over FY25-27. Reiterate BUY.

Segmental mix impact more than offset by higher operating leverage

* PIRPHARM’s 4QFY25 revenue grew 8% YoY to INR27.5b (in line). The CDMO segment’s revenue rose 8% YoY to INR17.9b. The CHG segment’s revenue (26% of total sales) grew 4% YoY to INR7.1b. ICH (9% of total sales) revenue increased 15% YoY to INR2.7b during the quarter.

* Gross margin expanded 510bp YoY to 65.3%.

* However, the EBITDA margin contracted 40bp YoY to 20.4% (in line) primarily due to lower operating leverage (employee costs/other expenses up 290bp/260bp as a % of sales).

* EBITDA grew 6% YoY to INR5.6b (in-line).

* PAT grew 34% YoY to INR1.5b (our est: INR1.9b) for the quarter, owing to lower tax burden (44% of PBT in 4QFY25 vs. 56% of PBT in 3QFY25).

* While revenue and EBITDA were in line with our estimates, PAT was much lower due to an impairment charge of INR447m for the quarter.

* In FY25, the company’s revenue/EBITDA/PAT grew 12%/21%/62% YoY to INR91b/INR14.4b/INR0.9b.

Highlights from the management commentary

* Considering the inventory normalization for the products in the CDMO segment, management guided a mid-single-digit YoY growth in revenue with mid-teens EBITDA margin for FY26.

* PIRPHARM expects significant improvement in revenue growth and EBITDA margin, reaching 19-20% in FY27 based on the order book in the CDMO segment and improved traction in the CHG and ICH segments.

* PIRPHARM maintained its guidance of USD1.2b revenue with a 25% EBITDA margin in the CDMO segment by FY30.

* The company witnessed a significant increase in the order book for the ADC segment within the CDMO space.

* Capex would be USD100-125m for FY26, including capacity expansion at the Lexington/Riverview site (USD90m).

* PIRPHARM has 75%/44% market share in Baclofen/Sevoflurane in the US.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412