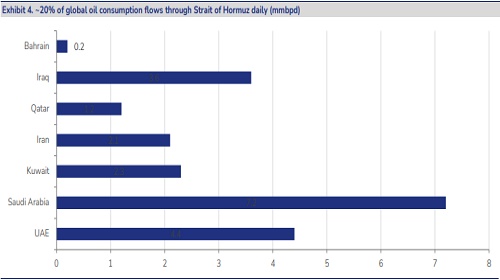

Oil and Gas Sector Update : Government clarifies on India’s energy security amid ME crisis By JM Financial Services Ltd

In a press briefing, the Indian government (GoI) has addressed issues around India’s energy security and current energy position amid blockage of oil and gas flows via the Strait of Hormuz (SoH) due to ongoing Middle East (ME) crisis. The briefing states India’s 30% crude and 25% natural gas requirements are currently impacted due to the SoH blockage despite taking various sourcing diversification measures. We believe India’s total oil inventory would be sufficient for meeting three–four months of current domestic oil demand shortfall if India’s crude imports from the SoH continue to be halted. However, we see a need for 20–25% gas demand rationalisation across sectors as the only sustainable way to offset the current gas requirement shortfall amidst minimal gas inventory. Furthermore, the blockage of SoH has impacted India’s LPG requirements the most with 44% still unmet (despite 25% rise in domestic LPG production) as 60% of our LPG requirements is imported - of which 90% comes from SoH and has ground to a halt. As per our understanding, ~85% of India’s LPG consumption is for domestic consumption and the balance ~15% for commercial usage. Though the GoI has prioritised LPG allocation for domestic cooking fuel usage, our current overall LPG availability of 56% even falls short of meeting domestic LPG demand; hence, availability for commercial LPG supply may continue to be a challenge.

* 30% of India’s crude requirements impacted due to blockage of SoH, though India’s crude and petroleum products inventory sufficient to meet this shortfall for 3–4 months: The GoI said India’s current daily crude consumption is 5.5mmbpd and 70% of India’s crude imports are coming in from routes other than the Strait of Hormuz (versus 55% earlier) as a result of various diversification efforts. This implies 30% of our crude requirements has been impacted given that crude imports meets 85% of India’s overall oil demand. However, it clarified that India’s refining capacity is currently operating at full utilisation of~100% (mostly due to 10–50 days of crude inventory that various refineries have). As per our understanding, India’s total crude and oil product inventory (industrial + strategic) is likely equivalent to meeting 30–40 days of domestic demand assuming: a) IOCL maintains 45–50 days of crude inventory and another 10–15 days of product inventory (1/3rd of India’s refining capacity); b) other refiners maintain 10–20 days of crude inventory and another 10–15 days of product inventory; and c) strategic crude reserve of ~6 days (~30mmbbbl). Hence, if India’s crude imports from SoH continues to be halted, India’s total oil inventory would be sufficient for meeting 3–4 months of domestic oil demand shortfall (~85% of India’s oil consumption is imported and ~30% of imports via the Strait is disrupted).

* 25% of India’s natural gas requirements impacted due to SoH blockage; 20–25% demand rationalisation only sustainable way to offset this shortfall amidst minimal inventory: The GoI said India’s natural gas consumption is ~189mmscmd, of which 97.5mmscmd is produced domestically and remaining the ~92mmscmd is imported; ~47.4mmscmd out of these gas imports has been impacted currently due to force majeure conditions (or 25% of our total gas supply has been disrupted). Indian gas companies are trying to procure additional gas via alternative routes to offset this disruption, and two LNG cargoes are on their way to India. Earlier yesterday, the government had issued a Natural Gas (Supply Regulation) Order, 2026 to ensure availability of gas for priority sectors (100% supply to Domestic PNG, CNG, LPG production and pipeline compressor fuel, 70% to fertilisers and 80% to tea, manufacturing and industrial consumers based on last 6-month average consumption) while curtailing supplies to the petchem, power and refining sectors. Given India doesn’t have much inventory of gas (given the challenges in storing gas due to nature of commodity), 20–25% demand rationalisation across sectors is the only sustainable way to offset the 25% disruption in our overall gas supply.

? 44% of India’s LPG requirements impacted, even after 25% rise in domestic LPG output; LPG supply can meet 56% of our demand, so commercial LPG supply may continue to be disrupted: The GoI clarified that India imports ~60% of LPG requirements (and 40% produced domestically) and 90% of these imports (i.e. ~54% of our LPG demand) come via the SoH. This implies 54% of India’s overall LPG supply is disrupted currently. To offset this, the GoI has ordered Indian refining and petchem companies to maximise LPG by diverting all C3-C4 hydrocarbon streams, which will add to LPG pool and will be supplied to OMCs to meet domestic LPG supply. These measures have led to a rise in domestic LPG production by 25% and entire domestic LPG is being diverted to the household segment. This implies LPG supply is only able to meet 56% of our requirement (domestic production is now meeting 50% of our requirement versus 40% earlier and another 6% of demand being met from imports made through routes other than the SoH). Hence, still 44% of our LPG requirements is unmet. For non-domestic LPG, priority is given to essential sectors like hospitals and educational institutions. Furthermore, India's oil ministry has set up a three-member panel of OMC executives to review the allocation of LPG supply to restaurants, hotels and other commercial users and is trying to work out a mechanism to ensure available LPG is distributed in fair and transparent manner.

* GoI prioritises LPG allocation for domestic cooking fuel usage; commercial LPG availability may continue to be a challenge : As per our understanding, ~85% of India’s LPG consumption is for domestic consumption and the balance ~15% is for commercial organisations (hospitals, educational institutes, restaurants/hotels, temples, etc). Hence, our current overall LPG availability of 56% even falls short of meeting domestic LPG demand (which constitutes 85% of our overall LPG demand). Hence, commercial LPG supply may continue to be a challenge. Separately, the GoI added that it has absorbed a significant part of the jump in global LPG prices to protect consumers despite the recent hike of INR 60/cylinder; current domestic LPG price is INR 913/cylinder in Delhi (and INR 613/cylinder for PMUY customers). It also clarified that panic domestic LPG booking is due to misinformation and there is no shortage of domestic LPG supply. Furthermore, it is trying to prevent diversion of domestic LPG for commercial LPG usage via OTP verification. As a temporary demand management measure, minimum booking time has been increased to 25 days (from 21 days).

Natural Gas (Supply Regulation) Order, 2026

Aims to ensure equitable distribution & availability of gas for priority sectors

The GoI has issued a Natural Gas (Supply Regulation) Order, 2026 to ensure equitable distribution and availability of gas for priority sectors:

a) Priority gas allocation (based on last 6-month average consumption):

i) 100% supply to Priority Sector I: Domestic PNG, CNG for transport, LPG production (including shrinkage), and pipeline compressor fuel.

ii) 70% supply to Priority Sector II: Fertiliser plants. iii) 80% supply to Priority Sector III: Tea industry, manufacturing and other industrial consumers connected to the national gas grid.

iv) 80% supply to Priority Sector IV: Industrial and commercial consumers supplied via CGD networks

b) Gas supply may be curtailed from following non-priority sectors to meet priority sector demand:

i) Petchem facilities (OPaL, GAIL Pata plant); ii) Power plants and iii) Refineries (gas allocation to oil refineries may be reduced to ~65% of their past six-month average consumption).

c) PPAC will notify a pooled gas price for gas diverted from non-priority to priority sectors. Priority sector consumers must accept the pooled price and cannot litigate under force majeure mitigation supply.

d) GAIL, in coordination with PPAC, will manage gas supply diversion and allocation. The order overrides existing Gas Sale Agreements (GSAs) and commercial arrangements if inconsistent with the regulation.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...