Accumulate Acutaas Chemicals Ltd For Target Rs.3,773 by Prabhudas Liladhar Capital Ltd

Preparing for new frontiers

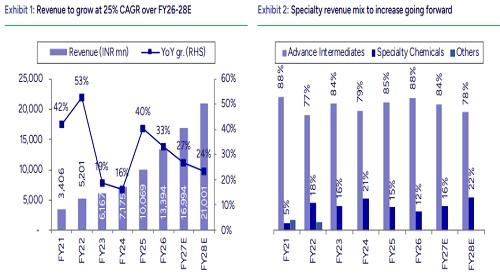

We initiate coverage on ACUTAAS with ‘Accumulate’ rating and TP of INR3,773, based on 56x FY28E EPS. Over the last 5 years, the company has delivered a strong growth track record, with revenue/EBITDA/PAT CAGR of 32%/43%/46%. We expect the growth trajectory to sustain, with revenue/EBITDA/PAT projected to grow at 25%/24%/24% CAGR over FY26–28E, led by the ramp-up of the Fermion contract, commercialization of 4 additional CDMO molecules, and increasing contribution from battery and semiconductor chemicals. Supported by strong process chemistry capabilities, backward integration, and expanding presence in high-entry-barrier specialty chemicals, ACUTAAS is well placed to deliver sustained earnings growth. At CMP, the stock trades at 52x FY28E EPS and 38x FY28E EV/EBITDA; we are positive on its growth visibility and improving business mix. However, considering the recent sharp rally in the stock, further upside would be subject to timely execution of projects. Initiate with ‘Accumulate’.

Strong leadership in the pharma intermediates market:

Advanced Pharma Intermediates segment contributed to ~88% of revenue in FY26 and is expected to deliver 18% CAGR over FY26-28E, supported by rising CDMO exposure, increasing innovator partnerships, and upcoming patent expiries of blockbuster molecules such as apixaban and rivaroxaban (Expired).

CDMO – The key growth catalyst:

The CDMO business is expected to be ACUTAAS' key long-term growth driver, supported by high regulatory entry barriers, long-term contracts, and superior margins. Its 10-year supply agreement with Fermion Oy is expected to drive the majority of CDMO revenue, with the management guiding ~INR10bn revenue by FY28E. The opportunity is backed by Nubeqa's strong commercial trajectory, with peak sales guidance raised to ~EUR3bn and patent protection extending to CY33-35. Additionally, 4 new CDMO molecules are expected to start contributing from H2FY27, with an INR500-1,000mn peak revenue potential for each.

Battery chemicals – A new growth avenue:

ACUTAAS is leveraging its strong chemistry capabilities to establish its presence in the fast-growing global battery chemicals market. The company has developed 9 electrolyte additive molecules and is commissioning 2,000mtpa each of VC and FEC under its ~INR1.77bn Phase I capex. Phase II is expected to add 2 more products by H2FY27, further expanding the product portfolio. Phase I alone has a peak revenue potential of ~INR3.8bn, supported by customer approvals and contracted volumes, with EBITDA margin expected to be in the ~15% range.

Foray into high-entry-barrier semiconductor chemicals market:

ACUTAAS entered the high-entry-barrier semiconductor chemicals market through the acquisition of 55% stake in Baba Fine Chemicals (BFC) in FY24 for INR682mn (4x FY23 adjusted EBITDA). Leveraging BFC's expertise in ultra-high-purity photoresist chemicals, the company is expanding beyond its historical single-customer model. Further, its ~INR2bn South Korea JV is expected to be commissioned by Dec'26, positioning ACUTAAS closer to key semiconductor customers and creating a scalable platform for long-term growth.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271