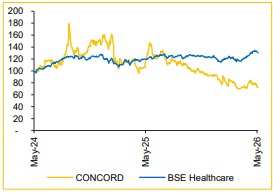

Reduce Concord Biotech Ltd for Target Rs.1,045 by Choice Institutional Equities

Scale-up Challenges Continue to Weigh on Growth Visibility

While the underlying demand environment and long-term growth drivers remain intact, the company continues to face near-term challenges arising from geopolitical disruption, tariff-related uncertainty and delays in regulatory approvals. We believe the next phase of growth will depend on the company’s ability to successfully ramp up its key growth engines. The management remains confident of sustaining historical revenue growth of ~18%; however, we conservatively forecast a revenue CAGR of 15% over FY26–29E, along with ~150bps EBITDA margin expansion in FY27E. That said, we remain watchful for a meaningful contribution from the injectables facility, which we believe is critical to driving a sustained recovery in both, growth and profitability. In view of the ongoing West Asia crisis and delayed approvals, we revise our FY27/28E estimate downwards by 18.5%/13.1%, respectively. We continue to value the stock at 30x FY28E EPS, arriving at a revised TP of INR 1,045 with a ‘REDUCE’ rating.

Revenue Growth Healthy; PAT Miss Weighs on Quarter

* Revenue declined 24.1% YoY and increased 17.4% QoQ to INR 3,261 Mn (vs. CIE estimate: INR 3,632 Mn).

* EBITDA declined 37.8% YoY and increased 19.8% QoQ to INR 1,185 Mn (vs. CIE estimate: INR 1,224 Mn); margin contracted 795 bps YoY and 72 bps QoQ to 36.4% (vs. CIE estimate: 33.7%).

* Adj PAT declined 36.8% YoY and increased 32.7% QoQ to INR 888 Mn (vs. CIE estimate: INR 932 Mn)

Successful Scale-up Key to Delivering Growth and Margin Recovery FY26 was a challenging year for the company due to multiple external disruption, including Middle East tender deferments and a slowdown in US orders amid tariffrelated uncertainty. Additionally, delays in CDSCO approvals and a slower-thanexpected ramp-up of the injectables facility impacted performance. Consequently, EBITDA margin also contracted sharply during the year. However, the management remains confident of returning to growth in FY27E, driven by:

* API: The segment is expected to remain the primary growth driver, supported by scale-up of products, such as Nystatin, new customer additions and continued traction in oncology APIs.

* Formulations: Key growth drivers include ramp-up of the injectables facility, expansion of the domestic branded business and improving operating leverage in the US Stellon business. While strategic demand for the company’s products remains intact, we believe growth recovery will largely depend on successful execution and scale-up across key initiatives including market expansion. We expect revenue CAGR of ~15% over FY26–29E, while EBITDA margin expansion is likely to remain modest at 100–150 bps in FY27E.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131