Neutral Zydus LifeSciences Ltd for the Target Rs 1,080 by Motilal Oswal Financial Services Ltd

DF/EM offset moderating US business Work in progress to scale up new growth levers

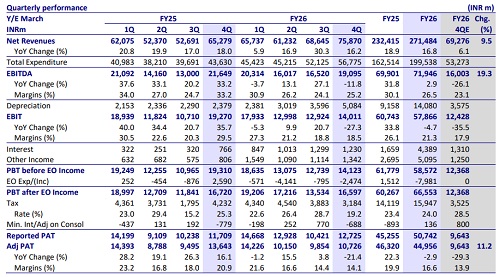

* Zydus LifeSciences (ZYDUSLIF) delivered a better-than-expected financial performance in 4QFY26, with 9.5%/19%/11% beat on revenue/EBITDA/PAT. Revenue traction in the US and emerging markets was higher than expected for the quarter. Domestic formulation (DF) and consumer wellness revenue came largely in line with expectations.

* After three consecutive years of strong YoY growth in the US segment over FY23-25, ZYDUSLIF reported stable sales in FY26 (down 11% in CC terms in 4Q). In addition to a limited-competition generics pipeline, ZYDUSLIF is building a specialty franchise through developing 505b2 products, as well as acquisitions. ? It has progressed well in the DF segment, outperforming the industry and improving the share of chronic therapies in the DF portfolio. Further, it is scaling up biosimilar offerings in the DF segment through new launches (Nivolumab, Aflibercept, Semaglutide).

* With the therapy-focused approach and market-specific targets, ZYDUSLIF has delivered strong YoY growth in the emerging market segment in 4Q and FY26.

* We raise our earnings estimates by 5%/4% for FY27/FY28, factoring in

a) increased traction in limited-competition products in the US

b) industrybeating performance in DF and other emerging markets

c) higher R&D spending

d) enhanced efforts toward marketing/promotion. We value ZYDUSLIF at 21x 12-month forward earnings to arrive at a TP of INR1,080.

* Considering a higher base of FY26, we expect 7% earnings CAGR over FY26- 28. The current valuation provides limited upside and hence, we maintain Neutral rating on the stock.

Lower operating leverage/product mix benefits impacted profitability

* ZYDUSLIF sales grew 16.2% YoY to INR75.9b (our est. INR69.2b).

* Gross margin was stable at 74%.

* EBITDA margin contracted 800bp YoY to 25.2% (our est. 23.1%) due to higher opex (other expenses up 465bp YoY each as % of sales), R&D spend (up 185bp YoY as % of sales), and employee expenses (up 145bp YoY as % of sales).

* EBITDA decreased 11.8% YoY to INR19.1b (our est. INR16.0b).

* ZYDUSLIF had forex gains of INR6.5b. An exceptional item of INR3.9b pertains to a one-time settlement cost with Astellas Pharma.

* Adjusting for the same, PAT declined 21.4% YoY to INR10.7b (our est.: INR9.6b).

* For FY26, revenue/EBITDA grew 17%/3% YoY to INR271b/INR72b, while PAT fell 3% YoY to INR45b.

Valuation and view

* We raise our earnings estimates by 5%/4% for FY27/FY28, factoring in

a) increased traction in limited-competition products in the US

b) industry-beating performance in DF and other emerging markets

c) higher R&D spending

d) enhanced efforts toward marketing/promotion. We value ZYDUSLIF at 21x 12- month forward earnings to arrive at a TP of INR1,080.

* Considering a higher base of FY26, we expect 7% earnings CAGR over FY26-28. The current valuation provides limited upside and hence, we maintain Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412