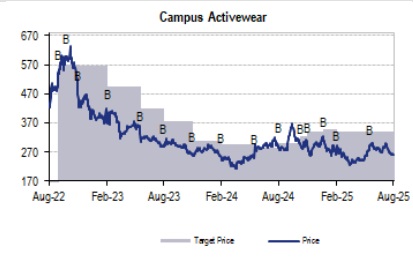

Buy Campus Activewear Ltd for the Target Rs. 310 by JM Financial Services Ltd

Revenue grew only 1% YoY despite a weak base, resulting in 5% miss to our estimates. Growth was impacted due to consolidation of the three warehouses and implementation of SAP software, leading to loss of 15-20 days of sales. Owing to this, the D2C online channel registered sales decline of 13% YoY due to supply related constraints while the company stocked the inventory at the distributor level and offline channel in 4Q. Barring this abnormality, overall sales growth would have been in high single digits. ASP growth was robust at 15% YoY led by (i) higher sneaker sales, and (ii) lower DIP school shoes and slippers segment, resulting in 12% volume decline; however, this resulted in gross margin expansion of ~160bps. Negative operating leverage resulted in ~90bps contraction in EBITDA margin. Warehouse consolidation and SAP implementation may have posed some hindrance to nearterm growth but will help in capacity addition and margin improvement. We cut our EPS estimates by 2-5% to bake in the 1Q miss and also cut our P/E multiple from 50x to 45x as revenue performance remains sub-par despite a weak base (4% CAGR over FY23-25). We maintain BUY with a revised TP of INR 310 as we roll forward to 45x Jun’27 EPS

* Miss on all grounds: Net revenue increased 1% YoY to INR 3.4 bn (5% below our estimates) led by loss of 15 days of sales due to (i) implementation of SAP software, and (ii) consolidation of three warehouses. EBITDA fell 5% YoY to INR 493mn (14% below JMFe) as EBITDA margin contracted ~90bps YoY to 14.4% (JMFe: 15.8%) despite ~160bps gross margin expansion to 54.6% (JMFe: 52.5%) due to ~90/160bps YoY higher employee/other expense. APAT declined 13% YoY to INR 222mn (13% below JMFe) as interest and depreciation increased 33%/24% YoY partially offset by 170% YoY higher other income

* Online channel declined 13% YoY; Volume fell 12%, while ASP grew 15% YoY: D2C online channel revenue declined 13% YoY while Trade distribution/D2C offline revenue grew 9%/27% YoY. Volume declined ~12% YoY to 5.1mn pairs while ASP increased 15% YoY to INR 671. Higher ASP is led by (i) increasing salience of sneakers, which garners higher ASP by INR 200 vs. company average, and (ii) reduced salience of DIP school shoes and slippers (lower ASP items) by transitioning to EVA category shoes. Share for premium products (above INR 1,500) increased to 50%+, which is highest ever for the company.

* Building blocks for future growth: The company undertook consolidation of its three warehouses into one warehouse. This will increase its product handling capacity from 80k pairs to 200k pairs. It will provide bandwidth to the company to feed RM to 50 more fabricators. This, however, impacted 15-20 days of online sales in 1Q. It also implemented SAP during the quarter due to which a blackout was observed in 2nd week of Apr’25 (period shorter than expected). Predicting this, the management stocked up the inventory in 4Q at the wholesale channel. The company is strengthening the supply chain through warehouse consolidation and SAP implementation, whose benefits are expected in terms of margin expansion in upcoming years.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361