Buy Suzlon Energy Ltd for the Target Rs. 78 by JM Financial Services Ltd

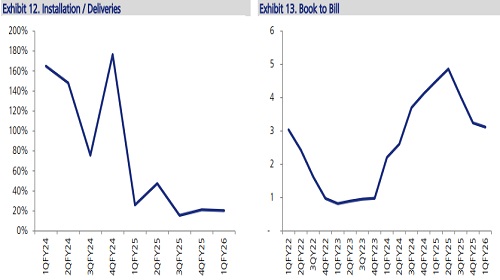

Suzlon Energy Ltd (Suzlon) reported 1QFY26 consol. revenue of INR 31.3bn (55% YoY/ -3% JMFe) driven by higher deliveries (62% YoY). EBITDA came in at INR 6bn (62% YoY/ 1% JMFe) with improvement in margins to 19% vs. 18% in 1QFY25 due to operating leverage. Post adjustment of reversal of DTA which was created in FY25, Adj. PAT stood at INR 4.6bn (7% YoY/ -2% JMFe). With the manufacturing capacity of 4.5 GW and an order book of 5.7 GW, the company is confident of 60% growth in key performance parameters. As utilities’ new renewable energy tenders slow down, commercial and industrial customers are driving growth, especially in wind power. Current installations have consistently stayed at c.20% of the deliveries over the past three months for the last three quarters, which is a cause for concern. Considering deliveries of 2500 MW/3100 MW in FY26/FY27, we arrive at an EPS of INR 1.51/ INR 2.31 during FY26/FY27 and, maintain our BUY rating on the stock with a revised TP of INR 78 based on a 35xFY27 EPS.

* Segment Performance: Strong WTG (wind turbine generator) deliveries (444MW/ 274MW for 1QFY26/ 1QFY25) led to revenue and EBITDA margin to grow to INR 24.9bn/ INR 14.9bn and 15%/ 10% during 1QFY26/ 1QFY25. The installed capacity base for the Operations & Maintenance Services (OMS) business stood at 15.2 GW in 1QFY26 vs. 14.8 GW in 1QFY25. Revenue and EBITDA margin for OMS during 1QFY26/ 1QFY25 stood at INR 4.8bn/ INR 4.4bn and 39%/ 44%. The EBITDA margin for the foundry and forging division was 19% during 1QFY26 vs. 11% during 1QFY25.

* Order book: Suzlon’s order book stood at 5,361 MW as on Jun’25 (3,817 MW as on Jun’25) which increased to 5,742 MW in Aug’25 with a diversified mix (92% 3x MW series; 54% C&I customers; 21% PSU customers; 78% non-EPC; spread across 7 States).

* Deliveries and project execution: India added 1,637 MW of wind energy capacity during 1QFY26 vs. 770 MW during 1QFY25. Suzlon commissioned 117 MW of projects in 1QFY26 vs. 71 MW in 1QFY25. Additionally, 547 MW of WTGs are erected on sites which are ready for commissioning. Deliveries in 1QFY26 stood at 444 MW vs. 274 MW in 1QFY25. Grid connectivity and land remains major challenges in ramp up of installations.

* Push for Make in India: Ministry of New and Renewable Energy (MNRE), on 31st July 2025, mandated wind OEMs to source key components-blade, tower, gearbox, generator, and special bearings only from domestic suppliers. It also mandates wind turbine data and control systems to remain within India, using local data centers, servers, and R&D facilities to improve data security and enhance the country's cybersecurity ecosystem. This is likely to create level playing field for domestic OEMs like Suzlon.

* Guidance: Management maintained earlier guidance for 60% growth on key parameters viz. deliveries, revenue, EBITDA in FY26. It expects India to add 6 GW and 7-8 GW of wind energy capacity during FY26 and FY27.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361

Top News

India a much better destination to invest for European companies