Buy Maruti Suzuki Ltd For Target Rs.15,529 Motilal Oswal Financial services Ltd

Demand outlook remains upbeat

Healthy demand to help offset cost headwinds

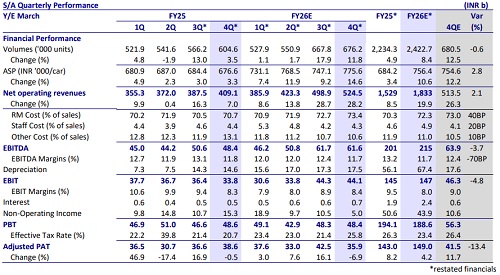

* Maruti Suzuki (MSIL)’s 4QFY26 PAT declined ~7% YoY to INR35.9b, below our estimate of INR40b. While operational performance was in line, the PAT miss was largely due to an MTM loss on its investment book.

* The GST rate cut has helped revive small car demand as vehicles are now much more affordable for price-conscious consumers. MSIL now enjoys a strong order backlog of 190k units. Given its order backlog and a healthy new launch pipeline, management is confident of posting 10% volume growth in the domestic market in FY27E, which is expected to drive market share recovery for MSIL. This would, in turn, drive the stock re-rating, in our view. Healthy demand is expected to help offset near-term cost headwinds. We expect MSIL to deliver a 16% earnings CAGR over FY26-28. We reiterate our BUY rating with a TP of INR15,529, valued at 25x FY28E EPS.

Minimal margin pressure despite multiple headwinds

* MSIL’s 4QFY26 revenue grew 28.2% YoY to INR524.5b, in line with our estimates. The combined effect of volume growth (+11.8% YoY) and improvement in average realization per car (+14.6% YoY) led to this healthy performance. FY26 revenue grew 20% YoY to INR1.8t (8% volume growth and 11% ASP growth).

* EBITDA margin came in line and was flat YoY at 11.7%. EBITDA grew 27.1% YoY in 4QFY26 to INR61.6b. FY26 EBITDA grew 6.5% YoY to INR215b as margins contracted 150bp to 11.7%.

* EBIT margin remained broadly flat YoY at 8.4% (vs. estimated 8.3%).

* Sequential EBIT margin drivers were: normalization in employee costs (100bp), lower discounts (50bp), favorable forex movement (30bp), and reduced fixed overhead led by inventory accretion (50bp). However, these were partially offset by higher commodity costs (80bp), elevated launch-related expenditure for new models (60bp), and the seasonal nature of CSR/R&D spending in 4Q in other expenses (20bp).

* Non-operating income came in far below our est. at ~INR5b (vs. est. INR10.6b), primarily due to MTM losses on the investment book.

* Consequently, PAT missed our estimates, declining 7% YoY to INR35.9b (vs. estimated ~INR40b). FY26 PAT grew 4.2% YoY to INR149b.

* FY26 OCF generation stood at INR190b, while FCF generation stood at INR87b. FY26 RoE/RoCE stood at 13.7%/18%.

Key highlights from the management commentary

* MSIL’s second plant in Kharkhoda has commenced production in Apr’26, and its fourth plant in Gujarat is expected to commence production by Jul’26. Each of these would have about 250k units p.a. capacity. Beyond this, MSIL would be investing INR 140b in capex in FY27E for further expansion. This itself highlights management’s confidence in sustaining demand momentum going forward. Given its healthy order backlog and positive consumer sentiment, MSIL has provided a strong domestic volume growth guidance of 10% YoY for FY27E.Given the adverse global macro environment, management has refrained from giving an export outlook for FY27E.

* While startup costs associated with these new facilities are likely to drive nearterm margin impact, the same is likely to be offset by operating leverage benefits.

* Management believes there remains meaningful headroom for ASP expansion, driven by white spaces in the SUV space. A richer SUV mix and increasing EV penetration over time should structurally improve MSIL’s ASPs and support margin improvement.

* MSIL remains committed to a multi-powertrain strategy spanning ICE, CNG, ethanol-compatible vehicles, hybrids, and EVs. Thus, it remains well placed to meet its CAFÉ 3 compliance.

* Despite robust demand, supply constraints limited volume upside potential for MSIL in 4Q. This led to a rise in the order backlog to ~190k units, of which ~130k units were in the small cars segment.

* Given the supply constraints, dealer inventory remained lean at roughly 12 days, which is well below the normal level of 4-5 weeks.

Valuation and view

The GST rate cut has helped revive small car demand as vehicles are now much more affordable for price-conscious consumers. MSIL now enjoys a strong order backlog of 190k units. Given its order backlog and a healthy new launch pipeline, management is confident of posting 10% volume growth in the domestic market in FY27E, which is expected to drive market share recovery for MSIL. This would, in turn, drive the stock re-rating, in our view. Healthy demand is expected to help offset near-term cost headwinds. We expect MSIL to deliver a 16% earnings CAGR over FY26-28. We reiterate our BUY rating with a TP of INR15,529, valued at 25x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041