Buy Juniper Hotels Ltd for Target Rs. 250 by Choice Institutional Equities

Scaling India’s Largest Hyatt-affiliated Luxury Portfolio

Backed by a long-standing Hyatt–Saraf partnership, JUNIPER’s JV ownership structure (Hyatt 38.8% / Saraf 38.8%) supports sustained brand access and local execution. JUNIPER operates India’s largest Hyatt-affiliated luxury and upper-upscale platform, owning ~20% of Hyatt’s domestic key base (~1,895 keys), with hotels concentrated in high-barrier corridors (BKC, Aerocity, and select state capitals) that support RevPAR resilience. A visible pipeline across Bengaluru Airport, Northeast India and other projects positions JUNIPER to grow keys by 77%+ by FY29E.

The "Big-Box" Advantage: High Yields and Diversified Income

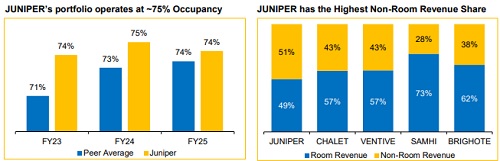

JUNIPER’s portfolio operates at ~75% utilisation, led by “Big-Box” hotels such as Grand Hyatt Mumbai (GHM) and Andaz Delhi that command ~15–20% ARR premiums vs the city average. Non-room revenue contributes 51% of total revenue, led by F&B and MICE from large-scale banqueting and specialty dining, and is expected to grow at a 19.1% CAGR (FY26E–FY29E). The new ~49K sq.ft. ballroom at GHM and upgrades across Andaz Delhi, Hyatt Ahmedabad and Hyatt Raipur should lift yield per key. With assets stabilised and efficiencies improving, incremental revenue should translate into higher EBITDA conversion, supporting ~243 bps margin accretion (FY26E–FY29E).

Capital Discipline & Balanced Growth Sustaining Value Creation

Following its INR 18 Bn IPO and balance sheet deleveraging, JUNIPER has transitioned into a phase of capital discipline and self-funded expansion. INR 15 Bn+ of debt has been repaid post-listing, reducing interest costs by ~60% and lowering net debt-to-equity to ~0.3x, enabling a structurally leaner balance sheet. Future growth is expected to be primarily self-funded, supported by strong operating cash flows and minimal incremental leverage. JUNIPER also has an opportunity to acquire Hyatt Regency Mumbai and Hyatt Regency Chennai from the promoter group via ROFO, structured as cashless share swaps, adding 737 keys over time. Commercial land banks adjoining Grand Hyatt Mumbai and in high-growth corridors remain embedded long-term value drivers, supporting continuity in JUNIPER’s valuecreation trajectory.

Investment View: We initiate coverage on JUNIPER with a BUY rating and an EV/Adj. EBITDA of 11.0x to arrive at a TP of INR 250, implying an upside potential 22.7%. We expect Revenue / Adj. EBITDA / PAT expected to expand at a CAGR of 18.3% / 21.2% / 30.8% over FY26E–29E, driven by, growth in keys, “Big-box” operating model, capex funding largely from internal accruals.

Key Risks: Extended geopolitical tensions, Project execution delay & geographic concentration of assets

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131