Reduce Torrent Power Ltd For Target Rs. 1,333 By JM Financial Services

2QFY26: Excluding the one-off gain, it is in-line

Torrent Power (TPW) in 2QFY26 reported revenue of INR 79bn (10% YoY, 6% JMFe, 3% Cons.) due to one-off higher merchant sales (c. INR 3 bn) during the quarter, excluding which revenue is in-line (6% YoY, 2% JMFe, -1% Cons.). EBITDA came in at INR 15bn (25% YoY, 6% JMFe, 10% Cons.). Adj. PAT stood at INR 7.2bn (50% YoY, 4% JMFe, 13% Cons). The increased utilization of gas-fired power plants and the trading of gas have driven the otherwise stable performance of the company in recent quarters. As demand for power remains subdued, we expect company’s gas-fired power plants to remain underutilised in near to medium term. Earnings visibility from the new capacity additions from RE, storage and likely new thermal are back ended. We estimate company to report FY25-28 CAGR of 9% / 13%/ 5% in Revenue/ EBITDA/ PAT largely driven by addition in RE capacity. As per our new rating system, we downgrade stock to REDUCE from HOLD with SOTP based TP of INR 1,333.

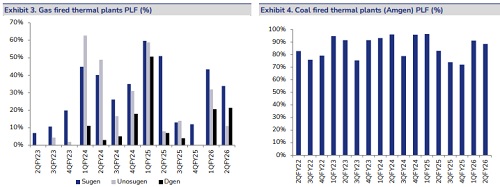

* Generation: Generation stood at 3,148 MU vs. 3,009 in 2QFY25. The PLF of thermal plants moderated- 1147.5MW Sugen (34% / 51% in 2QFY26 / 2QFY25); 382.5MW Unosugen (11% / 8% in 2QFY26 / 2QFY25); 1200MW Dgen (21% / 7% in 2QFY26 / 2QFY25) and 362MW Amgen (89% / 83% in 2QFY26 / 2QFY25). Contribution from renewable segment improved due to solar capacity additions resulting in PLF for wind / solar at 30% / 16% in 2QFY26 vs. 32% / 13% in 2QFY25.

* Capacity: Torrent added just 81 MW of solar capacity during 2Q, taking aggregate installed generation capacity to 4,961 MW (2,730 MW gas, 362 MW coal, 949 MW solar, 921 MW wind). Further, under construction capacity stands at 5,170 MW (1721MW / 1849MW / 1600MW of Solar / Wind / Coal) taking the total portfolio capacity to 10,131MW.

* MP Thermal Project: The company is setting up a 2x800MW Ultra Supercritical power plant in Madhya Pradesh, based on the LOA received from MP Power Management Company Ltd (MPPMCL) for power procurement at a tariff of INR 5.83/unit. Coal for the plant will be supplied by MPPMCL under the SHAKTI Policy. The project is expected to be commissioned within 72 months from the date of the PPA. The total capex is estimated at ~INR 220bn. The majority of the land has been acquired. The Boiler-Turbine-Generator (BTG) package has been awarded (management has not shared the vendor’s name) while the ordering for balance of plant is at an advanced stage.

* Pumped Hydro Storage: The company is developing a 3,000MW pumped storage project (PSP) in Raigad district, Maharashtra, at an estimated cost of INR 140bn. A 40-year PPA for 2,000MW/16,000MWh has been signed with MSEDCL, with commissioning expected in Oct’28. The project is estimated to generate annual revenue of INR 1.7bn. The company has received environmental clearance and the contracts for civil, electrical, and hydro-mechanical works have been awarded. Additionally, around 8.4GW of PSP capacity is under the planning stage across Maharashtra and Uttar Pradesh.

* Capex: In 1HFY26, company reported capex of INR 37bn (INR 25bn on renewables). For FY26, management has guided capex of INR 70-80bn.

* Transmission opportunities: Leveraging its rich experience, the company has ventured, afresh in the transmission business. The current portfolio includes transmission lines spanning a total of 483 km along with under-pipeline lines of ~104 kms (capex, INR 13bn). Given the limited number of players and large pipeline of bids in the next 6-8 months, we believe company will leverage the opportunity by selective participation in TBCB biddings and can also evaluate brownfield opportunities to strengthen the presence.

* T&D losses: T&D losses in license business of Ahmedabad were 5% / 4.5% and Surat were 3.6% / 3.3% during 2QFY26 / 2QFY25. Whereas in the franchise business T&D losses were – 10.3% / 10.9% in Bhiwandi, 11.4% / 10.7% in Agra and 24% / 28.4% in SMK during 2QFY26 / 2QFY25.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361