Oil and Gas Sector Update : Energy on the boil: Impact on upstream, OMCs and Gas cos By JM Financial Services

Brent crude price has jumped to ~USD 81/bbl and LNG price has soared due to shutdown of key oil and gas assets in the Middle East (shutdown of QatarGas’ huge ~82mmtpa LNG export plant), and as shipment via the Strait of Hormuz (through which nearly 20% of global oil and LNG flows) continues to be disrupted. Further upside risk to crude price exists (can easily jump to USD 90– 100/bbl in the near term) if Iran is able to block the key strait for a prolonged period (though it is a low-probability event based on historical precedents of past wars); US President said if necessary US Navy will begin escorting tankers via Strait and US DFC to provide insurance to ensure financial security of all maritime trade. India’s domestic oil demand is ~5.2mmbpd and inventory is sufficient to meet demand for 3-3.5 months if crude imports via Strait are reduced to zero; but, gas inventory is likely to be limited. ONGC and Oil India are likely to be the key beneficiaries if Brent sustains above ~USD 70/bbl (with the earlier ~USD 75/bbl cap on realisation no longer applicable); every USD 1/bbl increase in oil price boosts their EPS by 1.5–2% each. However, every USD 1/bbl rise in oil price above ~USD 70/bbl hits OMCs’ auto-fuel GMM by INR 0.55/ltr and consolidated EBITDA by 7–9%. Shutdown of Qatar’s LNG exports will impact 35- 40% of India’s LNG imports (and 50% of PLNG’s LNG imports); hence, it is a near-term negative for PLNG, GAIL, Gujarat Gas and other gas companies

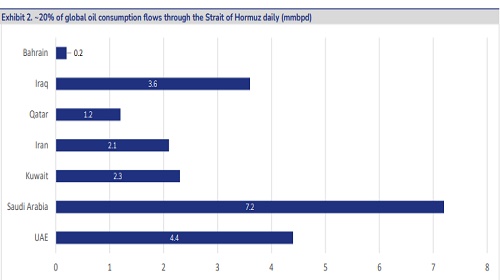

* Brent jumps to ~USD 81/bbl and LNG price surges due to shutdown of key oil and gas assets in the Middle East, and as shipment via the Strait continues to be disrupted: The price of Brent crude has jumped further to ~USD 81/bbl as there are no signs of de-escalation in tensions in the Middle East (ME) with the US President saying war can last for 4-5 weeks or longer. Iran is responding with strikes against energy infrastructure in Gulf countries, resulting in a disruption of traffic or production suspension/shutdown of the following key energy assets: a) Qatar’s huge, critical 82mmtpa LNG liquefaction plant; b) Saudi Arabia’s 550kbpd Ras Tanura refinery; c) UAE’s port of Fujairah (UAE’s largest oil export hub outside the Strait of Hormuz); d) tanker traffic in the Strait due to attacks; and e) suspension of crude production at Iraq’s largest 1.3-1.5mmbpd Rumaila facility and ~460kbpd West Qurna 2 facility due to lack of transport vessels and storage capacity (exhibits 4-6 for list of key oil and gas assets in ME). Shipments of crude/LNG via the Strait have nearly come to a halt after Iran said the strait was closed and warned it would fire on any ship trying to pass. The Strait of Hormuz is the primary export route for major oil-producing nations such as Saudi Arabia, Iraq, Iran, the UAE and Kuwait, and major gas exporter Qatar. However, the US President has directed US Development Finance Corp (DFC) to provide insurance to ensure financial security of all maritime trade and said that the US Navy would begin escorting tankers via the strait if necessary. Separately, China is pressing Iran to avoid disrupting shipping through the Strait. Also, Saudi Aramco is trying to load crude oil tankers from the Red Sea port of Yanbu, sending oil to the West through its 5mmbpd East-West pipeline..

* India’s domestic oil demand is ~5.2mmbpd and inventory is sufficient to meet demand for 3- 3.5 months if crude imports via the strait are reduced to zero; but, gas inventory is likely to be limited: India’s domestic oil demand is ~5.2mmbpd: a) Indian refineries process ~5.5mmbpd of crude oil (4.9mmbpd of imported crude oil and 0.6mmbpd of domestic crude); and b) net exports is 0.3mmbpd (1.3mmbpd of oil products exports and 1mmbpd of imports) –and Over 40% of India’s crude imports (~2mmbpd) and 55% of LNG imports flow through the Strait (exhibit 22-23 for India’s crude sourcing mix). As per our understanding, India’s total crude and oil product inventory (industrial + strategic) is likely equivalent to meeting 35-40 days of domestic demand assuming: a) IOCL maintains 45-50 days of crude inventory and another 10-15 days of product inventory (1/3rd of India’s refining capacity); b) other refiners maintain 15-20 days of crude inventory and another 10-15 days of product inventory; and c) strategic crude reserve of ~6 days (~30mmbbbl). Hence, if only India’s crude imports from Strait are halted, India’s total oil inventory would be sufficient for meeting 3-3.5 months of domestic oil demand shortfall (~85% of India’s oil consumption is imported and 40% of imports comes via the Strait).

* ONGC/Oil India key beneficiaries if Brent sustains above USD 70/bbl (USD 75/bbl cap no longer applicable); every USD 1/bbl rise in oil price boosts their EPS by 1.5–2% each: ONGC and Oil India will be the key beneficiaries if Brent sustains above ~USD 70/bbl (earlier ~USD 75/bbl cap on realisation no longer applicable after Jan’25 amendment of ORD Act) since every USD 1/bbl rise in oil price boosts their earnings by 1.5–2% each (exhibit 24-29). At CMP, ONGC and Oil India are discounting ~USD 68-70/bbl net crude realisation assuming 7–7.5x FY28E P/E for the standalone E&P business. We have a BUY each on Oil India (TP unchanged at INR 560) and ONGC (TP unchanged at INR 320) based on our Brent crude price assumption of USD 70/bbl and likely oil and gas output growth over the next two–three years. However, we prefer Oil India as it could be a 14–18% earnings-compounding story over the next three–five years driven by: i) strong 20–25% cumulative output growth over FY27–29E aided by commissioning of the Indradhanush gas pipeline; and ii) expansion of NRL refinery from 3mmtpa to 9mmtpa (given management guidance of excise duty benefits continuing for expanded capacity as well).

* OMCs’ auto-fuel GMM likely to be hit if Brent sustains above USD 70/bbl; every USD 1/bbl increase in oil price hits their GMM by INR 0.55/ltr and consolidated EBITDA by 7–9%: OMCs’ auto-fuel gross marketing margin (GMM) could be hit if Brent sustains above ~USD 70/bbl as they earn their historical INR 3.5-4/ltr at Brent price of ~USD 70/bbl. For every USD 1/bbl rise in crude price, OMCs' auto-fuel GMM declines by INR 0.55/ltr (assuming no change in retail petrol/diesel price and excise duty on petrol/diesel) and drags down their consolidated EBITDA by 7–9%, with HPCL the worst hit given its highest leverage to the marketing business (exhibit 30-36). At spot Brent of ~USD 83bbl Brent and current diesel crack of ~USD42/bbl and petrol crack of ~USD16.5/bbl, OMCs’ blended GMM is at negative INR 13.5/ltr (historical GMM of positive INR 3.5/ltr) while integrated gross margin is still positive INR 6.0/ltr (though below the historical average of positive INR 12.4/ltr). At CMP, HPCL is trading at 1.08x FY28 PB (last 3-year average of 1.17x), BPCL is trading at 1.28x FY28 PB (last 3-year average of 1.29x) and IOCL is trading at 0.99x FY28 PB (last 3-year average of 0.94x). For every decline in OMCs’ auto-fuel integrated margin by INR1/ltr (historical INR3.5/ltr) their book value decreases by 0.2-0.5% per month. Hence, if their current gross integrated margin is INR 6/ltr below their historical margin, their book value could fall by 1.5-3% per month.

* Spot LNG prices surge after QatarGas shutdown its huge ~82mmtpa LNG export plant; India’s 35-40% of LNG imports to be impacted, hence, it is a near-term negative for PLNG, GAIL, Gujarat Gas and other gas companies: QatarGas has announced that it has stopped LNG output at its main facility after military attacks; this is Qatar’s main LNG facility and handles 82mmtpa of LNG or ~25% of global LNG supply. PLNG gets a huge 8.5mmtpa of LNG from Qatar (or ~50% of its volume). Further, adding ~1mmtpa of LNG contract of GSPC, India gets 9.5-10mmtpa of LNG from Qatar and this constitutes over 35-40% of the country’s LNG import and ~20% of its natural gas demand. PLNG has issued a press release stating that QatarEnergy issued a notice indicating a potential event of force majeure. Hence, PLNG has issued corresponding force majeure notices to its offtakers (GAIL, IOCL, BPCL). Press reports also suggest India’s gas marketing companies have informed industrial customers they would receive 10-50% lower gas supply. Hence, if this shutdown sustains for a long period, it could lead to: a) a temporary spike in spot LNG price (has already more than doubled to ~USD 25/mmbtu as reported by Bloomberg quoting traders); Europe gas price has jumped 70-80% to USD 18-19/mmbtu – this could temporarily hurt India’s LNG/Gas demand and, therefore, could be a near-term negative for volume & margin for GAIL, PLNG, Gujarat Gas and other gas companies (GSPL, IGL and MGL); and b) temporarily disrupt LNG supply to PLNG given it gets 8.5mmtpa of LNG from Qatar (or ~50% of its volume) – a near-term negative for PLNG’s volume.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...