Accumulate HCL Technologies Limited for Target Rs. 1419 by Religare Broking Ltd

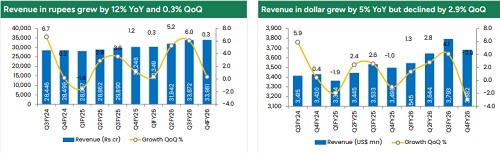

Financial Performance Stable but Moderating Growth: HCL Technologies Ltd reported a steady Q4 FY26, with revenue at Rs.33,981 crore, growing 12.3% YoY, while PAT rose 4.2% YoY to Rs.4,490 crore. However, sequential performance remained muted, with USD revenue declining 3% QoQ due to seasonal weakness in the software segment. EBIT margins came under pressure, declining to 16.5%, impacted by operating leverage and changes in business mix. Full-year FY26 revenue stood at $14.7 billion, growing 3.9% in constant currency. Overall, the performance reflects resilience in a challenging macro environment, while also highlighting a slowdown in discretionary IT spending and softer deal conversions in certain verticals.

Segment Performance Services Strong, Software Weak: The services segment remained the primary growth driver, growing 4.1% in Q4 FY26, supported by steady demand in digital engineering and cloud services. However, the software business declined 4.1% YoY, largely due to seasonality and delayed procurement decisions. Within verticals, Technology & Services led growth with 24.1% YoY expansion, while Financial Services remained stable. The telecom segment continued to lag, declining 2.2% YoY due to reduced spending from key global clients. This divergence between services strength and software weakness indicates a mixed demand environment, where core IT services remain resilient but product-linked revenues face near-term pressure.

AI Strategy Emerging as a Core Growth Engine: HCL Technologies Ltd’s AI-led transformation is becoming a central pillar of its growth strategy. The company reported an annualized AI revenue run rate exceeding $620 million, with nearly all new deals incorporating AI or GenAI components. Its five-pillar AI approach includes proprietary platforms like AI Force, industry-specific IP development, and expansion into AI-native services such as AI factories and physical AI solutions. Strategic partnerships with global leaders like Google, Microsoft, Nvidia, and OpenAI further strengthen its positioning. Additionally, large-scale talent upskilling, with over 135,000 employees trained in GenAI, ensures strong execution capability, positioning HCL Tech competitively in the evolving AI-driven IT services landscape.

Deal Wins and Order Pipeline Strong Visibility: HCL Tech maintained strong deal momentum with Q4FY26 TCV at $1.94 billion, taking the full-year deal wins to $9.3 billion. This robust pipeline provides medium-term revenue visibility despite short-term headwinds. The company continues to win large transformation deals, including high-value AI-led engagements exceeding $100 million. However, execution timelines remain slightly elongated due to delayed client decisionmaking and macro uncertainties. While the deal pipeline remains healthy, conversion into revenue could be gradual. This indicates that while demand exists, clients are cautious in ramping up spending, especially in discretionary areas, impacting near-term revenue acceleration.

Margins Headwinds and Capital Allocation: Margins remained under pressure due to wage inflation, lower utilization in certain segments, and an adverse business mix. Q4 EBIT margin declined to 16.5% (reported), reflecting these headwinds. Additionally, the company faces a structural challenge from “AI-led deflation,” which is expected to reduce pricing by 2-3% annually. On the positive side, HCL Tech continues to reward shareholders aggressively, with a total FY26 dividend of Rs.60 per share and a payout ratio of 97.6%. The company has also extended its capital allocation policy, committing to return at least 75% of net income, reinforcing its strong cash flow generation and shareholder-friendly approach.

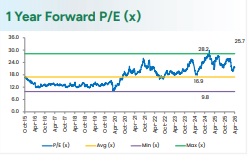

Outlook & Valuation: Looking ahead, HCL Technologies Ltd has guided for conservative FY27 revenue growth of 1-4% in constant currency, with services expected to grow slightly faster. EBIT margins are projected in the 17.5-18.5% range, indicating stability but limited expansion. The cautious outlook reflects macro uncertainty, weak discretionary spending, and ramp-downs from key clients. From a valuation perspective, the stock remains reasonable compared to peers, supported by strong dividends and consistent cash flows; however, meaningful upside will depend on acceleration in AI-led revenue and a recovery in global IT spending, making it a steady but not high-growth play in the near term. We estimate Revenue/EBIT/PAT CAGR of 7.5%/8.1%/8.2% over FY26–28E and maintain an ACCUMULATE rating with a target price of Rs.1,419.

Please refer disclaimer at https://www.religareonline.com/disclaimer

SEBI Registration number is INZ00017433