Consumer Sector Update : Strong primary demand as stocking continues by PL Capital

Demand momentum remains healthy, which will enable paint companies to report midteens value growth in 1QFY27. Primary sales continue to outpace secondary demand on dealer stocking ahead of price hikes. Trade channels don’t rule out some consumer deferment in repainting amid inflationary pressures, although no material signs are visible so far. Competitive intensity remains elevated, driven by sustained market share push by Birla Opus and JSW Akzo. We estimate Q1FY27 Sales/EBITDA/PAT for APNT & KNPL to grow by 16.5%/17.9%/18.2% & 13.5%/8.6%/1.3%

We remain constructive on KNPL, supported by a healthy industrial coatings outlook and attractive valuations. While our channel checks suggest APNT's market share trends are stabilizing, but rich valuations limit near-term upside post recent rally in the stock price. While persistent inflation remains key monitorable for demand, strong summer and weak monsoons will likely increase the window for painting in FY27. We estimate FY26-28 sales/EPS CAGR of 8.6%/9.9% for KNPL and 8.8%/10.5% for APNT. We retain Accumulate on KNPL (TP of Rs248) and Hold on APNT (TP of Rs2,654)

Strong summer, dealer stocking keeps demand trends strong in 1Q27

Our pan-India channel checks indicate that healthy demand momentum persisted in Q1FY27, supported by continued dealer stocking in April and May ahead of further anticipated price hikes. As a result, primary sales continued to outpace secondary offtake, with dealer inventory levels estimated to be higher by ~5-6% YoY and overall decorative paints industry growth remaining at healthy double-digit levels in 1Q.

West and south India report strong demand trends

On the regional front, West and South India continued to witness relatively stronger demand, driven primarily by renovation and repainting activity. In contrast, East, North and Central markets remained comparatively subdued amid inflationary concerns and cautious consumer spending behavior. Dealers also highlighted that repainting demand continues to materially outperform new construction-led demand.

Competitive Intensity remains elevated

On the competitive front, channel checks indicate that competitive intensity from Birla Opus remains elevated, with the company having garnered an estimated ~7% market share. Birla Opus continues to gain consumer traction, aided by product pricing that remains 7-8% below incumbent peers. Dealer support initiatives continue to be healthy, driven by the deployment of sales promoters, partial reimbursement of dealer staff costs and investments in store interiors. However, the pace of incremental dealer additions has moderated as dealer margin differentials versus Asian Paints have narrowed. We expect competitive intensity to remain high as JSW Akzo and JK Cement are also upping the ante in the decorative paints business.

Demand healthy as stocking continues, APNT gains some ground

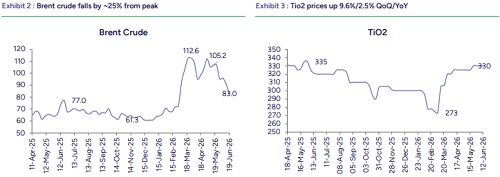

* Our recent channel interactions indicate that the industry has witnessed cumulative price hikes of ~10-17% so far, with companies taking price increases almost every month and, in several cases, revising prices nearly twice a month to offset elevated raw material costs.

* Demand trends remain healthy, supported by dealer stocking ahead of anticipated price hikes, although underlying consumer offtake has moderated as repainting decisions are being deferred. We expect paint companies to deliver healthy double-digit sales growth in Q1FY27, aided by continued channel loading and favorable pricing actions. However, the impact of the sharp correction in crude prices on channel inventories remains a key monitorable.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

.jpg)