Buy NMDC Ltd for the Target Rs.100 by Motilal Oswal Financial Services Ltd

In-line performance;

outlook bright Consolidated result highlights

* 3QFY26 revenue stood at INR76.1b (vs. our est. of INR71.1b), rising 16% YoY and 19% QoQ, primarily driven by improved volumes and better NSR.

* Iron ore production stood at 14.7mt (+11% YoY and +44% QoQ), while sales came in at 12.7mt (+6% YoY and +19% QoQ).

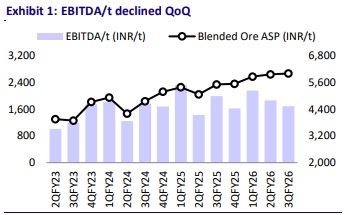

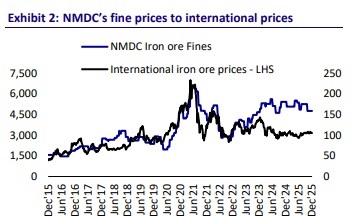

* ASP stood at INR5,993/t (+9% YoY and +1% QoQ).

* EBITDA stood at INR21.4b (-10% YoY and +8% QoQ) and was in line with our estimate. EBITDA/t came in at INR1,688/t (-15% YoY and -9% QoQ), against our est. of INR1,766/t.

* APAT stood at INR17.6b (-7% YoY and +3% QoQ), against our estimate of INR17.4b.

* During 9MFY26, revenue/EBITDA grew 23%/9% YoY to INR207.3b/INR66.2b, primarily supported by volume growth and healthy realization. 9MFY26 adj. PAT increased 7% YoY to INR54.2b. In 9MFY26, sales volume rose 10% YoY to 34.9mt and ASP increased 11% YoY to INR5,934/t.

Valuation and view

* NMDC reported decent earnings during the quarter, supported by healthy volume and NSR. Going forward, we expect volumes to pick up steadily to ~51mt in FY27 and 54mt in FY28, fueled by an increasing EC limit. We largely maintain our estimates for FY27/28 and expect volumes and prices to remain elevated, in line with strong demand from steel makers.

* NMDC has planned capex of over INR700b for various evacuation and capacity enhancement projects, aimed at improving the product mix and increasing production capacity to ~100mt by FY29-30.

* Additionally, NMDC is expected to generate strong OCF over FY26-28. This will support its capex plan without overleveraging.

* At CMP, the stock trades at 5.3x EV/EBITDA and 1.8x on P/BV on FY27 estimate. We reiterate our BUY rating on NMDC with a TP of INR100 (based on 6.5x EV/EBITDA on Sep’27 estimate).

* Key risks – a) rising competition from captive iron ore mining, b) Karnataka mineral tax demand, which could impact earnings if ruled against NMDC, and c) delay in acquiring the target EC limits.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412