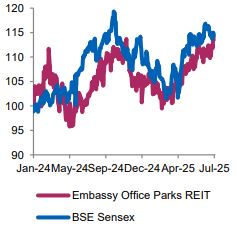

Buy Embassy Office Parks REIT Ltd for Target Rs. 450 by Axis Securities Ltd

Resilient Growth Backed by Record Leasing; Strong Fundamentals

Changes in Estimates post Q1FY26

FY26E/FY27E: Revenue: 1%/(0.3)%; EBITDA: 1%/(0.3)%; PAT: 0.3%/(10.4)%

Recommendation Rationale

• Strong Operating Metrics; High Quality Tenant base: Embassy REIT reported a 13% YoY increase in revenue to Rs 1,060 Cr, supported by a 7% growth in leasable area and a 100 bps improvement in occupancy. Net operating income (NOI) rose 15% YoY to Rs 872 Cr. Distribution per unit (DPU) came in at Rs 5.8, marking a 4% YoY increase led by robust leasing and contributions from Embassy Splendid Techzone. It continues to demonstrate robust leasing momentum, backed by demand from GCCs, healthcare, and technology firms. With 2 Mn sq. ft. leased in Q1—its best-ever start to a fiscal year—the REIT has shown resilience amid global uncertainties. The high re-leasing spread (38%) indicates strong pricing power, especially in core markets like Bangalore and Chennai.

• Strong Leasing Performance and Strategic Divestment: The REIT recorded gross leasing of 2 Mn sq. ft. in Q1FY26, across 25 deals. Embassy recorded its best-ever Q1 leasing, comprising 1 Mn sq. ft. at a healthy 38% re-leasing spread, 0.4 Mn sq. ft. of renewals and 0.7 Mn sq. ft. in pre-commitments. Occupancy improved to 88% by area, and 91% by value, with 10 out of 14 properties now above 90%. Embassy’s strategic divestment of ~0.37 Mn sq. ft. of strata-owned blocks at Embassy Manyata executed at a 2.2% premium to independent valuation, not only eliminating operational inefficiencies but also freeing up capital for higher-yielding opportunities or debt repayment. Financially, the transaction supports portfolio quality enhancement with minimal income loss (only ~Rs 8 Cr in annual rents) while strengthening the REIT’s already solid balance sheet, reflected in its low leverage ratio of 33% and declining cost of debt, now at 7.6% post-refinancing.

• 13% NOI Growth Target for FY26E from Vacancy Lease-Up and Expansion: For FY26, Embassy REIT has reaffirmed its guidance, projecting Net Operating Income (NOI) in the range of Rs 3,589–3,811 Cr, representing a 13% YoY growth at the midpoint, and a DPU of Rs 24.5–26, implying a 10% annual increase. The REIT expects portfolio occupancy to reach 90–91% by area and 93–94% excluding the underperforming Quadron asset in Pune. As of Q1FY26, it has already made strong progress toward this goal, achieving record leasing of 2 Mn sq. ft., with 84% of its 3.2 Mn sq. ft. scheduled FY26 completions already pre-leased. Key assets like Block 10 in Chennai (430,000 sq. ft.) have been fully pre-leased, and Embassy Manyata’s Block D1 and D2 (Q4 delivery) have reached 80% precommitment, reinforcing visibility on upcoming income streams and positioning the REIT well to meet its full-year targets.

Sector Outlook: Positive

Company Outlook & Guidance: We remain positive about the company’s long-term prospects.

Current Valuation: 28x FY27E EPS (Earlier: 28X FY27 EPS)

Current TP: Rs 450/share (Earlier TP: Rs 450 /share).

Recommendation: With a 14% upside from the CMP, we maintain our long-term BUY rating

Financial Performance

The company reported revenue of Rs 1,060 Cr for the Q1FY26, up 13% YoY. EBITDA stood at Rs 821 Cr, and margins stood at 77.4%. PAT was recorded at Rs 155 Cr. Distribution was at Rs 550 Cr, DPU of Rs 5.8/unit. Record leasing activity with 2 Mn sqft leased across 25 deals, marking the highest ever Q1 leasing volume.

Outlook

Embassy enters FY26 with strong momentum, driven by record leasing activity, robust operating metrics, and a high-quality tenant base. The REIT's best-ever Q1 leasing performance, combined with a 38% re-leasing spread and rising occupancy, shows sustained demand across its core markets. Strategic asset divestments have further strengthened the balance sheet while unlocking capital for future growth. With over 80% of upcoming completions already pre-leased and NOI guided to grow 13% YoY, Embassy is well-positioned to deliver on its FY26 targets. Overall, the outlook remains resilient and growth-oriented, even amid global macro uncertainties.

Valuation & Recommendation

• We continue to value the company by applying a 28X multiple to FY27E EPS of 16.1, arriving at a TP of Rs 450, implying an upside of 14%.

• Key Highlights •

Asset Recycling: Divesting 0.37 Mn sq. ft. in Embassy Manyata (strata-owned blocks) at 2.2% above independent valuation due to high capex and vacancy.

• SEZ De-notification: Total of 7.8 Mn sq. ft. de-notified so far; 74% of which is leased. Further 3.2 Mn sq. ft. under the de-notification pipeline.

• Macro Outlook: Market leasing momentum remained strong at 20 Mn sq. ft. pan-India absorption in Q1. Rental rates are growing by 5– 7%, supported by an active leasing pipeline of 1.5 Mn sq. ft. Chennai and Bangalore remain key leasing drivers.

• Debt Raised: Company raised Rs 4,225 Cr debt at 7.18% coupon, Rs 750 Cr NCD at 6.97% – lowest in 4 years. Net debt stands at Rs 20,183 Cr and leverage at 33%.

Key Risks to Our Estimates and TP

• Economic slowdown may impact the company’s profitability.

• Low rental yields going forward will result in a fall in occupancies.

• An increase in debt levels may impact the company’s profitability

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home SEBI Registration number is INZ000161633