Buy Fujiyama Power Systems Ltd for the Target Rs. 340 by Motilal Oswal Financial Services Ltd

An integrated B2C play on India’s rooftop solar boom

UTLSOLAR is an integrated B2C rooftop solar solutions provider offering a wide range of products, including inverters, solar panels, batteries, chargers, and solar management systems. As of Dec’25, the company has scaled the capacity of solar panels, batteries, and power electronics to over 1.5GW each.

* UTLSOLAR is expanding capacity to tap India’s ~100GW rooftop solar opportunity by FY30. It plans an INR3b capex for panels, inverters, and batteries at Ratlam, taking the capacity to 3.7GW/3.7GW/3.8GWh. Moreover, the company has backward-integrated into solar panels by setting up a 1GW domestic content requirement cell (DCR) capacity in Jan’26 (51% gross margins).

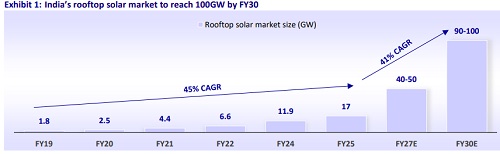

* The PM Surya Ghar Muft Bijli Yojana (PMSGMBY) scheme targets 10m installations of residential rooftop systems by FY27. So far, 2.9m households (~10.4GW, ~3.6kW per home) have been covered, leaving ~7.1m installations (~26GW potential) untapped. Eligibility requires DCR-compliant materials, driving UTLSOLAR’s in-house cell plant at Dadri and, thus, supporting growth potential.

* India is shifting from tubular to Li-ion batteries due to their longer life, lower maintenance, and better long-term efficiency. As such, UTLSOLAR plans to expand its Li-ion capacity from 45MWh to 2.5GWh (from FY25) by 1QFY27. Further, growth in rooftop solar solutions is driving a planned 2GW greenfield inverter facility at Ratlam (total capacity of 3.7GW).

* The company is largely a B2C player (~90%), with a rapidly expanding pan-India distribution network of ~900 distributors, ~6.3k+ dealers, and ~1.1k+ franchiseled UTLSOLAR shoppes. Network scaling has been driven by its twin-brand strategy, deeper geographic penetration, and expansion into underpenetrated southern and eastern states.

* We expect UTLSOLAR to deliver strong growth (56%/65%/65% CAGR in revenue/EBITDA/PAT over FY25–28), driven by PMSGMBY-led demand and capacity expansion. We value it at 15x FY28E EPS with a TP of INR340 and a BUY rating.

Robust manufacturing footprint led by backward integration

* UTLSOLAR runs four well-placed manufacturing units across Himachal Pradesh, Uttar Pradesh, and Haryana, and plans to add a new greenfield facility in Ratlam by 1QFY27 to enhance market access and efficiency. ? India’s rooftop solar market is projected to scale to ~100GW by FY30, driven by policy support, subsidies, declining battery costs, rising power tariffs, ESG commitments, and tech advancements.

* To capitalize on this demand, UTLSOLAR plans a major capacity expansion of 2GW each in solar panels/inverters/lithium-ion batteries at Ratlam (INR3b capex), taking total capacity to 3.6GW/3.7GW/3.8GWh in each.

* Further, to tap rooftop solar opportunity and comply with the DCR cells policy, the company has commissioned 1GW of backward-integrated solar cell capacity (~50% of panel cost). We expect the company to add 2GW capacity to achieve full backward integration in solar panels.

* Our scenario analysis indicates that in-house DCR solar cell manufacturing is the most value-accretive, potentially lifting gross margins to ~51% vs ~27%/~23% for outsourcing. Although realizations may fall from INR25/W to INR18/W in the medium term, margins are expected to moderate to ~32% but remain superior to outsourced DCR levels.

* This has resulted in the expansion of solar cell manufacturing for the industry from 30MW in CY22 to ~23GW in Dec’25. Further, capacity is expected to expand from 23GW to 110GW by FY27/FY28 (up 5x), according to data provided by various companies, led by superior economics and increasing demand for solar cells (dependent on margin viability and demand parity in the industry).

* Overall, the superior economics of DCR solar cells have driven rapid capacity build-up and wider industry participation, underscoring a structural shift toward backward integration and a more robust domestic solar manufacturing ecosystem in India.

Leveraging lithium-ion momentum with power electronics expertise

* India is shifting from tubular batteries to Li-ion batteries. Despite higher upfront costs, Li-ion batteries offer longer life, lower maintenance, and superior longterm cost efficiency, driving their growing adoption.

* As such, UTLSOLAR plans a significant capacity expansion from 45MWh in FY25 to 2.5GWh by 1QFY27. While capacity will be added upfront, utilization will ramp up in stages based on demand.

* The company has developed strong expertise in power electronics and technology. It has achieved key milestones, such as launching single-card online UPS, combo UPS, and patented rMPPT (Maximum Power Point Tracking) technology.

* The growth in rooftop solar solutions is also driving growth for solar inverters. Supported by growth in solar inverters, UTLSOLAR plans to expand capacity by adding a 2GW greenfield solar inverter facility in Ratlam by 1QFY27.

* Overall, the company is well-placed to benefit from rising lithium-ion battery demand and growth in integrated solar-storage solutions, supporting sustained growth and a stronger competitive position.

Rooftop solar opportunity backed by policy support

* The PMSGMBY scheme targets to install 10m solar rooftops in the residential sector by FY27, benefiting residential households, group housing societies, and residential welfare associations. Installations were expected to exceed 4m by Mar’26 (~2.9m installed as of 15th April), with the remaining 6m installations expected by Mar’27.

* Eligibility requires Indian citizenship, home ownership with a suitable rooftop, and a valid electricity connection. Further, applicants must not have availed prior solar subsidies and must use DCR-compliant materials. Benefits offered under the scheme are discussed in Exhibit 22.

* Despite strong policy support, execution is still at an early stage. Only ~56% of the target market has been applied for and ~29% of households are covered, leaving ~7.1m installations as a large untapped opportunity.

* As of 15th Apr,’26, ~10.4GW capacity has been installed across 2.9m households. With an average of ~3.6KW per household, the remaining ~7.1m installations imply ~26GW of additional capacity potential.

* The company previously relied on non-DCR cells for off-grid solar panel manufacturing. To tap this opportunity, it is sourcing from DCR-compliant vendors and has commissioned an in-house DCR cell plant at Dadri in Jan’26.

* With its established track record and integrated product portfolio, UTLSOLAR is well-positioned to capitalize on the accelerating adoption of rooftop solar and translate policy support into sustained growth going forward.

Expanding distribution network with twin-brand presence

* The company is largely a B2C player (~90%), supported by a pan-India distribution network. This includes ~900 distributors, 6.3k+ dealers, and ~1.1k+ exclusive shoppe franchisees (by FY26E), with distributors also serving large industrial orders.

* The distributor base grew ~65% from ~482 in Sept’24 to ~800 in Sept’25. Total channel partners more than doubled from ~3.7k in FY23 to ~8.2k by Dec’25, while untapped states reduced from over 13 in FY22 to 10 in FY25, indicating deeper penetration.

* This expansion is supported by a twin-brand strategy—UTLSOLAR and Fujiyama Solar. It allows two distributors in the same city, improving market penetration, brand visibility, and channel reach.

* Further, the company has increased its distributor presence in states including Tamil Nadu, Telangana, Karnataka, Kerala, Andhra Pradesh, and Odisha, and aims to increase distributors in these regions to 104 by FY26E from 42 in FY23.

* The company follows a franchise-led retail model (shoppe), offering end-toend rooftop solar solutions. Its separate project sales division enables the execution of large-scale projects and partnerships without channel conflict.

* Overall, the company’s twin-brand strategy, expanding network, and focused sales structure create a scalable go-to-market model. This strengthens market reach and execution across both retail and project segments.

Valuation and view: Initiate coverage with BUY and a TP of INR340

* UTLSOLAR’s growth is driven by the PMSGMBY scheme and its in-house DCR plant, supporting demand capture. Backward integration boosts margins, while expansion into Li-ion and inverters and a growing distribution network strengthen its market reach.

* In the absence of a direct listed peer, the company is valued using an equalweighted mix of consumer durables, solar, and battery peers. Factoring in company’s relatively modest scale, we apply a ~37% discount to the ~24x FY28 average P/E, the company is valued at 15x FY28E EPS.

* UTLSOLAR delivered strong growth with a CAGR of 45%/78%/76% in revenue/EBITDA/Adj PAT over FY22–25. It is expected to post a CAGR of 56%/65%/65% over FY25–28 and currently trades at 27x/16x/11x FY26E/FY27E/FY28E EPS, with RoE/RoCE of 33%/28% in FY28E.

* We value the company at 15x FY28E EPS with a TP of INR340 and a BUY rating.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412