2025-08-29 05:08:30 pm | Source: Motilal Oswal Financial Services

Buy EPL Ltd for the Target Rs. 280 by Motilal Oswal Financial Services Ltd

Margin expansions in Europe and the Americas drive

profitability In-line operating performance

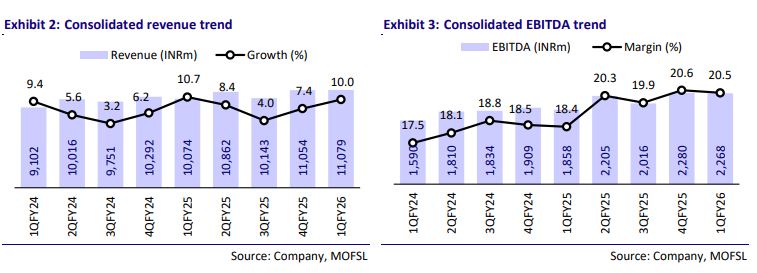

- EPL reported an EBITDA of INR2.3b (+22% YoY) in 1QFY26, in line with our estimate. This was driven by EBITDA growth across all regions, with Europe/America/EAP/AMESA witnessing a growth of 52%/35%/8%/2% YoY.

- EPL continued its trajectory of margin expansion (up 200bp YoY), supported by gains in Europe and the Americas. This was fueled by strategic restructuring, cost optimization, and an improving mix of the personal care segment in the overall portfolio (~54% in 1QFY26 vs. ~47% in 1QFY25).

- We maintain our estimates for FY26/FY27 and value the stock at 17x FY27E EPS to arrive at our TP of INR280. Reiterate BUY.

Product mix continues to improve and boost operating performance

- EPL’s revenue grew ~10% YoY to INR11b (in line). Gross margin expanded 70bp to 60%. EBITDA margin expanded 200bp YoY to 20.5% (est. 20.4%), led by improving margins in the Americas and Europe.

- The company’s EBITDA stood at INR2.2b (est. in line), up 22% YoY. Adj. PAT grew 56% YoY to INR1b (in line).

- Revenue from the Americas/Europe/EAP/AMESA grew 13%/15%/10%/2% YoY to INR2.9b/INR2.7b/INR2.6b/INR3.7b.

- EBITDA margin improved 300bp/400bp for the Americas/Europe to 18.8%/ 17.9%, while EBITDA margin for AMESA remained flat at 19%, and that of EAP contracted 30bp YoY to 21.6%.

- EBITDA for Americas/Europe/EAP/AMESA grew 35%/52%/8%/2% YoY to INR551m/INR478m/INR420m/INR714m during the quarter.

Highlights from the management commentary

- Guidance: EPL expects to maintain double-digit revenue growth, with EBITDA growth expected to be higher than revenue growth, driven by strong traction in the Beauty and Cosmetics (BNC) segment and the anticipated recovery in the oral care segment.

- Expansion: EPL has doubled its capacity in the BNC segment in Brazil, and this expansion is expected to enable the company to onboard new clients in the region. The Thailand plant is set to commercialize from 2HFY26.

- Personal care and beyond: Management is actively pursuing M&A opportunities in the BNC segment, targeting both geographic and product expansion. The growth momentum in the BNC segment is expected to continue, led by new customer additions due to capacity expansions.

Valuation and view

- EPL continues to deliver healthy operating performance across geographies, supported by a favorable product mix, product innovations, an improving sustainable mix (38% of total volume), and continued capacity expansion. We expect this positive trend to continue.

- With improved operational efficiencies, a focus on improving market share across geographies in the BNC segment, and a recovery in the Oral Care segment, we expect a CAGR of 9%/14%/22% in revenue/EBITDA/adjusted PAT over FY25-27. We value the stock at 17x FY27E EPS to arrive at our TP of INR280. Reiterate BUY.

Highlights from the management commentary Operating performance

- EPL delivered a strong revenue growth of 10.0% driven by double-digit growth in the Americas, Europe, and EAP.

- Strong momentum in ‘Personal Care & beyond with ~28% growth powered by the growth of beauty and cosmetics (up 35% YoY)

- Margin expansion in America and Europe was driven by the successful execution of strategic initiatives.

- Recyclable volumes are scaling up rapidly, with sustainable tubes now accounting for over one-third of the portfolio. Guidance and outlook

- Management remains confident of its double-digit revenue growth guidance, led by the company’s strategic focus and execution discipline.

- EBITDA is expected to grow faster than revenue, with PAT projected to outpace EBITDA growth.

AMESA

- Strong growth in Beauty & Cosmetics is offsetting the softness in oral care demand.

- The management anticipates the Oral care segment to bounce back in 2HFY26

- Oral care is showing signs of improvement, which, along with sustained momentum in Beauty & Cosmetics, is expected to support growth going forward.

- In India, tube revenue growth outpaced overall growth, led by the improving demand for laminated tubes.

EAP

- Robust growth in the quarter was driven by strong performance across the portfolio.

- The Thailand greenfield plant remains on track for commercialization by the second half of FY26.

- The Thailand project was executed with the support of Indorama, which played a key role in securing necessary permits on time, enabling the project to stay on schedule.

- The capex for the Thailand facility is ~USD5m. The company plans to start at a smaller scale and gradually ramp up operations, with margins expected to be in line with those in other global regions.

- The company has a strong pipeline of products in the Beauty & Cosmetics category in Thailand and plans to commence operations quickly, with a fast ramp-up of product lines.

- Thailand is a significant tube market where EPL currently holds a small share, primarily serving the region through its China facility.

- Following the launch of the Thailand facility, the company will be wellpositioned to service additional geographies such as Vietnam, Singapore, Malaysia, and Indonesia.

Americas

- Continued double-digit performance with strong revenue delivery across countries.

- The Brazil capacity expansion was completed by the end of 1QFY26.

- The region continues to witness strong momentum in the Beauty & Cosmetics segment.

- Brazil continues to deliver strong growth; the recently completed capacity expansion is expected to support the onboarding of additional customers.

- The Brazil plant has been operating at high utilization levels, with capacity in the Beauty & Cosmetics segment now doubled. Europe

- Robust revenue growth of over 15% was driven by strong momentum in the Beauty & Cosmetics segment.

- The company has made key changes and strengthened its sales resources, which have begun to deliver tangible value to the business.

- The company is actively exploring M&A opportunities in Europe.

- The opportunity to expand business in this geography remains significant, given the company’s currently low market share in the region.

Personal care and beyond

- The Personal Care and Beyond category, which includes Beauty & Cosmetics and Pharma, contributed 54% to the overall portfolio in 1QFY26.

- Management is actively pursuing M&A opportunities in the Beauty & Cosmetics segment, targeting both geographic and product expansion.

- Growth in the Beauty & Cosmetics segment is expected to continue, driven by its significant potential and the management’s focus on disciplined execution.

- New customer acquisitions have been a key driver of growth in the Beauty & Cosmetics segment, and the company will continue to target smaller customers to further expand its market share.

Oral Care

- The decline in oral care was due to category softness in AMESA and a few other markets, but the management anticipates a bounce back in 2HFY26

- Toothpaste remains a resilient category; the current softness is viewed as temporary and is expected to rebound.

Others

- The company is well geographically diversified across its portfolio, and despite softness in certain regions, it remains confident in achieving its overall growth objectives.

- The tax rate for the quarter may be impacted by the revenue mix, with an expected range of 18-20%, largely depending on the geographical distribution of revenue.

- This year, the overall tax rate could be slightly lower due to a higher contribution from low-tax geographies.

- The company only imports laminates into the U.S., and any cost increases are passed on to customers through contractual agreements.

- There is no competition with Indorama, as both companies operate in different product segments and instead share synergistic opportunities.

- The company plans to incur a CAPEX of ~INR3.5b-INR4b, roughly equal to the depreciation.

Valuation and view

- EPL continues to deliver healthy operating performance across geographies, supported by a favorable product mix, product innovations, an improving sustainable mix (38% of total volume), and continued capacity expansion. We expect this positive trend to continue.

- With improved operational efficiencies, a focus on improving market share across geographies in the BNC segment, and a recovery in the Oral Care segment, we expect a CAGR of 9%/14%/22% in revenue/EBITDA/adjusted PAT over FY25-27. We value the stock at 17x FY27E EPS to arrive at our TP of INR280. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Buy Cyient Ltd for the Target Rs 830 by Motilal Oswa...

The Art of Slow Living: Why Slowing Down Can Improve...

Government institutes framework to strengthen cybers...

Over 77 lakh annual FASTag passes issued, register 6...

Quote on Technical Market Commentary for July 22nd, ...

Maruti Suzuki India to hike car prices by up to Rs 3...

Buy Mahindra Logistics Ltd For Target Rs. 507 by Pr...

Women's Short and Stylish Kurti: The Perfect Blend o...

Resistance : 24150 (Pivot Level) and 24300 (Key Resi...

Economic activity posted strong expansion in June 20...