Oil & Gas Sector Update : OMCs - not out of the woods yet by PL Capital

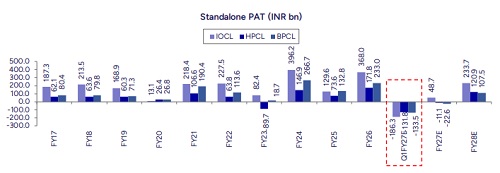

After 3.5 months of one of the worst energy shocks in recent history, we see some positivity as the US-Iran ceasefire deal finally gets signed, although uncertainty remains, especially over the nuclear deal. Brent crude dropped below ~USD80/bbl, its lowest level since Mar’26, providing a positive respite for OMCs. Q1FY27 is expected to weigh sharply on profitability, impacting earnings for the full year. We expect an under-recovery of Rs7.0/ltr and Rs10/ltr in Q1FY27, after considering a Rs10/ltr excise cut and capping of cracks at USD10/bbl and USD15/bbl for MS and HSD respectively. Additionally, LPG continues to remain a key pain point, with losses estimated at around Rs500/cyl for Q1FY27. As per Q4FY26 concall, OMCs reported LPG under-recoveries in the range of Rs610-670/cyl in May’26 vs ~Rs170/cyl in April’26. Saudi CP prices for Q1FY27 are expected to increase by ~47% QoQ, driven by supply constraints due to the West Asia disruption. The overhang of a rollback in excise duty cuts of Rs10/ltr remains a key pressure point for OMCs, although the rollback is expected to happen in a phased manner. If the US-Iran situation progresses positively and full normalcy is restored at the Strait of Hormuz, crude prices may soften further. However, we expect crude oil prices to rise again as countries are expected to replenish inventories and SPRs to maintain optimum resource levels, creating incremental demand in the market. As a result, we downgrade IOCL & BPCL to “Reduce” and HPCL to “Hold” from “Accumulate” as near-term earnings visibility remains weak. We lower the multiples accordingly from 0.8x, 1.2x, and 1.3x to 0.7x, 1.1x, and 1.2x based on FY28E PBV, arriving at a TP of INR126/384/291/share for IOCL/HPCL/BPCL respectively

GMMs expected to remain under pressure in Q1FY27

Q1FY27 has remained a challenging quarter for OMCs. The impact of the US-Iran conflict led to higher crude prices and pressure on marketing profitability. To offset the widening losses, OMCs implemented retail fuel price hikes in May’26 of Rs7.4/7.5/ltr for MS/HSD. The subsequent softening in crude prices, following the announcement of a ceasefire agreement between the US-Iran (reportedly signed electronically on June 17th), provided some relief towards the latter part of the quarter. However, the overall Q1FY27 performance remains weak as the benefit from lower crude prices was insufficient to offset the full-quarter impact of elevated input costs and compressed marketing margins. For Q1FY27, MS and HSD GMM are estimated at a loss of Rs7/10/ltr, respectively, after factoring in the impact of excise duty cuts and capped product cracks. The sharp deterioration in marketing margins is expected to materially impact profitability. At crude price of US78.0/bbl, GMM for MS and HSD are expected at Rs10.6/ltr and Rs8.2/ltr respectively (including excise cuts and capped cracks).

Excise duty rollback remains a risk for OMC earnings

While the recent improvement in crude prices and retail fuel price hikes have resulted in a recovery in GMMs, a key risk remains underappreciated - the potential rollback of the excise duty cut. The excise duty reduction was introduced as a crisis management measure rather than a permanent structural change. With crude prices moderating, retail fuel price hikes implemented, and marketing margins turning positive, the government may gradually withdraw this benefit. The government continues to bear a significant revenue impact of ~INR1700bn per year from the excise cut. Overall, while near-term sentiment has improved, Q1FY27 losses and continued uncertainty around the excise duty rollback suggest that OMC profitability is likely to remain under pressure through FY27.

LPG under-recovery remains the biggest pain point

LPG continues to remain the most challenging component of the OMC loss pool. While commercial LPG prices have witnessed periodic price increases, residential LPG prices continue to remain regulated, resulting in significant under-recoveries. Based on Q4FY26 concall commentary, OMCs witnessed a sharp increase in LPG losses. Industry-wide LPG under-recoveries increased from ~Rs84/cyl in Q4FY26 to ~Rs170/cyl in April’26 and further surged to ~Rs600-670/cyl in May 2026 due to supply disruptions caused by the US-Iran conflict. Saudi CP prices in Q1FY27 are estimated to average USD796.0/mt, representing a QoQ increase of ~46.7%.

Crude oil outlook: Near-term decline, but volatility remains

After a hiatus of 3.5 months, a concrete US-Iran deal has finally been announced. As a result, Brent declined below USD80/bbl after remaining above USD95/bbl for much of the quarter. Iranian oil exports are expected to resume immediately; however, the structural damage from the disruption is not completely resolved yet. We expect oil prices to decline initially as a gush of supply is expected to enter the market once safe passage through the Strait of Hormuz resumes, putting further downward pressure on crude prices. However, the decline in prices may be limited. Countries that utilised their Strategic Petroleum Reserves (SPRs) and inventories during the conflict are likely to begin replenishing stocks, which could provide support to crude prices. The rebuilding of inventories is expected to create additional demand in the market, potentially offsetting some of the near-term supply-driven pressure and supporting prices

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Utilities & Power Equipment : 10 POWER points; A weekly roundup on power & utilities #34/FY2...