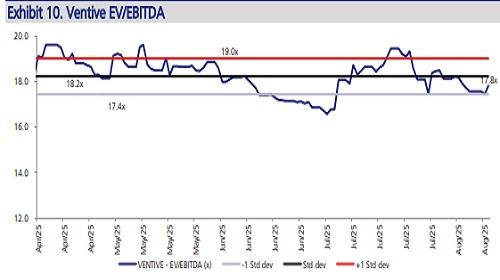

Buy Ventive Hospitality Ltd for the Target Rs. 154 by JM Financial Services Ltd

Ventive Hospitality’s (Ventive) earnings print was a mixed bag: revenue of INR 5.1bn (+18% YoY) was in line while EBITDA was a ~3% miss on JMFe (INR 2.1bn, +13% YoY). The India hospitality and international portfolio recorded 7% and 11% YoY growth in RevPAR and (same-store) TRevPAR respectively. Raaya in Maldives continues to do well and remained EBITDA positive during the quarter. With an extremely comfortable leverage position and steady cash flows from its existing portfolio, the company is well positioned to fund the addition of 1,582 keys across 8 upcoming hotels (including pipeline assets and ROFO). We estimate revenue/EBITDA CAGR of c.13%/15% respectively over FY25-28E, with a 200bps improvement in EBITDA margin. We maintain BUY rating and a target price (TP) of INR 890, valuing the company on an SoTP basis.

* Steady performance with double-digit ARR growth: Ventive reported consolidated revenue of INR 5.1bn (+18% YoY, -27% QoQ, in line) and EBITDA of INR 2.1bn (13% YoY, 3% miss on JMFe) as margin declined 230bps due to consolidation impact of Raaya. Indian hospitality revenue was up 13% YoY and EBITDA was up 28% YoY, due to impact of heat wave and general elections in the base quarter. The portfolio witnessed 10% YoY growth in ARR to INR 19,498, while the occupancy declined 180 bps to 60.5%, resulting in 7% YoY uptick in RevPAR. The management highlighted that c. 40% of F&B revenue in India is driven by MICE and weddings, with the balance coming from restaurants. Also, c. 80% of F&B income comes from non-resident guests, thus making the revenue stream independent of occupancy.

* Raaya continues to remain EBITDA positive: The Maldives portfolio reported 33% YoY growth in revenue led by consolidation of Raaya. On a same-store basis, revenue was up 11% YoY, driven by similar uptick in TRevPAR. The management noted that Raaya’s occupancy was in line with industry benchmarks and the asset continues to remain positive at EBITDA level. It had delivered ~50% EBITDA margin in 4QFY25 (best quarter for the region) and outperformed the company’s other two assets in the region.

* Development pipeline update: Ventive has an expansion pipeline of 1,582 keys across 8 eights, of which 4 hotels (482 keys) will be developed by the company. The remaining 4 assets will be developed by the promoter group and will be made available to Ventive on a ROFO basis. The company has budgeted a cumulative outflow of c. INR 22bn towards development of owned assets (INR 10bn) and funding the ROFO pipeline (INR 12bn). The management expects the company to generate a total EBITDA of c. INR 65bn over the next 5 years, which will result in INR 45bn surplus – thus providing sufficient liquidity to fund the expansion. Ventive is also actively evaluating other growth opportunities especially in the high-end leisure and wellness segment.

* Maintain BUY with a Sep’27 TP of INR 890:

\We maintain our BUY rating and a target price (TP) of INR 890, valuing the company on an SoTP basis.? Earnings concall highlights: - The company expects industry level occupancy to reach 70-75% in Pune, driven by growing office space absorption, Navi Mumbai airport and strong influx of GCCs - It is confident of delivering mid-teens top line growth along with high teens growth in EBITDA - Strong growth in Maldives portfolio was led by stabilisation in Raaya’s performance. - Gross debt stood at INR 22bn, comprising INR 13bn of rupee-denominated debt and the balance being USD-denominated debt. While the Maldives debt is USDdenominated, revenue booking also happens in the same currency, thereby providing a natural hedge against currency movements - The new airport terminal in Maldives can support tourist traffic of 7mn compared to 2mn earlier, thus enabling higher ARRs and occupancies - While there is no legal obligation to go with Marriott, its robust distribution network and broad brand spectrum makes it one of the most preferred brands globally

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361