Information Technology Sector Update : Weak result cloud FY27 start for Indian IT peers by PL Capital

Accenture’s (ACN: NYSE) Q3FY26 revenue growth came in below consensus estimates, while bookings were weaker than anticipated due to delayed closure of large deals amid disruptions caused by the Middle East conflict. Management highlighted a ~US$100mn revenue impact in Q3FY26 from the Middle East conflict, with continued disruption expected in Q4FY26, leading to a 100bps reduction in the upper end of its FY26 revenue growth guidance. The impact was also visible in bookings, particularly within Managed Services, where several large deals were deferred into FY27, highlighting elongated decision-making cycles. The company also announced a dedicated strategy to target mid-market enterprises (US$300mn– US$3bn revenue), which it estimates represents a US$ 240 bn addressable market. For Indian IT services companies, the read-through is incrementally negative as the results suggest a softer start to FY27, with limited direct revenue exposure to the Middle East but potential indirect impact through delayed deal closures, slower project ramp-ups and prolonged client decision cycles. Further, Accenture's increased focus on the midmarket segment could intensify competitive pressures for mid-cap Indian IT companies, while weaker Managed Services bookings and the guidance cut suggest that discretionary spending weakness & delayed decision making, pointing to a weaker H1 for Indian IT peers.

* Demand & Outlook:

Accenture reported Q3 revenue growth of 3% YoY in CC, below consensus estimates. The growth was driven by CMT segment and APAC region. The demand environment was subdued, with management indicating a USD 100mn impact on revenue from geopolitical uncertainty in the Middle East conflict & an indirect global impact in Products and resources verticals. ACN lowered the top end of its FY26 revenue guidance to 2–4% YoY CC (vs. 2–5% earlier) excl. US Federal business as its expects demand uncertainty from ME conflict to continue in Q4.

* Weak Managed Services bookings:

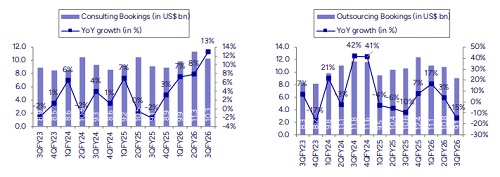

Managed services growth moderated at 5% YoY CC, with deal wins softening to USD 9.1bn, down 15% YoY (vs. USD 10.8bn, up 3.5% YoY in Q2). Overall bookings saw marginal degrowth at USD 19.3bn, down 3% YoY CC (down 2% reported), while consulting bookings were strong at USD 10.3bn, up 13% YoY. ACN expects managed services to grow at mid-single digits for FY26.

* CMT momentum continues, FS moderates:

ACN growth was broad based across segments & geographies (excluding healthcare which is impacted by Federal services business). Growth was driven by CMT segment which grew by 9% YoY CC after reporting 10% growth in Q2. FS growth moderated to 3% while Healthcare was flat.

* AI investments for newer opportunities:

ACN continues to see strong momentum in GenAI, with clients investing in the foundations needed to scale AI, including cloud, data, security and operating model transformation. Management highlighted that data remains a critical enabler, with at least one out of every two advanced AI projects continuing to lead to a data project. Management further highlighted plans to scale investments in the OT cybersecurity platform & the Midmarket Segment, where it identifies a TAM of USD 240bn.

* Increase in net employee:

Net headcount rose by 12.3k, marking a third consecutive quarter of additions.

Please refer disclaimer at Report

SEBI Registration number is INH000000933