Buy Accumulate HCL Technologies Ltd for the Target Rs.1,910 by PL Capital

Strong performance, deal wins lays foundation for sustainable momentum

Quick Pointers:

* Increased Consol. Rev. guidance to 4-4.5% YoY CC & Services revenue guidance to 4.75-5.25% YoY CC

* Robust Deals wins of USD 3.06 bn compared to USD 2.57 bn in Q2

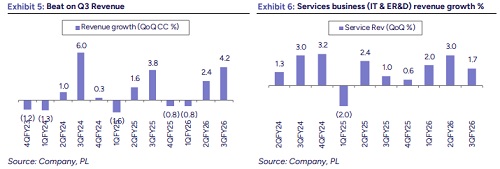

The revenue growth performance (+4.2% QoQ CC) was above our estimates (+3.0% QoQ CC), aided by strong seasonality of HCLSoftware (+28.1% QoQ CC). Services business performance was also strong (+1.8% QoQ CC) defying the furloughs and holidays impact. The service business growth was majorly led by ER&D segment that reported another quarter of strong growth (+3.1% QoQ CC vs 2.2% QoQ CC LQ). The service-led growth was largely aided by extop 20 accounts (+2.3% QoQ), which implies the decision making and execution cycle remains strong at the lower-end of the pyramid. Again, the advanced AI revenue growth (19.9% QoQ CC) is largely a component of short-burst deals that further validates the velocity of smaller deal remains strong. The new deal TCV reported at USD3.0b, which includes one of the mega deals (USD473m) of five-year strategic engagement. We believe the service-led growth should continue its momentum in FY27/FY28 on the back of strong order wins and growing AI revenue stream. Hence, we are revising the topline CC growth upward by 30bps/20bps to 7.0% and 7.7% for FY27E/FY28E. Despite the beat on margins in Q3, we expect Q4 will see some normalization, while additional new labour code would also keep the margin in check. The stock is currently trading at 22x and 19x FY27E/FY28E EPS. We assign 22x to FY28 EPS to arrive at a TP of 1,910.

Revenue: HCLT delivered a robust performance in Q3, reporting 4.2% QoQ CC growth, materially ahead of our estimate of 3.0% and the consensus estimate of 2.8% QoQ CC. Despite furloughs, Services business posted steady growth of 1.8% QoQ CC, with IT Services growing 1.4% QoQ CC and ER&D reporting a stronger 3.1% QoQ growth. Software segment reported robust growth of 28.1% QoQ CC and 3.1% YoY CC.

Margins: EBIT margin (excluding restructuring expense of 0.81%) expanded 150 bps QoQ to 19.4%. Services margins were largely stable, with ~10 bps improvement in IT Services offset by a ~90 bps decline in ER&D, while the Software segment saw a sharp ~860 bps QoQ margin expansion. At the consolidated level, margins benefited from ~120 bps contribution from Software, ~110 bps from higher utilization, and ~40 bps currency tailwinds, partly offset by wage hike (~80 bps) and furlough (~50 bps) headwinds.

Guidance: Following a strong Q3 performance, HCLT raised its FY26 revenue guidance to 4.0–4.5% YoY CC for the consol. business and to 4.75–5.25% CC growth for the Services segment, excluding the impact of announced acquisitions. The company maintained its EBIT margin guidance of 17–18% for FY26.

Valuations and outlook: We are baking in USD revenue/Earnings CAGR of 7.5%/13.3% between FY26E-28E. We are assigning a PE multiple of 22x to FY28E earnings and arrive at a TP of INR 1,910. We maintain our BUY rating.

Above views are of the author and not of the website kindly read disclaimer

.jpg)