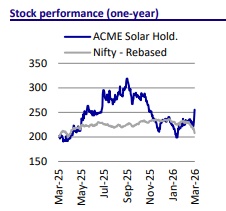

Buy ACME Solar Ltd for the Target Rs.341 by Motilal Oswal Financial Services Ltd

Strong earnings visibility backed by PPAs; BESS upside

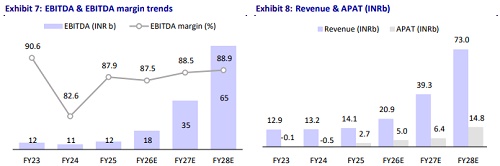

* ACME Solar’s (ACME) portfolio currently stands at 8.1GW (comprising ~3GW operational capacity and ~5.1GW under construction), with ~78% of capacity backed by PPAs, providing strong earnings visibility. As projects under construction are commissioned, operational capacity is expected to increase from ~2.5GW at end-FY25 to ~5.5GW by end-FY28, driving EBITDA/APAT CAGR of ~74%/76% over FY25–28.

* In addition, ACME plans to fast-track BESS deployment linked to its FDRE projects, leveraging its existing operational sites. The company is targeting ~2GWh commissioning in 4QFY26 and another ~2GWh in 1QFY27, with a broader goal of ~10GWh by end-CY27 under 25-year PPAs. This potential BESS ramp-up has not been incorporated into current estimates, representing a potential earnings upside (EBITDA guidance of ~INR1.7b/GWh assuming INR5/unit arbitrage).

* On the execution front, ACME has secured transmission connectivity for almost all of its ~5.1GW under-construction capacity and maintains a ~7.5GW connectivity inventory (1.3GW secured, 6.2GW applied), providing it an upper hand when bidding for future projects and limiting downside risks from execution delays.

* We assign an EV/EBITDA multiple of 9.5x to FY28E EBITDA. Adjusting for net debt, we derive our TP of INR341, implying a 34% potential upside.

74% EBITDA CAGR over FY25–28E, driven by capacity expansion

* We estimate EBITDA/APAT to expand at a CAGR of 74%/76% over FY25-28, driven by an increase in operational capacity from 2.5GW at end-FY25 to ~5.5GW by end-FY28.

* EBITDA margins are expected to remain broadly stable, improving marginally from 87.9% in FY25 to 88.9% in FY28, supported by the commissioning of more FDRE and hybrid projects, which offer higher perunit realizations compared with the current operational portfolio that is largely plain-solar projects.

Accelerated BESS rollout could drive earnings upside

* ACME currently has a total BESS pipeline of ~16GWh, comprising 550MWh of standalone (PPA-backed) projects and ~15.5GWh associated with its under-construction FDRE projects.

* During the 3QFY26 results call, the company indicated plans to fast-track the commissioning of BESS capacity linked to its under-construction FDRE projects at existing operational sites. ACME targets ~2GWh commissioning in 4QFY26 and another ~2GWh in 1QFY27, with a broader goal of ~10GWh commissioned by end-CY27, which will subsequently be integrated with their respective FDRE projects and operate under 25-year PPAs.

* We have not incorporated this potential BESS commissioning into our current estimates, making it a potential earnings upside (the company has guided for EBITDA of ~INR1.7b/GWh, assuming an INR5/unit arbitrage for a single battery charge-discharge cycle).

~78% of ACME’s 8.1GW portfolio backed by PPAs

* ACME’s total portfolio currently stands at 8.1GW, comprising ~3GW of operational capacity and ~5.1GW under construction. The portfolio is largely backed by PPAs, with ~78% of capacity already tied up, providing strong earnings visibility going forward.

* In 2026 YTD, as ACME has already signed PPAs for 890MW of projects, only ~1.8GW of its under-construction pipeline of 5.1GW remains without PPAs. Notably, the majority of this untied capacity comprises FDRE/Hybrid projects, with only a single 300MW solar project yet to secure a PPA, thereby materially reducing any risk associated with future PPA tie-ups.

Bidding activity to gradually pick up as states reassess demand

* As highlighted previously, over 40GW of bid-out renewable projects are still awaiting PPA signings, which has weighed on the pace of new renewable energy bidding activity.

* According to our channel checks, the rebidding of these projects is gradually gaining traction following certain adjustments to bid terms. For instance, Punjab has signed ~1.5GW of FDRE projects, while Bihar has signed ~1–2GW of FDRE projects.

* Once this backlog of pending PPAs is cleared, the renewable bidding trajectory is expected to accelerate meaningfully, with state utilities also playing a larger role in capacity additions, thereby supporting a broader revival in renewable project tendering.

ACME’s strong connectivity pipeline mitigates transmission constraints

* India’s transmission line commissioning pace continues to lag behind targets. In FY25, the country added 8,830ckm of transmission lines against a target of 15,253ckm. The trend has persisted in FY26, with 7,398ckm commissioned during 10MFY26 vs. a target of 17,480ckm.

* With the new supplementary Right-of-Way (RoW) guidelines issued in December 2025, which tighten the land?valuation methodology and timelines, transmission?line RoW delays are expected to moderate.

* ACME has already secured transmission connectivity for almost its entire 5.1GW under-construction capacity.

* Additionally, the company maintains a pipeline of transmission connectivity for future bids, and as of end-3QFY26, it reported a connectivity inventory of ~7.5GW (1.3GW secured and 6.2GW applied), which could provide it with a competitive advantage in bidding for upcoming RE projects.

IPP competitive landscape is evolving to cater to the demands of the industry

* Amid increasing grid stability concerns, states are progressively favoring demand-centric renewable projects such as FDRE and RTC projects over conventional standalone solar projects. This shift in project structures has raised the complexity of bidding and execution, making it more challenging for smaller developers to offer competitive tariffs, with many remaining largely confined to vanilla solar or wind projects.

* Additionally, the higher capital intensity associated with such projects, driven by incremental costs related to battery storage and hybrid configurations, acts as a deterrent for potential bidders.

Valuation and view

* We reiterate our EV/EBITDA-based TP of INR341, valuing the stock at 9.5x FY28E EBITDA.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)