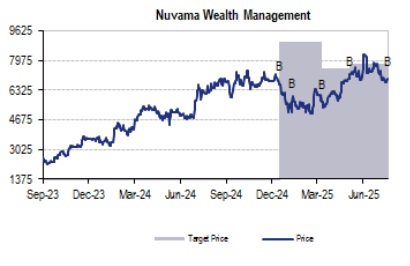

Buy Nuvama Wealth Management Ltd for the Target Rs. 8,100 by JM Financial Services Ltd

Nuvama reported strong results with a PAT of INR 2.6bn (+3.4% QoQ, +19.5% YoY), in line JMFe [link to first cut]. Despite weak 1Q inflows in Private segment, management maintained its guidance of 25-30% of ARR AUM as inflows, translating into INR 190bn for FY26e. Basis mgmt. commentary, we estimate the total impact of the regulatory action on Jane Street to be limited to 5% of FY25 PAT in FY26e, should it not resume trading. We cut our FY26e EPS by 1% but maintain key FY27, FY28 estimates. Key data points shared on granularity of business provides comfort on sustained growth and we revise our Target Price to INR 8,100 (up from INR 7,800), valuing the franchise at a blended 22x FY27e EPS. We reiterate BUY.

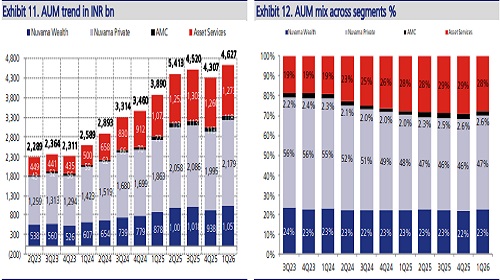

* Steady growth outlook despite headwinds: Management highlighted granularity of the business in concall – if Jane Street does not resume trading, growth outlook in asset services reduces to early double digits from high teens. Further, FY26 PAT from IE business may fall by INR 150-INR 160mn over FY25. Total derivatives revenues (not including asset services) were quantified at INR 28 - 30bn, ~10% of FY25 revenues. Meanwhile, in the wealth business, mgmt. remains confident of 25-30% levels of net inflows. We believe even on the strong base of capital markets in FY25, the company should drive 12% EPS growth in FY26e, before recovering to 23% levels over FY27/FY28e.

* Cost to Income Ratio sustaining at these levels can lead to EPS upgrades for FY26e: In concall, mgmt. highlighted that income from insurance and transactions was seasonally weak in 1Q, still blended CIR improved both sequentially and on a YoY basis. If both these income streams grow substantially as the year progresses, CIR can improve hereon, posing an upside risk to our EPS growth estimates. Given the upfront RM additions over 2HFY24 – FY25, we expect the company to deliver ~100bps YoY improvement in CIR annually in near term in the wealth business. We are circumspect of the CIR in capital markets business – which is subject to volatile revenue growth. With the RM additions and weak growth in capital markets (on a strong base) in FY26, we expect blended CIR to increase in FY26e from FY25 levels, before an improvement of 100bps/150bps in FY27/FY28e.

* Valuations and view – appreciate the granularity of the business, raise TP, reiterate BUY: Nuvama has delivered strong gains since its listing in Sep’23, however, recent performance has been muted with concerns over derivatives and asset services businesses. We estimate a 12% FY26e EPS growth on the back of 103%/55% growth in FY24/FY25, before recovering to 23% levels over FY27-FY28e. We value the company’s wealth management revenues at 26x FY27e EPS, capital markets at 17x and the AMC at 18x – we get a blended multiple of 22x FY27e EPS. With an FY27e EPS of INR 375, we get a Target Price of INR 8,100 at 22x P/E. We reiterate BUY.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361