Buy Rites Ltd For Target Rs.275 by Prabhudas Liladhar Capital Ltd

Execution-led growth with sustainable margins

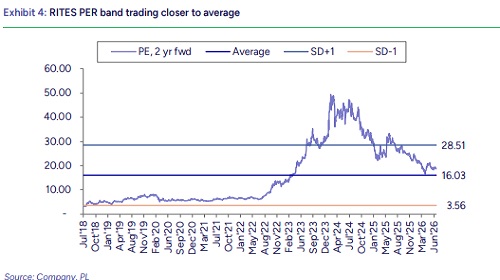

We hosted RITES management for an NDR, where management reiterated its confidence in the medium-term growth outlook, supported by a relatively young order book, with around two-thirds of projects (12–18 months old) entering the execution phase over FY27–28. The company targets an order book of INR 100 bn by FY27-end, with at least 80% of new orders through competitive bidding, and guides for 10–20% revenue growth, while PAT growth is expected to trail initially as EBITDA margins normalize from the historical 27–28% to a sustainable 18–20%, with a minimum 15% PAT margin. The company also highlighted its record export order book of INR 21 bn, comprising INR 17.5 bn in rolling stock and INR 3.5 bn in consultancy, providing strong execution visibility through projects in Bangladesh, Mozambique, South Africa, Guyana and Nepal. We continue to like RITES for its asset-light business model, negative working capital cycle and expected ~19% RoE by FY28E. We model a 16% revenue CAGR over FY26–28E and, maintaining our 25x FY28E P/E, retain BUY with a target price of INR 275, along with an attractive 4–5.0% dividend yield.

FY27 / FY28 targets:

We hosted RITES management for NDR, where-in management indicated that around two-thirds of the order book is relatively young (12–18 months old), providing strong revenue visibility as these projects enter the execution phase in this and next year. The company aims to expand its order book to INR 100 bn by FY27- end, with at least 80% of orders secured through competitive bidding. Revenue growth is guided at 10–20% YoY, while PAT growth is expected to lag initially as margins normalize from the historical 27–28% EBITDA level to a more sustainable ~20%, with management maintaining a minimum annual PAT margin of 15%. As execution scales up, higher revenues are expected to offset the margin reset, enabling the company to deliver absolute earnings over time.

Margin normalization driven by business mix:

Long-term margin profile will be driven by the evolving business mix, with pure consultancy projects generating EBITDA margins of around 30% (vs. 40%+ historically), turnkey projects at ~2%, and exports and leasing delivering intermediate margins at 10-15%, resulting in a blended EBITDA margin of 18– 20%. The company expects the share of competitively bid orders to remain around 75– 80% (with a minimum target of 80%), while the balanced mix of nomination and competitive orders is expected to support the targeted margin floor.

Record export order book with strong execution visibility:

The export order book stands at an all-time high of INR 21 bn, comprising INR 17.5 bn in rolling stock and INR 3.5 bn in project consultancy, providing healthy medium-term execution visibility. Mozambique coach order was fully executed in FY26, contributing around INR 3 bn of export revenue after nearly a two-year gap. The rolling stock order book includes INR 9.5 bn for 200 passenger coaches in Bangladesh, INR 2 bn for five new locomotives in Mozambique (awarded in Q4), and ~INR 6 bn for the conversion of 30 Indian Railways broad-gauge locomotives to Cape gauge, primarily for South Africa. The INR 3.5 bn project consultancy order book comprises infrastructure assignments such as a highway project in Guyana, an airport project in Nepal, and an Integrated Check Post (ICP) in Nepal, with project durations of 2.5–3 years and 1–2 years of execution remaining.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271