Neutral R R Kabel Ltd for the Target Rs. 1620 by Motilal Oswal Financial Services Ltd

Disciplined execution drives profitability; healthy volume growth outlook

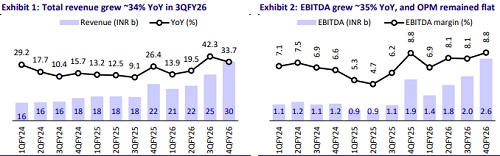

* RR Kabel’s (RRKABEL) 4QFY26 performance was above our estimate, led by higher-than-estimated revenue and margin in the cable and wire (C&W) segment. Consol. revenue rose ~34% YoY to INR29.6b (~10% beat). EBITDA grew ~35% YoY to INR2.6b (+24% vs. our est.). OPM was flat YoY to 8.8% (+1.0pp vs. our est.). PAT increased 30% YoY to INR1.7b (+24% vs. our est.).

* Management indicated that the C&W segment reported volume growth of ~10% YoY in 4Q and ~16% in FY26. It guided ~16-18% volume growth in FY27, fueled by capacity expansion and export opportunities. Input material costs remained volatile, while timely pricing action, disciplined procurement, and efficient execution aided profitability. Margin expansion of 1.3pp was achieved under project RISE, and it will achieve a 10.5% margin in C&W by FY28. Export demand remained strong except for temporary headwinds amid geopolitical issues in the Middle East.

* We increase our EPS estimates by ~7%/6% for FY27-28 on account of higher volume growth guidance. The stock is trading at 32x/26x FY27E/FY28E EPS. We value RRKABEL at 27x FY28E EPS to arrive at our revised TP of INR1,620 (earlier INR1,500). Reiterate Neutral.

C&W revenue rises ~36% YoY, and margin stands at 9.6% (est. 8.2%)

* Consol. revenue/EBITDA/Adj. PAT stood at INR29.6b/INR2.6b/INR1.7b (up 34%/35%/30% YoY and +10/+24%/+24% vs estimates). Gross margin dipped 1pp YoY to ~19%. Employee costs increased ~35% YoY (at 3.6% of revenue, similar to 4QFY25). Other expenses increased 14% YoY (at 6.2% of revenue vs. 7.2% in 4QFY25). Depreciation/interest increased ~38%/61% YoY, while other income rose ~8% YoY.

* Segmental highlights: 1) C&W: Revenue increased ~36% YoY to INR26.7b, and EBIT increased ~33% YoY to INR2.6b. EBIT margin dipped 30bp YoY to ~10%; and 2) FMEG: Revenue increased ~14% YoY at INR3.0b. The company reported a segmental loss of INR93m vs. INR91m/INR49m in 4QFY25/3QFY26.

* In FY26, Revenue/EBITDA/PAT stood at INR97.2b/INR7.8b/INR5.1b, which was +28%/+61%/+63% YoY. OPM expanded 1.7pp YoY to 8.1%. The C&W segment revenue grew ~31% YoY to INR87.6b, while EBIT grew ~56% to INR7.8b. C&W EBIT margin expanded 1.4pp YoY to 8.9%. OCF stood at INR3.0b vs INR4.9b in FY25, due to an increase in working capital. Capex stood at INR2.9b vs INR3.7b. FCF stood at INR42.6m vs. INR1.3b in FY25.

Key highlights from the management commentary

* The C&W segment continues to be the key growth driver, aided by healthy domestic demand (infra, housing, and industrial) and strong export traction.

* FMEG revenue remained steady despite a competitive market environment and selective demand conditions. Revenue growth was supported by stable demand across key categories and continued expansion in distribution.

* Capex was pegged at INR12b over FY26-28, with INR3.5b already spent. Capacity will be added in phases every six months, ensuring demand-linked expansion and better utilization.

Valuation and view

* RRKABEL’s 4QFY26 earnings were above estimates, led by higher growth in both the C&W and FMEG segments. It witnessed robust export performance during the quarter, despite global conflicts. Management remains confident of sustaining growth in the C&W segment and targeting ~16-18% volume growth in FY27E. It expects C&W margin to improve to 9.5%/10.5% in FY27/FY28 vs. 8.9% in FY26, given margin expansion initiatives under project RISE. It is targeting ~25% value growth in the FMEG segment, with breakeven expected in FY27.

* We estimate RRKABEL’s revenue/EBITDA/PAT CAGR at ~15%/18%/17% over FY26-28. We estimate OPM at 8.2%/8.5% in FY27/FY28 vs. 8.1% in FY26. The stock is trading at 32x/26x FY27E/28E EPS. We value RRKABEL at 27x FY28E EPS to arrive at our revised TP of INR1,620 (earlier INR1,500). Reiterate Neutral.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041