Buy JSW Steel Ltd for the Target Rs.1400 by Motilal Oswal Financial Services Ltd

Favorable macros to support margin recovery; longterm growth backed by capacity expansion

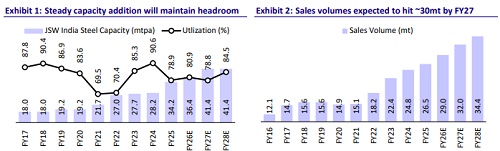

Volume growth through strategic capacity expansion

* JSW Steel (JSTL) has outlined a structured expansion roadmap targeting ~56MTPA crude steel capacity by FY31 (India ex-BPSL: 50MTPA). The 5MTPA integrated steel plant at Jagatsinghpur (Odisha) remains the cornerstone project, comprising BF, SMS, and HSM (900–2,150mm) with ~350MW CPP. The coastal location, with port connectivity and a slurry pipeline, ensures logistics efficiency. Phase-II scalability to 13.2MTPA is embedded upfront, lowering future capex intensity.

* The 5MTPA JVML facility is fully ramped up, and the BF-3 upgrade (shutdown initiated in end-Sep’25) will add ~1.5MTPA by 4QFY26, supporting incremental volumes from FY27 onward.

* The expansion of the Dolvi facility from 10MTPA to 15MTPA (capex ~INR210b; completion by Sep’27) is expected to strengthen the company’s positioning in Western India and in export markets. Additionally, the 1MTPA EAF at Kadapa (INR38b; commissioning by FY29) will enhance the long-product portfolio and provide decarbonization optionality.

* The company plans ~INR1t of investment over 4–5 years (FY26 capex guided at INR150–160b; INR100b spent in 9MFY26), covering Odisha Phase-I, Dolvi Phase-III, downstream VAP, mining, and renewable energy (RE). Funding will be supported by internal accruals, INR320b proceeds from BPSL, and disciplined leverage management.

Cost leadership via resource optimization and raw material security

* The company is accelerating backward integration to structurally lower input volatility and support its ~50MTPA capacity target by FY31. Iron ore captive sourcing is expected to range in 30-40% in 2HFY26, with a long-term target of ~50%. Incremental iron ore volumes are expected from three Karnataka mines (~4mt from 1QFY27) and Goa mines (~3.7mt across FY26-27), while 2 x 8MTPA pellet plants in Odisha (by FY28) will further enhance integration.

* On coking coal, the company has secured domestic blocks in Jharkhand (2.2MTPA), which is expected to ramp up in 2-3 years. Internationally, the company has increased its stake to 30% in Illawarra Metallurgical Coal (~1.2MTPA offtake of PLV coal) and is pursuing the Minas de Revuboè project (Mozambique) to secure high-grade supplies, improving sourcing diversification.

* Logistics integration is being strengthened via a 302km (30MTPA) slurry pipeline by FY27, linking the Nuagaon mines to the Jagatsinghpur plant. Additionally, the company is developing the 30MTPA Jatadhar Port by FY27 to increase port throughput, along with expanding dedicated rail capacity.

* Additionally, renewable integration is scaling up, with ~1GW of installed capacity and Board approval for 2.5GW of RE capacity along with 320MWh of battery storage, supporting decarbonization and long-term energy cost optimization

Premiumization through VASP portfolio enhancement

* JSTL continues to shift toward higher-margin value-added and special products (VASP), which contributed ~67% (ex-JVML) to 3QFY26 volume.

* At Vijayanagar, key downstream projects include a 0.4MTPA Continuous Galvanising Line (Jun’28 target) focused on high-strength automotive grades and a 0.55MTPA CRNO electrical steel plant (Mar’28 target). Additional expansions include tinplate and galvanized/galvalume capacities, along with EAF-based green steel projects.

* While current production at JVML Vijayanagar remains relatively higher upstream, the commissioning of downstream facilities will progressively increase the share of high-value products, strengthening margins.

Valuation and outlook

* We believe JSTL is well-placed with new capacities coming on-stream, strong domestic demand, and a rising share of value-added proportion in the sales mix. Its focus on increasing the captive share of iron ore and improving coal linkages will support earnings.

* Going forward, we estimate double-digit revenue growth over FY26-FY28, driven by the ramp-up of new capacity and price recovery led by safeguard duty. Further, as input costs are expected to remain steady, we believe EBITDA/t will rebound to ~INR13,500/t in FY27/28E on account of domestic steel price recovery, led by safeguard duty.

* Strong margins will enable JSTL to generate a strong CFO to fund the expansion plan of INR150-200b annually over FY26-29E. JSTL’s net debt/EBITDA stood at 2.9x as of 3QFY26, which we expect to decline further by FY28, supported by robust operating performance.

* At CMP, JSTL trades at 7.6x FY28E EV/EBITDA, and we reiterate our BUY rating on the stock with a TP of INR1,400 (premised on 9x EV/EBITDA on Sep’27 estimate)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041