Buy Reliance Industries Ltd for the Target Rs.1,655 by Motilal Oswal Financial Services Ltd

Jio IPO imminent; AI, FMCG, and New Energy to be the key growth engines

In the FY26 AGM speech, Reliance Industries’ (RIL) chairman announced: i) an ambition to more than double RIL’s consolidated EBITDA over the next five years, ii) DRHP filing and the imminent listing of Jio Platforms (JPL), iii) a deeper push into manufacturing across fresh produce, apparel, and consumer electronics, while reiterating the target of achieving INR1t in gross revenue for Reliance Consumer Products (RCPL, the FMCG arm) by FY30, and iv) five major value creation pathways for RIL (reinventing the O2C business to create secular growth revenue streams, accelerating commissioning and early revenue generation in New Energy, scaling Reliance Intelligence into the most prolific growth platform, turning RCPL into India’s largest FMCG company, and enabling USD125-150b exports by 2032). Reiterate BUY with a TP of INR1,655.

JPL: Value unlocking underway through an imminent IPO

* JPL has filed its DRHP, with the IPO comprising a fresh issue of up to 270m equity shares (~2.9% of post-issue equity capital). The proceeds from the IPO will primarily (INR275b) be utilized to prepay or repay RJio’s borrowings.

* Management is targeting to: i) migrate all subscribers to 5G by 2030 (currently 268m subs on 5G), while advancing India’s leadership position in 6G, ii) provide high-speed home broadband (HBB) to every part of India through JioAirFiber, iii) digitize Indian enterprises and small businesses, iv) make AI accessible to everyone, and v) take India’s deep tech capabilities to the global market.

* HBB connections have now accelerated to 60k installations per day, with TAM expanding significantly through non-line-of-sight capabilities.

* Jio also announced plans to build sovereign satellite broadband capabilities through a dual strategy of partnering with global constellation operators while evaluating the development of its own Low Earth Orbit (LEO) satellite constellation and ground station infrastructure in India.

* Please refer to our latest note for a deep dive into JPL and our analysis of JPL and RJio’s FY26 annual report. We ascribe an enterprise value of ~INR12t (~USD128b) to JPL, based on ~11.5x Mar’29 EV/EBITDA, which implies an overall equity value of INR10.7t (~USD114b) for JPL (INR525/share attributable to RIL).

Reliance Retail (RRVL): Building a vertically integrated consumer platform

* Since its launch in Nov’06, RRVL has aggressively scaled to 20,000+ stores, transforming into an omnichannel retail ecosystem through JioMart and AJio.

* Reliance outlined a deeper push into manufacturing, extending from beverages and daily essentials to fresh produce, apparel, and consumer electronics, with the aim of increasing control over sourcing, production, and distribution while capturing a larger share of the value chain.

* Alongside domestic expansion, the company is building export capabilities for its consumer businesses, creating a potential new growth avenue beyond the Indian retail market.

* Quick commerce is emerging as an important growth engine, with the company leveraging its existing store network and supply chain infrastructure rather than building a standalone fulfillment model.

RCPL: Scaling FMCG through manufacturing and distribution

* RCPL reiterated its ambition of reaching INR1t revenue by FY30 (vs. INR220b in FY26), supported by continued investments in brand building, distribution expansion, exports ramp-up, and category diversification.

* The company plans to invest INR300b over the next three years (on top of INR100b investments to date) in integrated food parks, reflecting a strong focus on backward integration, manufacturing scale, and long-term cost leadership.

* Distribution has already reached over 3m outlets within three years, while recent acquisitions continue to strengthen the portfolio across foods, beverages, and personal care.

Media & Entertainment: Building a scaled engagement and commerce platform

* JioStar, JioStudios, and Network18 together posted revenue of INR349b, EBITDA of INR58.5b, and net profit of INR34.3b in FY26, with a 34.7% viewership share and 451m MAUs on JioHotstar.

* The company continues to integrate content, commerce, and advertising across the JioStar ecosystem, leveraging its leadership position across television, digital media, and sports streaming.

* The company highlighted increasing use of AI across content creation, discovery, and user engagement, while introducing commerce capabilities that allow consumers to transact directly within content platforms.

* The broader strategy is to deepen user engagement across the digital ecosystem, creating additional monetization opportunities beyond traditional subscription and advertising revenues.

Reliance Intelligence (RI): Building India's sovereign AI infrastructure and democratizing AI

* Reliance Intelligence entered the execution phase with the objective of building a profitable AI infrastructure, platform, and services business catering to consumers, enterprises, and governments at scale. RIL reiterated its ambition of making AI accessible to "everyone, everywhere."

* RIL is building India's sovereign AI backbone in Jamnagar, powered entirely by renewable energy from the Kutch platform. The first 120MW of AI infrastructure will be commissioned by end-2026 and will house advanced NVIDIA GB300 GPUs equivalent to more than 75,000 H100 GPUs on an inference basis, scalable to over 200,000 H100-equivalent GPUs.

* RIL deepened partnerships with Google and Meta. Google AI Pro powered by Gemini is already being offered free to Jio users, while the Meta collaboration enables sovereign deployment of Llama models with full transparency and portability for Indian enterprises.

* RI is developing multilingual AI solutions across 22 Indian languages through platforms such as JioBharatIQ, AI Vyapar, JioHealthIQ, JioLearnIQ, and JioKrishiIQ, targeting consumers, SMEs, healthcare, education, and agriculture.

* Management reiterated that, similar to how RJio disrupted telecom services, RI aims to disrupt AI economics by making AI dramatically more affordable for Indian users by the end of the decade. AI capabilities are already being embedded across Jio, Retail, JioStar, and O2C operations.

E&P volumes to plateau; downstream O2C integration in focus

* RIL’s E&P business is expected to deliver stable production, with KG-D6 producing ~26mmscmd of gas and ~18kb/d of oil.

* The O2C segment faced margin pressure in 4QFY26 due to elevated crude spot premiums, higher freight rates, and increased insurance costs.

* However, RIL continues to invest aggressively in downstream integration and specialty materials, including a 3mmt PTA plant at Dahej, a carbon fiber facility at Hazira, and a 1.2mmt PVC plant at Nagothane.

* Jio-bp is expected to maintain strong momentum (FY26: 29% YoY auto-fuel volume growth), supported by a network of over 2,200 outlets (another 400 under development).

New Energy: Enters commissioning and early revenue generation phase

* RIL indicated that its New Energy business will begin contributing meaningfully to financial performance from FY27.

* The company commissioned solar PV cell and module manufacturing lines during FY26, achieved India’s first ALMM listing for HJT technology, and expects commercial solar revenues to commence in FY27.

* Key projects under construction include a 20GW integrated solar manufacturing ecosystem, a 40GWh battery giga-factory (scalable to 120GWh), a massive renewable energy hub in Kutch, and green hydrogen/green ammonia initiatives.

Valuation and view

* We expect RJio to remain the biggest growth driver (digital to contribute ~80% of RIL’s incremental EBITDA), with 18% EBITDA CAGR over FY26-28E, driven by the wireless tariff hike (~15% in 2Q), market share gains in wireless, and the continued ramp-up of Homes and Enterprise offerings.

* We expect RRVL to deliver ~12% revenue CAGR over FY26-28E, driven by a mix of store rollouts, improved productivity, and scale-up of hyper-local offerings. However, the faster ramp-up of lower-margin businesses could weigh on blended EBITDA margin, driving ~10% EBITDA CAGR over FY26-28E.

* After a subdued FY25, RIL’s O2C EBITDA improved in FY26 but was hit by higher crude premiums and high freight and insurance costs due to the West Asia conflict. Going ahead, we expect only a modest recovery over FY26-28. Our FY28E consolidated EBITDA for O2C and E&P is broadly similar to FY24.

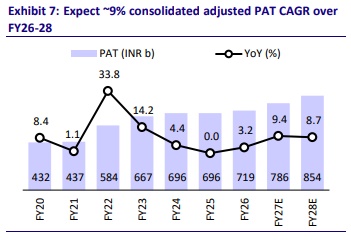

* Overall, we build in a CAGR of ~9-10% in RIL’s consolidated EBITDA and PAT over FY26-28E. We model an annual consolidated capex of INR1.25t for RIL over FY26-28E as we believe the peak of capex in digital services is likely behind, which should lead to healthy FCF generation (~INR1t over FY26-28E) and a corresponding decline in consol. net debt.

* For RRVL, we ascribe a blended EV/EBITDA multiple of 28x (30x for core retail and ~6x for connectivity) to arrive at an EV of ~INR8.5t (or ~USD91b) and an attributable value of INR500/share for RIL’s stake in RRVL. Sustained mid-teen revenue growth in RRVL remains the key for RIL’s re-rating.

* We value RJio at ~11.5x Mar’28E EV/EBITDA to arrive at our enterprise valuation of INR11.3t (USD120b) and assign ~USD8b (INR740b) valuation to other nonmobility offerings under JPL to arrive at INR12t (or ~USD128b) enterprise valuation for RIL’s digital services. Factoring in net debt and ~33.5% minority stake, the attributable equity value for RIL comes to INR525/share.

* Using the SoTP method, we value the O2C/E&P segments at 7.5x/5.0x Mar’28E EV/EBITDA to arrive at an enterprise value of INR5.8t (or ~INR427/sh) for the standalone business. We ascribe an equity valuation of INR525/sh and INR500/sh to RIL’s stake in JPL and RRVL, respectively. We assign INR174/sh (~INR2.4t equity value) to the New Energy business, INR26/sh (~INR350b) to RIL’s stake in JioStar, and INR39/sh (~INR530b, based on 2x FY28 gross sales) to RCPL (RIL’s FMCG arm). We reiterate our BUY rating with an unchanged TP of INR1,655.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)