Buy Shriram Finance Ltd For Target Rs. 790 by Motilal Oswal Financial Services Ltd

NIM compression due to excess liquidity; credit costs rise QoQ

Earnings in line; technical write-offs lead to GS3 improvement

* Shriram Finance (SHFL)’s 4QFY25 PAT rose ~10% YoY to ~INR21.4b (inline). FY25 PAT (excluding exceptional gain) grew ~15% YoY to INR82.7b.

* NII in 4QFY25 grew ~9% YoY to INR55.7b (inline). Credit costs at ~INR15.6b (~12% higher than MOFSLe) translated into annualized credit costs of ~2.4% (PQ: 2.1% and PY: 2.3%). PPoP grew ~11% YoY to ~INR43.4b (inline).

* Yields (calc.) rose ~5bp QoQ, while CoB increased ~30bp QoQ to 9.1%, resulting in a spread decline of ~25bp QoQ. Reported NIM also dipped ~25bp QoQ to ~8.25%, primarily because of excess liquidity on the balance sheet. SHFL guided liquidity to normalize within the next two quarters.

* SHFL undertook technical write-offs of ~INR23.5b in 4QFY25, which was P&L neutral but led to an improvement of ~85bp in GS3 to 4.55%. Extechnical write-offs, GS3 rose ~3bp QoQ. Gross Stage 2 (GS2) rose ~20bp QoQ. Management shared that it does not anticipate any further increase in stress or credit costs in the upcoming fiscal year. Additionally, management remains confident that there will be no significant forward flows from the GS2 pool in 1QFY26.

* SHFL’s 4QFY25 was very unlike the typical 4Q of a fiscal year, as (organic) asset quality deteriorated and net slippages continued to remain elevated. 1QFY26 will be an acid test for the vehicle financiers. Hence, we remain cautiously optimistic, as opined in our recent Vehicle Finance Report.

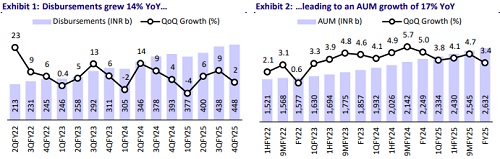

* SHFL expects the overall credit situation to improve, aided by an increase in urban demand (from higher government spending) and rural activity. SHFL continued to guide for AUM growth of 15%+ in FY26 and expects the cost-to-income ratio to decline to ~27-28% by the exit of FY26.

* SHFL has positioned itself to capitalize on its diversified AUM mix, improved access to liabilities, and enhanced cross-selling opportunities. The company has yet to fully utilize its distribution network for nonvehicle products. SHFL is our Top Idea (refer to the report) in the NBFC sector for CY25, given that we find its valuations of 1.7x FY27E P/BV attractive for a strong franchise that can deliver a ~17%/~19% AUM/PAT CAGR over FY25-27E and an RoA/RoE of ~3.3%/17% in FY26. Reiterate BUY with a TP of INR790 (premised on 2x FY27E BVPS).

Credit costs higher QoQ; GS3 improves driven by technical write-offs

* GS3/NS3 improved ~85bp/5bp QoQ to ~4.55%/2.65%. The reduction in GS3 was driven by a technical write-off of INR23.5b. Net slippages were higher in 4QFY25 and stood at INR14b (PQ: INR12b and PY: INR8b).

* PCR on Stage 3 declined ~8pp QoQ to ~43%. (PQ: ~52%). Management shared that it does not expect the S3 PCR to be increased again, but it would instead remain in the range of 43-45%.

* Management continued to guide for credit costs of ~2%, and we estimate credit costs of ~2.0%/2.1% (as % of assets) in FY26/FY27.

NIM to expand due to normalization in liquidity and likely decline in CoB

* A shift in the product mix to high-yielding non-CV products will be marginally accretive to the blended yields.

* Surplus liquidity stood at ~INR31b (PQ: INR27b), and the company expects the liquidity to normalize to INR18-19b within the next two quarters.

* SHFL is well-positioned to benefit from a declining interest rate environment. The recent rate cuts are likely to further support NIM expansion, and we model NIMs of 9.1%/9.2% in FY26/FY27 (FY25: ~9%).

Highlights from the management commentary

* Between 2019 and 2021, CV sales were subdued, resulting in a limited supply of used vehicles in the market. With CV sales picking up from FY22 onwards, the availability of used vehicles and the volume of used vehicle transactions are expected to increase from FY27.

* Certain rural segments in central parts of India (Chhattisgarh, MP, and some parts of Bihar), alongside their border areas, had some collection impact because of the slowdown in the economy. The situation has improved now, and the company does not see any scope for further deterioration in asset quality.

Valuation and view

* SHFL delivered a decent operational performance during the quarter, supported by healthy growth in AUM and disbursements. Although credit costs in the quarter were higher than guidance, the company does not foresee any further stress or deterioration in asset quality in FY26. Moreover, it anticipates an improvement in the overall credit environment, which is expected to sustain healthy AUM growth. NIMs are expected to revert to previous levels and further expand as excess liquidity on the balance sheet normalizes.

* SHFL is effectively leveraging cross-selling opportunities to reach new customers and introduce new products, which will lead to improved operating metrics and a solid foundation for sustainable growth. The current valuation of ~1.7x FY27E P/BV is attractive for ~19% PAT CAGR over FY25-27E and RoA/RoE of ~3.3%/ 16.0% in FY27E. Reiterate BUY with a TP of INR790 (based on 2x FY27E BVPS)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412