Technology Sector Update : ER&D Services: Q1FY27 Quarterly Results Preview by Choice Institutional Equities

Automotive Weakness Deepens; FY27 Recovery Deferred

Automotive demand in Europe weakened materially in Q1FY27, reversing the stabilisation seen over recent quarters. Profit warnings across global OEMs and renewed cost-rationalisation initiatives have resulted in delayed engineering programs, slower deal ramp-ups and selective project cancellations. Engineering spends continue to shift from new platform development towards sustaining existing portfolios, as OEMs prioritise near-term returns amid rising competitive pressure from Chinese manufacturers.

Demand remains relatively resilient across Aerospace, Communications, Sustainability Engineering and AI-led industrial automation, although these verticals will not be able to offset weakness in Automotive. Semiconductor engineering demand remains healthy; however, recent acquisitions are expected to remain margindilutive over the near term. We expect FY27 to remain another muted year for the ER&D sector, with industry growth likely limited to 0.5– 4.4% YoY, while recovery shifted to H2FY27-H1FY28 and there we cut our FY2027-28E revenue by 0.6-7.9% and fair values by 14-28%

Revenue Expectations Reset; KPIT Leads the Downgrade Cycle

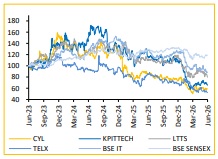

Q1FY27 is likely to be another weak quarter across our ER&D coverage. KPITTECH's pre-announced ~1% YoY/ ~4.5% QoQ USD revenue decline materially resets sector expectations, highlighting the sharp pullback in European automotive spending. TELX is expected to report flat growth (+0.3%) led by Media & Healthcare, while CYL DET (-1.7%) is likely to witness sequential decline owing to Energy & Mining weakness. LTTS is expected report stable revenue (+0.4%), supported by Sustainability Engineering and diversified exposure, although elongated deal conversion cycles continue to constrain growth

Margin Diverge; Weak Operating Leverage Persists

Margin performance is expected to remain mixed. LTTS should deliver modest sequential expansion, while CYL (DET) margin is likely to remain stable despite weaker revenues. TELX is expected to report margin contraction owing to continued investments in AI capabilities and talent, whereas KPITTECH is likely to witness disproportionate margin compression following significant revenue decline. Overall, favourable currency and cost optimisation should only partially offset weak operating leverage.

View: Recovery Deferred; Stay Selective

The sharp correction across ER&D stocks has reset valuations, but earnings risk remains inclined to the downside as recovery in automotive engineering spend continues to be deferred. While the slowdown is cyclical rather than structural and long-term drivers, such as SDVs, AI-led engineering and semiconductor R&D remain intact, discretionary automotive R&D budgets are likely to stay constrained as OEMs prioritise cost-optimisation and capital discipline. We continue to prefer companies with diversified vertical exposure, superior execution and resilient margin. LTTS and KPITTECH remain our preferred ideas within the ER&D space.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

More News

Auto Sector Update : Q4FY26: Healthy demand trends sustain amid rising cost pressure Choice ...