Sell HCL Technologies Ltd For Target Rs.1,200 by Elara Capital

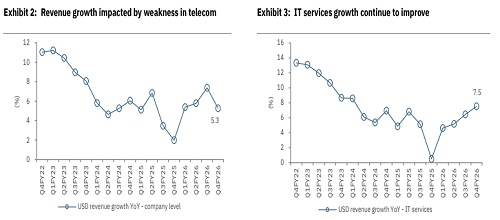

FY26 revenue growth guidance missed

HCL Technologies (HCLT IN) reported a weak Q4 on both revenue and margin fronts. Revenue declined 3.3% QoQ in CC, steeper than market expectations. This was due to: i) discretionary spending cuts in two large telecom clients, and ii) discontinuation of SAP programs in one manufacturing and one retail client. Management expects weakness in telecom clients to continue in CY26. As a result of weak Q4, HCLT missed its FY26 revenue growth guidance, and ended FY26 at 3.9% revenue growth in CC versus guidance of 4-4.5% growth. The company is now guiding for 1-4% revenue growth in CC in FY27. The company guiding 17.5-18.5% EBIT margins in FY27. We maintain SELL with TP lowered to INR 1,200 (from INR 1,270) on 18x (unchanged) FY28E P/E.

Products business – Seasonality, a drag on growth: HCLT reported revenue de-growth of -3.3% QoQ in CC terms and 2.4% in USD terms. IT services (75% of the mix) reported 0.6% QoQ growth in USD and 0.1% in CC. ER&D posted a -1.3% QoQ CC drop, while Products business (8.3% mix) was down 28.1% QoQ in CC terms. Vertical-wise, in USD QoQ, Tech and BFSI reported growth in the range of 1.2-4% QoQ while Retail, Telecom, Life sciences and Manufacturing reported sequential decline. Geography wise, in USD QoQ, the US market reported 0.2% growth while Europe contracted 2.0% in Q4FY26. New deal TCV wins were weak at USD 1.9bn in Q4FY26, down 35% on both QoQ and YoY basis. Advanced AI revenues were at USD 155mn in Q4FY26 (6.2% of revenue), but growth rate has moderated to +6.2% QoQ CC. HCLT declared an interim dividend of INR 12 per share in Q4, taking the total FY26 dividend to INR 54 per share, with a payout ratio of 88%.

Margin contracted due to seasonality in P&P: Q4 EBIT margin came in at 16.5% at the company level, pressured by a 181bps QoQ drag from seasonality in the software domain and delayed deal closures. Services margin declined by 27bps mainly due to the second wage hike cycle (-45 bps), along with restructuring costs (-41 bps) and higher bad?debt provisions (-19 bps). These were partly offset by productivity gains at Project Ascend (+13 bps) and favorable FX (+65 bps). For FY27, HCLT has guided to 17.5%-18.5% EBIT margin. Currency gains are planned to be reinvested into sales and GenAI capabilities.

Maintain SELL with a lower TP of INR 1,200: Q4 revenues were unusually weak and considering sustained weakness in some of the clients for the full calendar year, these will have a bearing on full-year revenues. Management assumes continued softness in discretionary spending at the lower end of the revenue growth guidance and expects a moderate pick-up in discretionary spending at the higher end of the guidance. We are considering median revenue growth, i.e., 2.5% in FY27E and ~2% in FY28E. Earnings growth adjusted to one time labor code over FY26-28E is likely to be ~2.0% CAGR. We revise our earnings estimates downwards by 3-5% for FY27E/28E to reflect weak Q4 and FY26 for the company. We maintain SELL with a lower TP of INR 1,200 (unchanged 18x FY28E EPS) from INR 1,270. Better-than-expected revenue and earnings growth are key risks to our call.

Please refer disclaimer at Report

SEBI Registration number is INH000000933