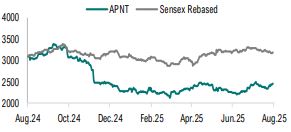

Hold Asian Paints Ltd For Target Rs. 2,777 By Geojit Financial Services Ltd

Green shoot in urban demand adds optimism

Asian Paints Ltd. (APNT), is engaged in the business of manufacturing, selling and distribution of paints and related products for home décor. APNT is the market leader in the Indian paint manufacturing industry.

• In Q1FY26, APNT's volume grew by 3.9% YoY, which is marginally better than our estimate, as the early arrival of the monsoon did not dampen demand as much as feared.

• Gross margin improved by 15bps YoY to 42.7% due to benign input prices and backward integration. The company expects input prices to inch up by 1.5-2% due to the imposition of anti-dumping duty on TiO2 imports from China.

• EBITDA margin contracted by 70bps YoY to 18.2% due to higher sales and marketing spending. However, the management maintained its EBITDA margin guidance of 18-20% for FY26.

• Urban markets are showing early signs of recovery, and a good monsoon is expected to support overall demand. At the same time, the company’s key backward integration projects such as the white cement plant in Dubai—are nearing completion, with output benefits expected to begin from the next quarter.

Outlook & Valuation

We expect the competition intensity to continue in the near term and expect a recovery in demand from H2FY26 on account of festival season and post-monsoon season demand. We, therefore, revise our rating to HOLD from Reduce with a revised target price of Rs. 2,777, based on a P/E of 55x (~10% discount to its 5- year average) on FY27 EPS.

Key Concall Highlights

• The company is expecting single digit volume/value growth in FY26.

• Expectations of better monsoons coupled with benign oil prices are near-term tailwinds for the industry.

• Backward integration processes are progressing well, the white cement plant with a capacity of 2.75 lakh ton is expected to become operational in Q2FY26.

• The VAM-VAE emulsion plant in Dahej is likely to become operational in Q1FY27.

• The new products contributed to over 14% of overall sales in Q1FY26.

• The company expects capex of Rs 700cr for FY26.

• The company maintained EBITDA margin guidance of 18-20% for FY26

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer SEBI Registration Number: INH200000345