Buy Nuvoco Vistas Corp Ltd for Target Rs. 500 by Choice Institutional Equities

Cost pressures trigger TP cut; BUY maintained on strong structural growth outlook

We retain our BUY rating on NUVOCO, while revising the TP down to INR 500/sh (from INR 560 earlier). The downgrade reflects earnings cuts of ~9.9% in FY27E and ~2.7% in FY28E, driven by rising input cost pressures amid geopolitical uncertainty:

a) Fuel cost remains the key overhang — the management highlighted blended fuel cost at INR 1.44/mn kcal, expected to rise to INR 1.51– 1.55/mn kcal in Q1 with a further uptick likely in Q2, led by higher pet coke and imported coal prices.

b) Additionally, sharp inflation in packaging cost is emerging as a new concern. PP granule prices have surged from ~INR 99/kg in Feb to ~INR 155/kg in April, translating into an incremental INR 100–120/t cost impact, factoring in higher granule and conversion cost.

To offset rising cost pressures, NUVOCO has initiated price hikes of INR 10–12/bag in April, with a scope for further increases if pricing sustains. On the fuel side, the company is actively optimising its mix — reducing pet coke usage from ~60% to 50%, with a target to bring it down to ~45%, which should help mitigate cost escalation.

Despite these measures, we estimate overall cost/t to rise by ~INR 230/t in FY27E, leading to an EBITDA/t of ~INR 838/t in FY27E.

We continue to be constructive on NUVOCO despite ongoing geopolitical volatility, supported by 1) Higher cement prices (prices hiked in April 2026), leveraging strong demand momentum, 2) 70% presence in the eastern market and 3) Strong capacity addition of 10 Mtpa by FY27E. Based on our realistic assumption, NUVOCO’s ROCE is anticipated to expand by 370 bps, from 6.5% in FY26 to 10.2% in FY29E. NUVOCO continues to be amongst our high-conviction ideas

We forecast NUVOCO’s EBITDA to expand at a CAGR of 9.8% over FY26–29E based on our volume growth assumption of 6.0%/8.0%/10.0% and realisation growth of 3.0%/1.0%/1.0% in FY27E/28E/29E, respectively. We arrive at a 1-year forward TP of INR 500/share for NUVOCO. We value NUVOCO on our EV/CE framework – we assign an EV/CE multiple of 1.4x/1.4x for FY27E/28E.

Risk to the thesis:

Geopolitical volatility risk: Possible prolonged geopolitical disruption could lead to an increase in petcoke price, resulting in higher input cost and margin pressure.

Q4FY26 & FY26 result: Volume momentum strong; Margin recover QoQ

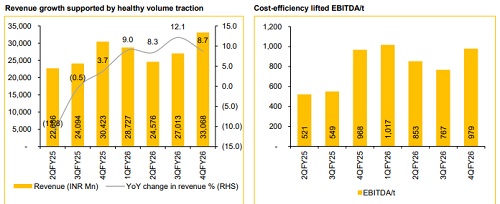

NUVOCO reported Q4FY26 consolidated revenue and EBITDA of INR 33,068 Mn (+8.7% YoY, +22.4% QoQ) and INR 5,876 Mn (+6.5% YoY, +53.1% QoQ) vs CIE est of INR 33,230 Mn and INR 6,108 Mn, respectively. For FY26, revenue and EBITDA stood at INR 113.4 Bn (+9.5% YoY) and INR 18.6 Bn. Total volume for Q4 stood at 6.0 Mnt (vs CIE est. 6.0 Mnt), up 5.3% YoY and up 20.0% QoQ. For the full year, volume was 20.4 Mnt, up 5.2% YoY.

Realisation/t came in at INR 5,511/t (+3.3% YoY and +2.0% QoQ), which is in line with CIE’s estimate of INR 5,500/t. Total cost/t came in at INR 4,532/t (+3.7% YoY and -2.2% QoQ). As a result, EBITDA/t came in at INR 979/t, which is an increase of ~INR 212/t QoQ. For FY26, EBITDA/t stood at INR 910/t, up 28.7% YoY.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131