Automobiles and Auto Ancillaries Sector Update : Delhi EV Policy 2.0: Aggressive mandate, contained impact by Elara Capital

The Delhi Cabinet has approved a new EV Policy, succeeding the 2020 framework, committing ~INR 150bn over four years and targeting EVs at 95% of new personal vehicle registrations by 2027. This is among India’s most aggressive state-level mandates, with a strict BEV focus that excludes strong hybrids. We see limited impact on listed OEMs: Delhi is just 1-4% of pan-India volumes, readily offset by EV sales and NCR spillover. Eicher (RE) is the key name to monitor — its exposure is ~4%, unlike scooter-led peers, it lacks an EV line-up currently to recapture lost ICE volumes; and motorcycle acceptance in EVs is yet to be proven; though the company has couple of more years to address this. We view the policy as a net positive for EV-focused plays — Ather (NR) and ancillaries, Minda Corp, Sona BLW and UNO Minda. The policy should sustain EV momentum, support our FY30 penetration targets of 15%/20% for PVs/2Ws, and likely expedite massmarket EV motorcycle launches in the next two years. Key monitorable is whether other states follow Delhi's lead, though we see no near-term signs of this. Our top picks among OEMs are MSIL, TVSL, EIM, Hyundai, M&M with any correction a buying opportunity

Front-loaded incentives, firm phase-out deadlines:

The policy pairs purchase and scrappage-linked incentives with hard registration cut-offs. On the demand side, e-2Ws qualify for up to INR 30,000 in Year 1 (tapering thereafter to INR 20K in year 2 and INR 10K to year 3), e-3Ws up to INR 50,000, and N-1 goods vehicles up to INR 100,000, each with additional scrappage benefits. Passenger cars get no direct subsidy but a scrappagelinked benefit of up to INR 100,000 plus full road-tax and registration exemption (for EVs up to INR 3mn). On the phase-out, only electric auto-rickshaws can be registered from 1 January 2027, and new petrol/CNG 2W registrations cease entirely from 1 April 2028.

OEM volume impact contained at 1-4%; Eicher, the key name to watch for

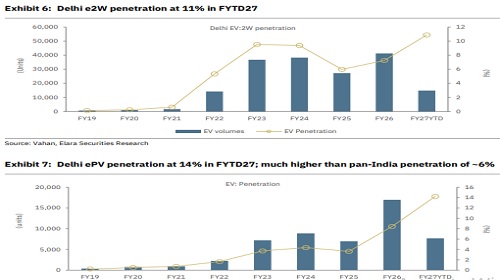

Delhi's contribution to pan-India volumes is modest – ~3-4% for PV OEMs, 1-4% for 2W OEMs and ~2% for 3W OEMs — limiting the impact. For 2W players such as TVS and Bajaj, the lost ICE volumes are readily absorbed by their expanding EV portfolios (as also current absence of HMSI in EV scooters; and ~20% Delhi market share). Eicher (RE) Delhi contribution is at ~3-4%, and unlike scooter-led peers, it lacks an EV line-up currently to recapture banned ICE volumes from FY29. Further, Delhi’s scooterization is on the higher side at ~44% versus India’s 39%, which has a higher EV penetration. This is a marginal negative for HMCL as its scooter market share is only 3% in Delhi versus 7% in India and much lower than motorcycle pan-India market share of ~42%

MSIL, TVSL, EIM, Minda Corp, Sona and Uno Minda, our top picks:

While the loss of volume for 2W OEMs seems in the range of 1-4%, we see this as easily offset by EVs. RE ‘s EV product launch acceptance will be keenly monitored (~4% volume exposure) and the likely ICE ban from FY29 will remain an overhang on valuation multiple, on fears of other states following a similar policy. However, we see key EV focused OEMs (Ather – Not Rated) to be a direct beneficiary of this. For PVs, rise in EV contribution will be a positive for M&M and TMPV. That said, as highlighted in our recent note, EV Adoption: The resurgence, EV-focused auto ancillary names such as Sona BLW, Minda Corp and Uno Minda will be direct beneficiaries of higher EV adoption, as it will lead to premiumization trends and higher content per vehicle.

Please refer disclaimer at Report

SEBI Registration number is INH000000933