Oil & Gas Sector Update : Gas supply normalizing; volume growth in focus for upstream by Motilal Oswal Financial Services Ltd

We met with the management teams of GAIL, Petronet LNG (PLNG), and Oil India in Delhi last week. Key takeaways from our discussions are as follows:

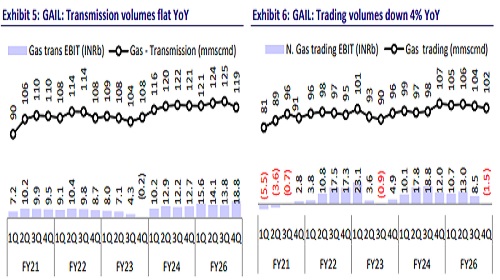

* Post Strait of Hormuz (SOH) re-opening, Middle East gas flows continue to normalize upward: Following the re-opening of the SoH, ME gas flows have continued to normalize upward. Our channel checks indicate GAIL transmission volumes of 115–120 mmscmd in 1QFY27 (peaking at 130 mmscmd on some days in June), led by robust power sector demand. PLNG is witnessing a similar trend, with utilization expected to normalize by end-July as Qatari supply ramps up.

* Focus on listing plans and CGD expansion in FY27: GAIL continues to evaluate the listings of MNGL and GAIL Gas, with progress on the MNGL listing expected during FY27. Ahead of the GAIL Gas listing, the company intends to consolidate its CGD portfolio by transferring some GAs and certain other investments into GAIL Gas (GAIL currently holds a 22.5% stake in MNGL). Separately, the CGD rollout is set to accelerate, with annual CNG station additions expected to rise from ~90 to ~140.

* Spot LNG demand strong despite high prices; normalization ahead: Spot LNG activity remained strong over the past two months despite elevated prices (USD18–19/mmbtu). PLNG management expects this to normalize from Sep’26 as long-term LNG volumes ramp up.

* We have a BUY rating on PLNG and GAIL and a Neutral rating on Oil India.

Valuation and view

* PLNG (Buy): At 12x FY27E P/E and a ~3.6% dividend yield, we believe valuations are inexpensive. Our DCF-based TP of INR360 is based on a WACC of 11.5% and TG of 2%. The valuation assumes a 5% tariff cut at the Dahej terminal in FY28, followed by a 4% rise for both the terminals. While we have incorporated the full capex for the petchem plant, we value it conservatively at 0.5x FY29E P/B and discount this back to FY27.

* OINL (Neutral): In the past few quarters, OINL has struggled to raise production/sales. Further, while we like the increased exploration intensity, we believe this will likely be accompanied by higher dry well write-offs, which will weigh on earnings. The company aims to drill 100 wells by FY27. The NRL refinery segment is expected to achieve 50% capacity utilization by the end of FY27, which shall gradually ramp up to 100% by the end of 2QFY28. Our SoTPbased TP is INR475.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...