Renewable Energy Sector Update : India's solar boom powers RE leadership by PL Capital

Quick Pointers

* India’s solar capacity surged to ~150GW(AC) as of Mar’26, with ~45GW(AC) added in FY26.

* ALMM-II has created a growth runway for integrated players

India’s solar sector is entering a structural multi-year growth phase, supported by record capacity additions, strong policy support, and rapid localization in manufacturing. India added a record 44.6GW(AC) of solar capacity in FY26, taking cumulative installed solar capacity to ~150GW(AC) and making the country the world’s third-largest solar market. Growth was broad-based across utility, C&I, rooftop and agricultural segments, while domestic module manufacturing capacity scaled to ~172GW(DC), supported by PLI, ALMM and BCD measures. The sharp reduction in module imports and increasing selfsufficiency across the value chain is strengthening long-term industry competitiveness and execution visibility.

Distributed solar emerged as a key growth driver in FY26, contributing ~16.3GW(AC) (~36% of total additions), aided by strong traction under the PM Surya Ghar: Muft Bijli Yojana (PMSG) and Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan (PMKUSUM). Residential rooftop adoption continues to accelerate, with PMSG covering ~3.4mn households against the target of 10mn, while agricultural solarization represents a massive long-term opportunity of ~191GW(DC). In parallel, C&I solar installations increased to ~15GW(AC) and are expected to sustain strong momentum, supported by favorable open-access policies and rising demand for green power. With ~90GW(AC) of solar capacity under construction and a large tender pipeline across utility, rooftop and PM-KUSUM segments, demand visibility remains robust over the medium term.

On the manufacturing side, ALMM-I continues to support domestic module demand, while cell manufacturing capacity is likely to increase from 27GW in FY26 to 37.5GW in FY27 and 50GW in FY28, as per industry estimates. Despite announced expansions, domestic cell capacity remains well below potential demand, creating a favorable environment for integrated players with cell-module capabilities, through better pricing power, higher utilization and stronger order inflows. We remain constructive on the domestic solar value chain given rising localization, strong policy support, expanding domestic demand and emerging export opportunities, with preference for companies possessing scale, backward integration, technology readiness and proven execution capabilities.

For PREMIERE, we estimate revenue/EBITDA/PAT CAGR of 46.4%/35.8%/23.0% over FY26-28E, with ‘HOLD’ rating and TP of INR1,138 based on 12x Mar’28E EV/EBITDA.

For WAAREEEN, we estimate revenue/EBITDA/PAT CAGR of 21.9%/21.7%/17.3% over FY26-28E, with ‘BUY’ rating and TP of INR3,713 valuing at 12x Mar’28E EV/ EBITDA.

For VIKRAMSO, we estimate revenue/EBITDA/PAT CAGR of 69.9% / 66.9% / 19.0% with over FY26-28E. with ‘Accumulate’ rating and TP of INR 226 based on 5.3x Mar’28E EV/EBITDA

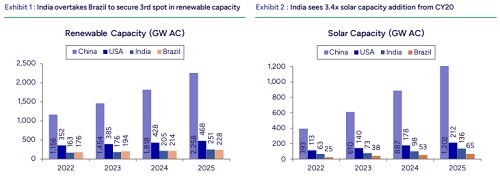

India rises to 3rd globally in RE installed capacity

India has overtaken Brazil in the global RE rankings, according to data released by the International Renewable Energy Agency (IRENA) as of Dec’25. Further, the country now ranks 3rd globally in solar installed capacity at 136GW(AC), behind China (1,202GW(AC)) and the US (212GW(AC)). India recorded stronger capacity addition growth of 37.6% in CY25, outpacing China’s 35.5%.

India’s solar capacity has reached ~150GW(AC) with module manufacturing capacity scaling up to ~172GW(DC) as of Mar’26, significantly reducing import dependence and strengthening domestic supply-chain selfsufficiency. This backward integration, supported by policy measures (PLI, ALMM and BCD), has led to a sharp decline in module imports, while improving module availability for domestic developers and C&I players.

The strong capacity addition of ~45GW(AC) in FY26, highest ever alongside rising rooftop and distributed solar penetration (~36% of additions), indicates robust underlying demand and deeper market penetration. India is transitioning from import reliance to potential export competitiveness, supporting long-term sectoral growth visibility and margin stability.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

.jpg)