Oil and Gas Sector Update : Crude Compass: Evaporation of Precautionary Demand Choice Institutional Equities

Developments over the past week:

* The US President confirmed that an agreement between the US and Iran had been reached and authorized the withdrawal of US naval blockade measures on Iranian ports in the Strait of Hormuz

* The official signing of the agreement is scheduled for June 19, 2026 , in Switzerland.

* The US President commented in France on June 17, 2026 that US strikes would resume if Iran does not honor the agreement

In our opinion:

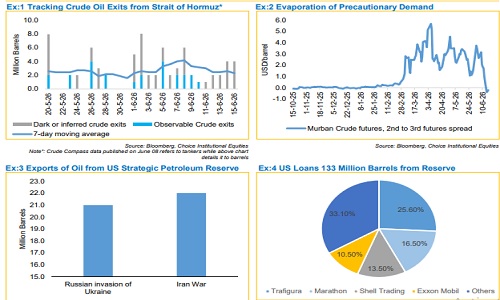

* As we closely track the crude exits through the Strait of Hormuz in Exhibit 1, these are still in the range of 2mbd on a 7-day moving average. However, the dark crude exits have increased to 4mbd as of 14th and 15th June respectively. The current market prices are reflecting not just crude exits but evaporation of precautionary demand, explained in edition of Crude Compass on March 12, 2026. We had set the reflection of precautionary demand from USD90/b and upwards and Brent settling at USD87.33/b as of June 12, 2026, ahead of Sunday meeting, justifies our view based on Energy economics.

* This is supported by Exhibit 2, wherein Murban Crude futures chart has moved into contango as of 15th June 2026, as the spread turned negative. The collapse in Murban backwardation indicates that the precautionary demand premium has largely evaporated, with market participants becoming increasingly comfortable with the availability of near-term crude supplies.

* As there has been a draw of about 8mbd from inventories due to 7-11mbd of physical deficit over the previous weeks, the replenishment of these inventories will provide support to Brent prices during FY27.

We have built the following scenarios for Brent price:

* Our base case for Brent remains at USD 89.0/b for FY27, supported by curtailed production levels, critically low inventories, and the likelihood that supply normalization will lag the reopening of shipping routes

* In a faster-normalization scenario, where traffic through the Strait of Hormuz recovers materially ahead of our assumed threemonth timeline following sustained reopening, we estimate Brent to average approximately USD 82.0/b for FY27 . For context, Brent has averaged at USD 99.7/b on a FY27 year-to-date basis.

* As published on April 23, 2026 along with commentary published in Convex Choice, we assigned a 5% probability to our least-likely scenario, which envisaged a prolonged geopolitical standoff delaying the sustained reopening of the Strait of Hormuz until end-July 2026. Under such conditions, continued supply constraints and accelerated inventory drawdowns could have lifted Brent to an average of USD 98.0/bbl in FY27.

We estimate Brent to average at USD89.0/b in FY27, provided flows through Strait of Hormuz recover over a period of 3 months. In best possible scenario, we expect to average at USD82.0/b for FY27.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...