Buy Brigade Enterprises Ltd For Target Rs.1,540 by Motilal Oswal Financial Services Ltd

Strong performance even after approval delays

Bangalore and Chennai to drive growth; 12msf launch pipeline creates growth visibility for near term

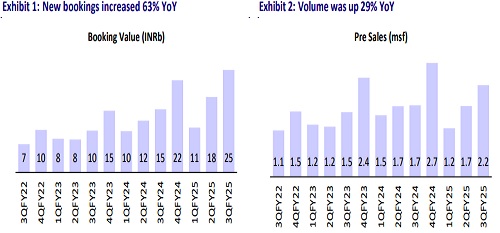

Brigade Enterprises (BRGD) reported bookings of INR24.9b in 3QFY25, up 63% YoY (in line with the estimate). Volume was up 29% YoY at 2.2msf.

* With launches of 1.9msf projects in Bengaluru, Hyderabad, and Mysore, BRGD recorded its highest-ever quarterly realization of INR11,364/sft, up 26% YoY.

* The company intends to launch ~12msf of residential projects in Bangalore (9 projects), Chennai (4 projects), Hyderabad (1 project), and Mysuru (2 projects) in the next four quarters.

* In light of this growth, we expect BRGD to deliver 32% CAGR in pre-sales over FY24-26E to INR105b.

* BRGD’s consolidated collections rose 27% YoY to INR17.8b (vs. MOFSLe of INR21b).

* For 9MFY25, BRGD achieved pre-sales of INR54b, up 43% YoY. Collections improved 31% YoY to INR53b.

* BRGD's gross debt was INR45.3b, while net debt was INR11.3b. Its net debt to equity stood at 0.18x by end-3QFY25; the cost of debt was 8.76%.

P&L performance

* Revenue grew 25% YoY to INR14.6b (9% above our estimate). For 9MFY25, BRGD achieved revenues of INR36.1b, up 13.1% YoY, 73% of our full-year estimate.

* EBITDA stood at INR4.1b, up 58% YoY (in line with our estimate). EBITDA margin came in at 28.3%, up 594bp YoY, while it was lower by 374bp against our estimates. For 9MFY25, the company reported an EBITDA of INR10b, up 31% YoY. Its EBITDA margin stood at 27.3%.

* For 3QFY25, BRGD's adj. PAT jumped 221% YoY to INR2.4b, reporting a margin of 16%. During 9MFY25, it reported an adj. PAT of INR4.4b, up 79% YoY.

Annuity business reports healthy growth

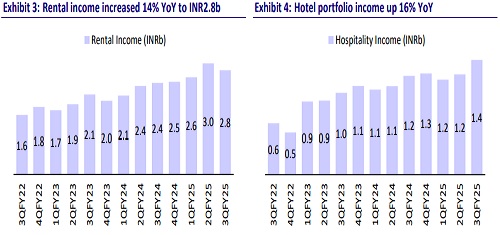

* Leasing revenue grew 14% YoY to INR2.8b and the hotel business reported INR1.3b revenue, which rose 16% YoY.

* Over the last few quarters, the company has made good progress in the commercial portfolio’s occupancy, which rose to 98% by 3QFY25 from 86% in 1QFY24.

* The company has 2.67msf of Office and Retail area under construction. It has a balance capex commitment of INR7.1b out of a total ongoing capex of INR12.5b for commercial assets.

Valuation and view

* BRGD reported a decent quarter even after approval delays, guided by strong demand for its recently launched projects across its core markets. However, it has a strong launch pipeline of ~12msf, which should enable it to sustain the growth traction going ahead.

* The management intends to keep assessing growth opportunities in the residential segment and expects to spend higher on business development over the next two years. This will provide growth visibility in the residential segment and lead to a further re-rating. We reiterate a BUY rating with a TP of INR1,540, implying a 32% potential upside.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412