2025-08-29 04:17:51 pm | Source: Motilal Oswal Financial Services

Neutral Alembic Pharma Ltd for the Target Rs. 990 by Motilal Oswal Financial Services Ltd

Export strength offsets muted DF/API show

Re-assessing DF business for higher productivity and sustainable growth

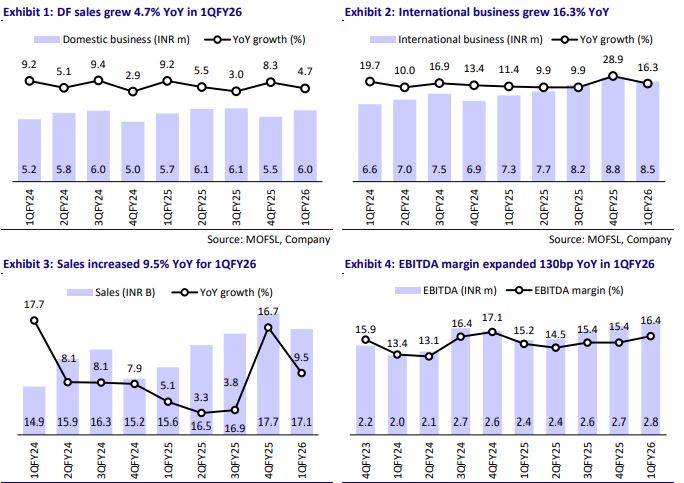

- Alembic Pharma (ALPM) delivered a largely in-line performance for 1QFY26. Superior execution in the export market led to YoY growth in revenue/EBITDA/PAT for the quarter. This benefit was offset, to some extent, by a muted show in the domestic formulation (DF) and API segments.

- ALPM sustained its growth momentum in the US market on the back of new launches. Notably, upcoming introductions such as g-Entresto have the potential to further strengthen growth in the US generics segment. That said, a broader scope of business would be necessary to enhance capacity utilization and, in turn, improve the profitability of the US generics segment.

- Growth of non-US exports has been broad-based across focus markets.

- The DF segment continues to struggle with growth. In 1QFY26, ALPM undertook measures to address certain challenges in this segment, which impacted the growth of the DF segment’s specialty category.

- We tweak our estimates for FY26/FY27 (+3%/+2%), factoring in: a) improved business prospects in the export market and b) near-term disruption in the DF segment. We value ALPM 22x 12M forward earnings to arrive at a TP of INR990.

- After a muted performance in FY25, ALPM is working to improve business prospects across its key markets. Growth in export markets is strengthening on the back of new launches and superior supply chain management. However, this is being offset to some extent by an inferior show in the DF and API segments. Considering these aspects, we expect a 24% earnings CAGR over FY25-27. The current valuation largely factors in the earnings upside. Hence, we reiterate a Neutral rating on the stock.

In-line 1Q; margin gain from product mix supports PAT growth

- ALPM sales grew 9.5% YoY to INR17b (in line).

- US generics sales grew 13% YoY to INR5.2b (USD61m; 31% of sales). Ex-US generics, export sales grew 21% YoY to INR3.3b (19% of sales). DF sales grew 5% YoY to INR6b (35% of sales).

- API sales were stable YoY at INR2.6b (15% of sales).

- Gross margin expanded 140bp YoY to 76% due to a better product mix.

- EBITDA margin expanded 130bp YoY to 16.4% (in line), led by a better gross margin. Higher R&D spend (+150bp YoY as a % of sales) was offset by lower other expenses (down 170bp as a % of sales).

- Consequently, EBITDA grew 19% YoY to INR2.8b (our est: INR2.7b).

- Adj. PAT grew 14.6% YoY to INR1.5b (in line).

Key highlights from the management commentary

- ALPM has guided for US sales to grow 10-15% YoY in FY26.

- Non-US sales are also guided to grow at 10-15% YoY in FY26.

- ALPM is addressing certain challenges in the DF business and has gained better control over channel inventory for its products. This, however, impacted specialty segment growth for the quarter.

- Data leakage by certain Chinese traders regarding exports from India has impacted ALPM’s API business.

- APLM expects to launch 4-5 products in the US in 2QFY26.

- Gross/net debt stood at INR11.8b/INR9.7b at the end of 1QFY26.

Exports drive near-term momentum; DF/API keeps outlook balanced US: Specialty focus and launch momentum to drive better sales growth

- The launch momentum continued in the US, driving 11% YoY growth in 1QFY26, reaching USD61m.

- Post 16 launches in FY25, ALPM launched four ANDAs in 1QFY26 with a target of 20 product filings in FY26.

- Interestingly, the filings are spread in terms of dosages (24 OSDs, 11 injectables, 6 Ophthalmics, and 5 dermatology by the end of Mar’25).

- ALPM’s R&D team is working on high-growth therapy such as oncology and dermatology, with 75 molecules in the pipeline and 35-40% in the non-oral solid dosage formulation. This implies complexity to manufacturing and, thus, fewer entry barriers, thereby driving better profitability.

- ALPM filed 2 ANDAs and received approvals for 6 ANDAs in 1QFY26.

- Notably, the capex required to cater to the manufacturing needs will be largely completed and going forward, only maintenance capex will be required over the medium term.

- From the approved portfolio, ALPM has a total of 223 approved ANDAs, comprising 153 oral solids, 30 dermatological products, 20 ophthalmic formulations, 18 injectables, and 2 inhalation products.

- Considering the new launches of complex products and a scale-up in existing products, we expect a 14% sales CAGR over FY25-27, reaching USD306m.

India: Acute outperforms, while specialty underperforms in 1QFY26

- The DF business has been witnessing moderate 6.7% growth on annual basis for the past three years. Specifically, for 1QFY26, the DF business came in at INR6b, up 5% YoY.

- 1QFY26 is the second consecutive quarter to reflect better growth in acute therapy (+6% YoY). After healthy performance for almost 19 quarters, the specialty segment was stable YoY in 1QFY26. Animal health continued its growth momentum, posting a 16% YoY growth in the quarter.

- ALPM’s specialty focus continues on gynaecology, anti-diabetes, ophthalmology, and dermatology, enabling it to outpace the industry.

- ALPM is working to improve customer orientation behavior among the sales force to enhance its market share. It is also using Artificial intelligence (AI) for better productivity.

- Moreover, the addition of sales force is expected to drive better outlook in the DF segment going forward.

- Over the past 12M, ALPM’s prescription base has been 131m.

- We expect a 6% sales CAGR over FY25-27, reaching INR26.2b. Reiterate Neutral

- We tweak our estimates for FY26/FY27 (+3%/+2%), factoring in: a) improved business prospects in the exports market and b) near-term disruption in the DF segment. We value ALPM 22x 12M forward earnings to arrive at a TP of INR990.

- After a muted performance in FY25, ALPM is working to improve business prospects across its key markets. Growth in exports markets is strengthening on the back of new launches and superior supply chain management. However, this is being offset to some extent by an inferior show in the DF and API segments. Considering these aspects, we expect a 24% earnings CAGR over FY25-27. The current valuation largely factors in the earnings upside. Hence, we reiterate a Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Buy Cyient Ltd for the Target Rs 830 by Motilal Oswa...

The Art of Slow Living: Why Slowing Down Can Improve...

Government institutes framework to strengthen cybers...

Over 77 lakh annual FASTag passes issued, register 6...

Quote on Technical Market Commentary for July 22nd, ...

Maruti Suzuki India to hike car prices by up to Rs 3...

Buy Mahindra Logistics Ltd For Target Rs. 507 by Pr...

Women's Short and Stylish Kurti: The Perfect Blend o...

Resistance : 24150 (Pivot Level) and 24300 (Key Resi...

Economic activity posted strong expansion in June 20...

Tag News

Buy Granules India Ltd for the Target 950 by Emkay Global Financial Services Ltd

Buy Divi's Laboratories Ltd For Target Rs.7,375 by Choice Institutional Equities Ltd

Pharma Sector Update : Healthy Growth Driven by Strong Demand and Product Expansion- Choice Institutional Equities Ltd

Pharma Sector Update : Coverage Companies Deliver Healthy Growth; Margin Pressure Largely Transitory Choice Institutional Equities Ltd