Monthly Auto Sales Update- April 2026 by ARETE Securities Ltd

Auto dispatches declined ~2% MoM in April, while YoY growth remained robust at ~34% (due to higher growth in 2W due to a low April 2025 base for Hero). Exports grew ~9% MoM and ~51% YoY, driven by a sharp surge in Bajaj, with export mix at ~22%. PVs held steady on domestic demand with EVs maintaining mid-teens share; CVs saw the sharpest MoM correction as year-end inventory normalization set in, though YoY growth remained intact at ~14%; Tractors benefitted from Akha Teej demand and continued Rabi harvest activity; 2Ws were mixed MoM but broadly positive YoY ex the Hero base effect. The start of FY27 reflects a more normalised demand environment after the strong FY26 exit.

PV Segment

Domestic PV dispatches were broadly flat MoM and grew ~25% YoY in April, with 12% QoQ growth in Maruti Volumes and decline in sequential volumes of the rest. Export volumes declined overall at 10% QoQ with only M&M posting 25% sequential jump, while the rest declined.

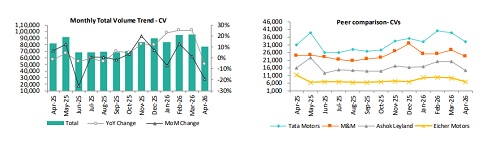

CV Segment

CV dispatches declined ~28% MoM, as expected given the significant channel-filling that typically characterises the March year-end. YoY growth remained positive at ~15%, supported by continued traction in trucks and SCVs. Trucks (contributing ~60% of CV volumes) declined sharply MoM at ~33% across all OEMs but remained up double-digits YoY. LCVs and buses also corrected sequentially by 15% and 24% respectively.

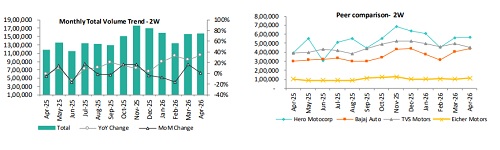

2W Segment

2W volumes were broadly flat to slightly negative MoM at the industry level (Hero -5% MoM, TVS -9% MoM), with Bajaj as an outlier at +15% MoM driven by a sharp surge in exports (230k units vs 159k in March). YoY industry growth appears optically elevated at ~38% due to Hero's anomalously low April 2025 base (~305k units); on a normalised basis ex-Hero, 2W volumes grew ~21% YoY. E2W volumes at TVS were 37.9k units, down 3% MoM but up 36% YoY. For FY27, demand trends in 2Ws are constructive - rural recovery, new model launches, and export momentum at Bajaj/TVS remain supportive

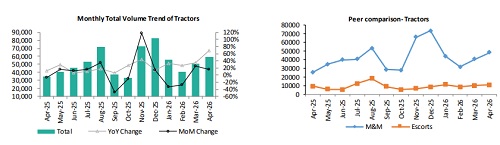

Tractor Segment

Domestic tractor dispatches rose ~4% MoM and ~22% YoY in April, supported by Akha Teej festival activity and continued Rabi harvest momentum. Good reservoir levels and a favourable Rabi crop output sustained rural demand. M&M led with a 7.5% MoM and 21% YoY domestic increase, while Escorts Kubota corrected 10% MoM on normalisation but grew 24% YoY. Export volumes recovered sequentially for M&M after weakness in March, up 23% MoM, while Escorts declined 14% MoM.

Please refer disclaimer at http://www.aretesecurities.com/

SEBI Regn. No.: INM0000127

More News

Pharma Sector Update : Pharma Firms Steady Amid Tariff Turmoil Choice Broking Ltd