Oil and Gas Sector Update : Tighter Balances, Higher Risks Choice Institutional Equities

Developments over the past week:

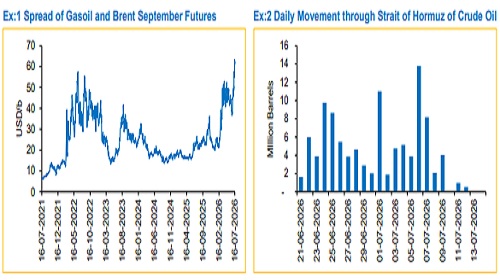

* Hormuz Tensions Escalate: Geopolitical tensions intensified this week as the US resumed military strikes on Iran and reinstated its blockade of Iranian shipping, following the collapse of the interim peace agreement. Iran reiterated that the Strait of Hormuz would remain closed until its demands are met, while the International Maritime Organization warned that the waterway remains unsafe for commercial navigation. The renewed uncertainty pushed Brent crude above USD85/b, reflecting a higher geopolitical risk premium

* IEA Warns of Rising Global Energy Risks: The International Energy Agency (IEA) cautioned that prolonged disruptions in the Strait of Hormuz could pose a significant risk to the global economy if normal shipping is not restored within weeks. The agency highlighted that while developed Asian economies would face supply challenges, import-dependent nations such as India, Pakistan and Bangladesh remain particularly vulnerable to sustained disruptions in oil and gas flows

* Russian Refining Disruptions Tighten Diesel Markets: Ukraine's continued attacks on Russian refineries have reduced Russia's crude processing to its lowest level since 2005, prompting Moscow to ban exports of gasoline, jet fuel and diesel. The resulting decline in Russian product exports has tightened global diesel balances, driving refining margins and gasoil cracks sharply higher as importers increasingly compete for replacement supplies from the US, India and the Middle East.

In our opinion:

* The renewed disruption in the Strait of Hormuz has emerged at a time when global inventories have already been significantly depleted following several weeks of supply deficits. With inventory buffers considerably lower than during the first disruption, any prolonged restrictions on crude and product flows could trigger a sharper price response than previously witnessed as consumers increasingly compete for a shrinking pool of available barrels. We estimate there is an apparent demand of 900 million barrels for calendar year 2026 which bakes in disruptions in Strait of Hormuz and interim ceasefire

* Diesel balances continue to tighten as Russian refining disruptions coincide with Middle East supply risks. We expect elevated diesel cracks to persist, providing a meaningful earnings tailwind for MRPL and CPCL given their diesel-heavy product slate

* Provided the flows through Strait of Hormuz were materially higher during second half of June as compared to our previous assumption wherein we estimated that flows would take at least 3 month to normalize, we now believe that replenishment of flows could be much faster. Therefore, we estimate Brent price to average at USD82/b for FY27. However, we note upside risk to our estimate if the current blockade extends beyond 3-4 weeks

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

More News

Automobiles Sector Update : Auto Sales Soar as Rain Pours by PL Capital